How DoorDash’s Hibbett Partnership And Profitability Surge At DoorDash (DASH) Has Changed Its Investment Story

DoorDash, Inc. Class A DASH | 156.45 | +3.95% |

- In January 2026, DoorDash and Hibbett, Inc. announced a partnership to offer on-demand delivery of athletic footwear, apparel, and accessories from roughly 1,000 Hibbett stores across the United States, including availability through DashPass.

- Against a backdrop of strong operating performance and very large earnings per share growth, this expansion into sporting goods highlights DoorDash’s push to broaden its convenience-focused marketplace beyond restaurants and groceries.

- We’ll now examine how DoorDash’s improved profitability, alongside its Hibbett partnership, may influence the company’s longer-term investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

What Is DoorDash's Investment Narrative?

To own DoorDash, you really need to believe in its evolution from food delivery into a broader, convenience-first logistics platform, where high-margin, incremental orders justify a still-rich valuation multiple. The Hibbett tie-up slots neatly into that story, adding nearly 1,000 athletic stores to a retail network that already includes Old Navy, RONA and others, but on its own it is unlikely to shift the near-term financial picture materially. The more immediate catalysts remain the upcoming Q4 2025 results and any updates on capital allocation, automation and international expansion, particularly given earnings growth has recently far outpaced revenue growth. On the risk side, rising regulatory pressure on gig worker pay, intensifying fee competition and growing consumer pushback on delivery costs all sit in the foreground, with the Hibbett deal doing little to reduce those pressures.

Yet behind the growth story, one structural risk could still surprise newer shareholders.

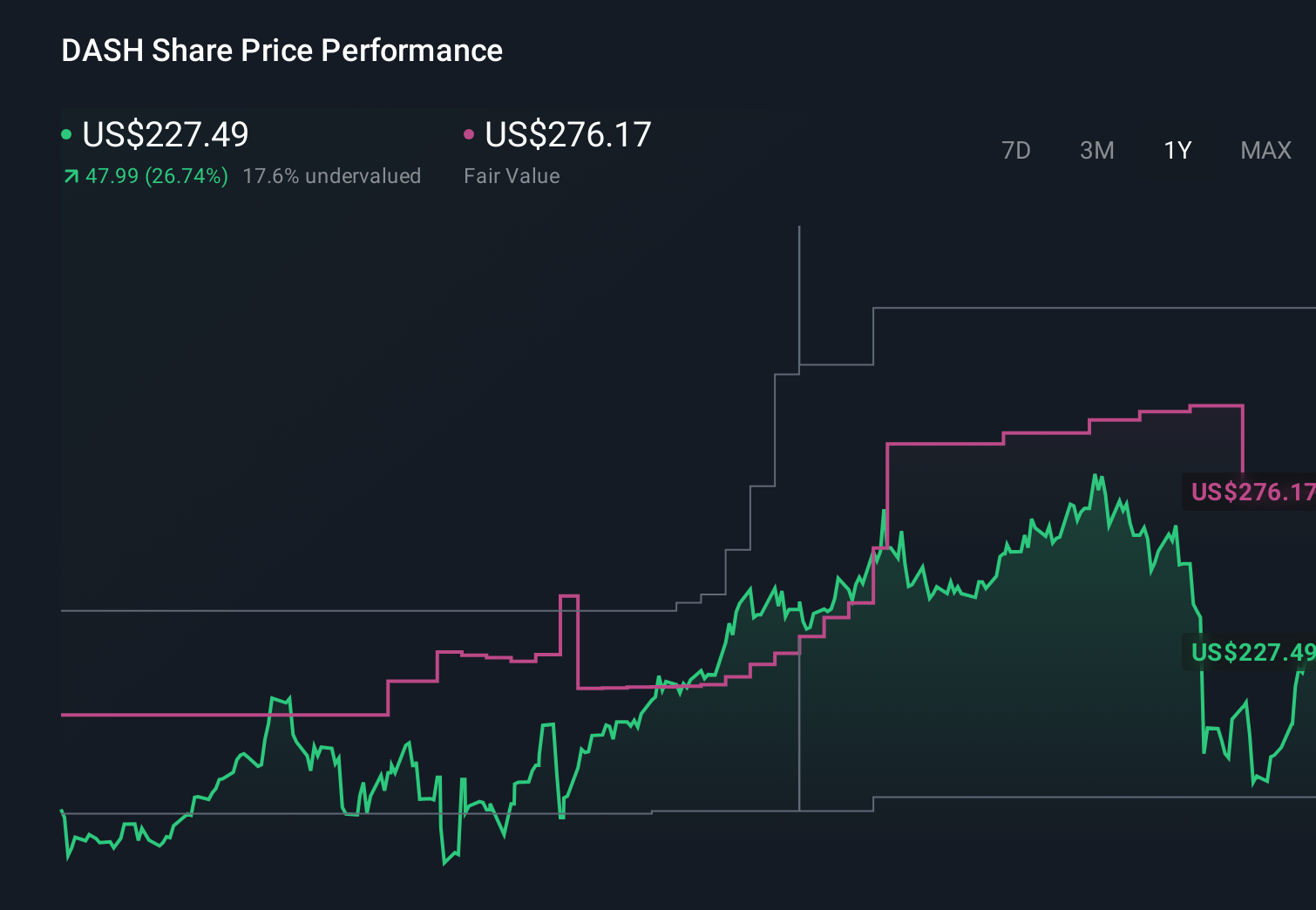

Despite retreating, DoorDash's shares might still be trading above their fair value and there could be some more downside. Discover how much.Exploring Other Perspectives

Thirteen Simply Wall St Community fair value views spread from about US$194 to US$418 per share, reflecting very different expectations around DoorDash’s future. Set that against the rich earnings multiple and ongoing regulatory and fee pressures, and it becomes clear why you may want to weigh several viewpoints before deciding how much risk you are comfortable with here.

Explore 13 other fair value estimates on DoorDash - why the stock might be worth over 2x more than the current price!

Build Your Own DoorDash Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 112 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.