Please use a PC Browser to access Register-Tadawul

Get It

How Atlassian’s (TEAM) Lowered Billings Outlook Could Influence Its Long-Term Growth Story

Atlassian Corp Class A TEAM | 83.62 | +1.35% |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To be a shareholder in Atlassian, you need to believe in its ability to drive long-term recurring revenue through continued cloud migrations, AI-powered feature adoption, and expanded use among large enterprise clients. The recent lowering of full-year billings guidance directly impacts the most important short-term catalyst, enterprise cloud adoption, while also highlighting execution risk as the biggest current challenge. This moderation in outlook signals that near-term growth may be lumpier than previously assumed, though the fundamental business case remains closely tied to successful cloud transitions.

Of Atlassian’s recent announcements, the acquisition of developer intelligence firm DX stands out for its relevance to customer value expansion and product differentiation. By integrating DX’s capabilities, Atlassian aims to enhance its AI-driven insights for developers, a potential catalyst for deepening adoption among existing customers and supporting future upsell opportunities. The development is particularly meaningful in light of heightened market focus on cloud and AI metrics as key value drivers for the business.

In contrast, investors should be aware that cloud billings volatility could have ongoing effects on Atlassian’s free cash flow and ability to fund growth initiatives ...

Atlassian's narrative projects $8.7 billion revenue and $310.2 million earnings by 2028. This requires 18.7% yearly revenue growth and a $566.9 million earnings increase from -$256.7 million currently.

Uncover how Atlassian's forecasts yield a $245.23 fair value, a 66% upside to its current price.

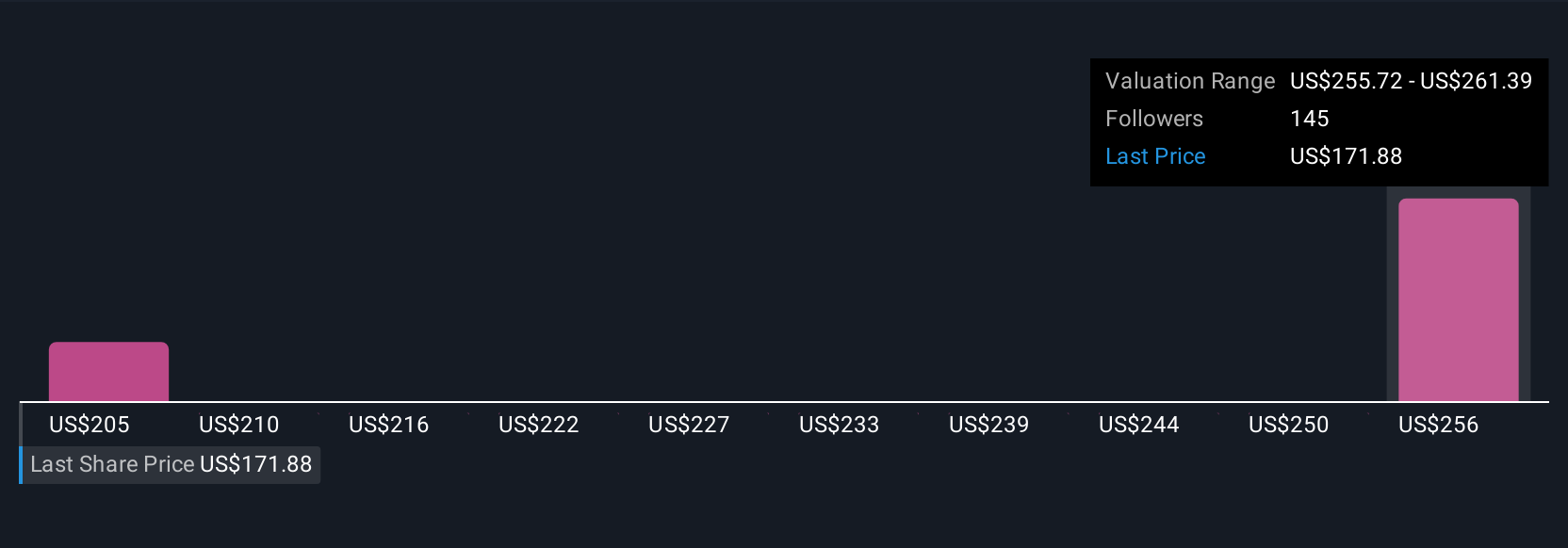

Six unique fair value estimates from the Simply Wall St Community place Atlassian’s value between US$204.74 and US$250.73 per share. While many see significant upside, ongoing variability in cloud billings and cash flow could reshape these expectations, consider how diverging views reflect real uncertainty around future performance.

Explore 6 other fair value estimates on Atlassian - why the stock might be worth as much as 69% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.