Please use a PC Browser to access Register-Tadawul

Get It

How Collegium’s New $980 Million Credit Facility Could Reshape Collegium Pharmaceutical (COLL) Investors’ Risk Lens

Collegium Pharmaceutical, Inc. COLL | 45.00 | -0.40% |

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

To own Collegium, you need to believe its focused pain and ADHD portfolio can sustain earnings despite looming patent cliffs, regulatory scrutiny of opioids, and rising commercial spend. The new US$980 million credit facility looks helpful but does not fundamentally change the near term catalyst around Jornay PM execution or the central risk of future generic and pricing pressure.

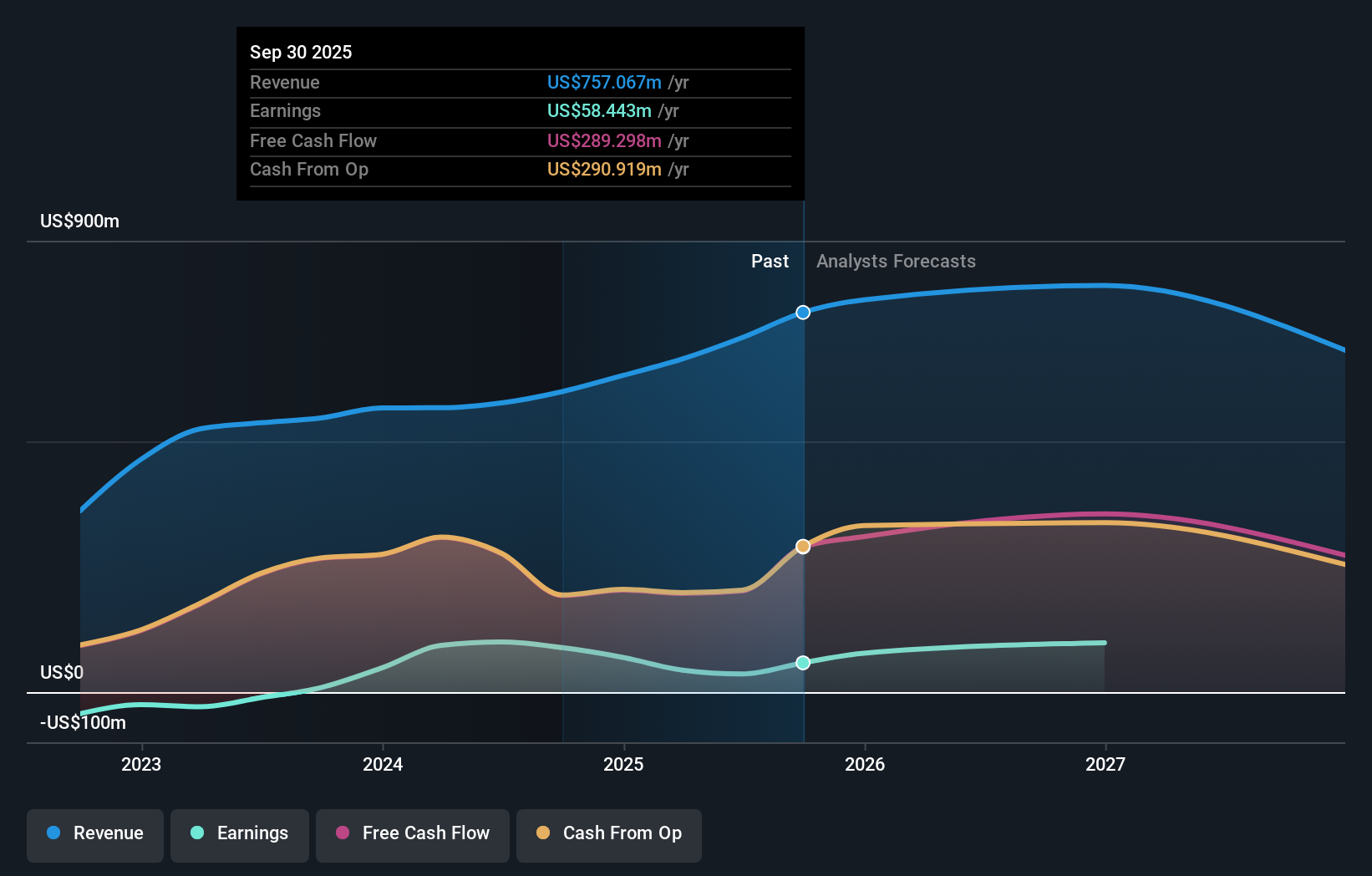

Among recent announcements, the Q3 2025 guidance raise to US$775 million to US$785 million in net product revenue is most relevant here, as it highlights management’s confidence while the company refinances into lower cost, more flexible debt. Together, improving earnings and a reworked balance sheet may influence how investors weigh concentration risk in core pain brands against Collegium’s plans for portfolio expansion.

Yet, against this stronger balance sheet, investors should still be aware of the looming patent expirations and potential generic competition that could...

Collegium Pharmaceutical's narrative projects $695.3 million revenue and $131.4 million earnings by 2028.

Uncover how Collegium Pharmaceutical's forecasts yield a $48.67 fair value, a 3% upside to its current price.

Three Simply Wall St Community fair value estimates for Collegium span roughly US$49 to US$183 per share, underscoring how far apart individual views can be. Against that backdrop, the new lower cost credit facility and associated financial risk considerations give you more context to compare these perspectives and explore alternative views on the company’s future performance.

Explore 3 other fair value estimates on Collegium Pharmaceutical - why the stock might be worth over 3x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.