Please use a PC Browser to access Register-Tadawul

Get It

How Investors May Respond To Ares Management (ARES) Spotlighting Fee-Driven Growth and Private Credit Expansion

Ares Management Corporation ARES | 113.36 | +1.21% |

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

To be a shareholder of Ares Management, one needs to believe that investor demand for alternative assets will remain strong, supporting fee-driven revenue growth, even as competition increases. The recent focus at the Citizens Financial Services Conference 2025 on the capital-light, fee-centric model reinforces this narrative, supporting the company’s key short-term catalyst: converting dry powder into fee-earning assets. The biggest near-term risk, intensifying competition and potential pressure on management fees, remains relevant, but the news event does not materially shift this risk landscape.

Among recent developments, the launch of the Ares Core Infrastructure Fund in Australia stands out, directly supporting management’s outlook for growth in digital infrastructure and asset-based lending. This initiative highlights Ares’ ability to expand into new markets, which aligns with ongoing catalysts such as broadening the firm’s addressable market and increasing fee-generating assets. However, these expansion efforts also bring into focus how execution and integration risks can shape future returns.

By contrast, fee pressure from competitors is a risk investors should be aware of if Ares cannot sustain its margins in the face of...

Ares Management's narrative projects $7.1 billion revenue and $2.2 billion earnings by 2028. This requires 13.7% yearly revenue growth and a $1.83 billion earnings increase from $369.5 million.

Uncover how Ares Management's forecasts yield a $183.94 fair value, a 27% upside to its current price.

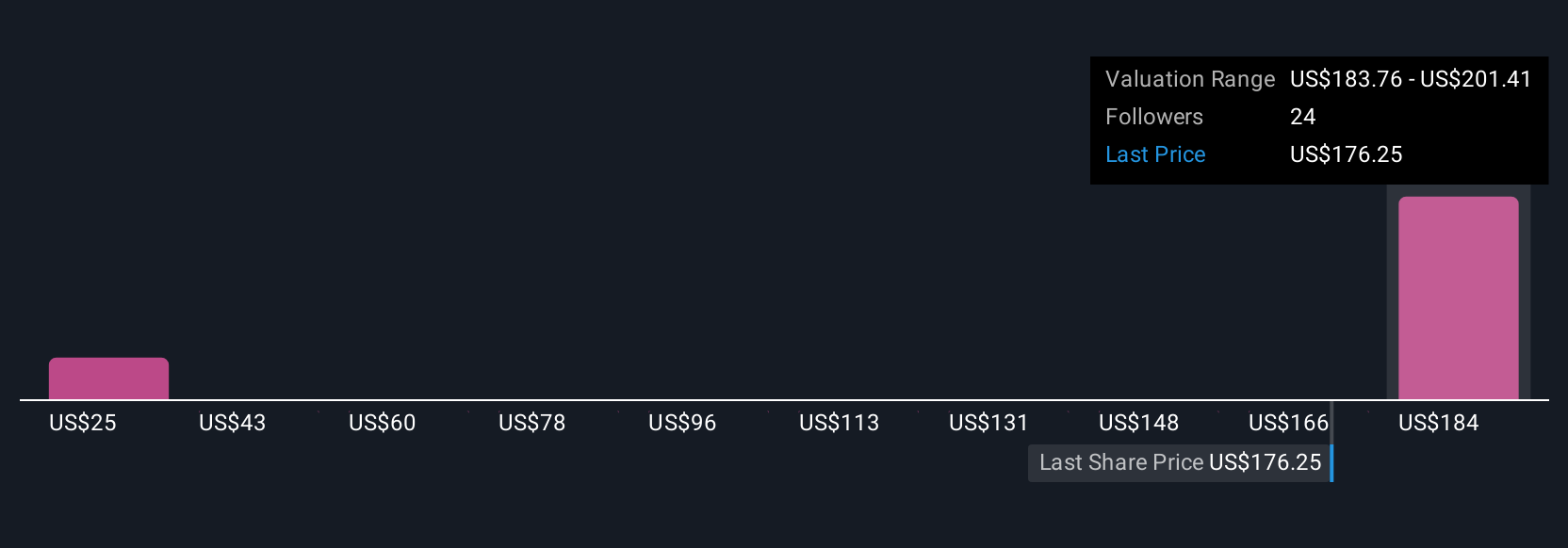

Simply Wall St Community members provided three fair value estimates for Ares Management ranging from US$31.12 to US$201.41 per share. As you consider these differing outlooks, keep in mind that ongoing fee competition remains a central challenge to watch for future earnings and revenue momentum.

Explore 3 other fair value estimates on Ares Management - why the stock might be worth as much as 40% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.