Please use a PC Browser to access Register-Tadawul

Get It

How Investors Are Reacting To Automatic Data Processing (ADP) Steady Earnings Growth and Russell 1000 Influence

Automatic Data Processing, Inc. ADP | 266.10 | +1.18% |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To be a shareholder in Automatic Data Processing, you need to believe in the long-term demand for outsourced, cloud-based HR and payroll solutions as businesses digitize operations. The recent results, showing stable margins and healthy revenue gains, reinforce the view that ADP’s core franchises remain resilient. These updates do not appear to materially affect the key short-term catalyst for ADP, sustaining growth in advanced technology product adoption, nor do they significantly shift the main risk: ongoing competitive pressure and delayed deal closures. Among recent company news, ADP’s product launches, particularly the rollout of ADP® Embedded Payroll for SMB software providers, aligns closely with the company’s growth catalysts. This move supports ADP’s efforts to increase customer lock-in and expand its addressable market through technology adoption, potentially offsetting booking slowdowns or sales cycle delays if widely embraced. Yet, the growing influence of newer, SaaS-native competitors could lead to an acceleration in pricing pressure and pipeline delays, which investors should be aware of as...

Automatic Data Processing is projected to reach $24.3 billion in revenue and $5.1 billion in earnings by 2028. This outlook depends on a 5.7% annual revenue growth rate and a $1.0 billion increase in earnings from the current level of $4.1 billion.

Uncover how Automatic Data Processing's forecasts yield a $314.17 fair value, a 11% upside to its current price.

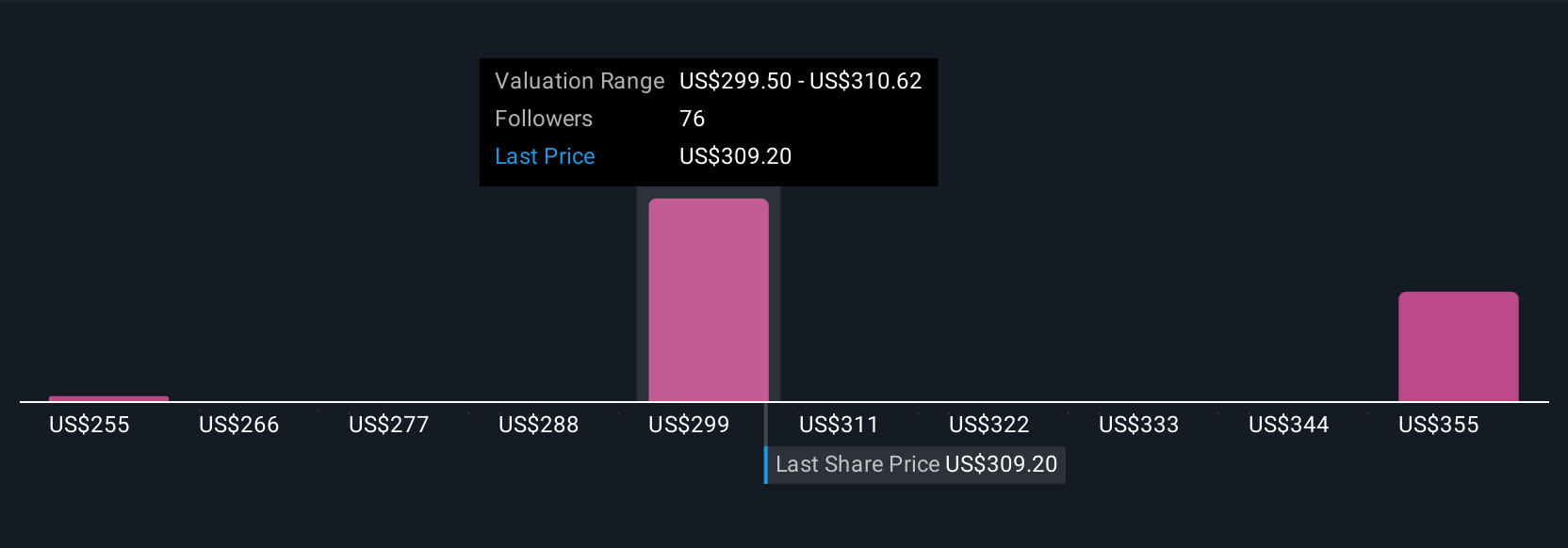

Private fair value estimates from eight Simply Wall St Community members for ADP range widely from US$235 to US$387 per share. With deal cycle delays posing a real risk, you may want to review how others see pressure points shaping future results.

Explore 8 other fair value estimates on Automatic Data Processing - why the stock might be worth 17% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.