Please use a PC Browser to access Register-Tadawul

Get It

How Investors May Respond To Element Solutions (ESI) Margin Jitters From Rising Middle East-Linked Input Costs

Element Solutions Inc ESI | 31.32 31.32 | +1.06% 0.00% Pre |

Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

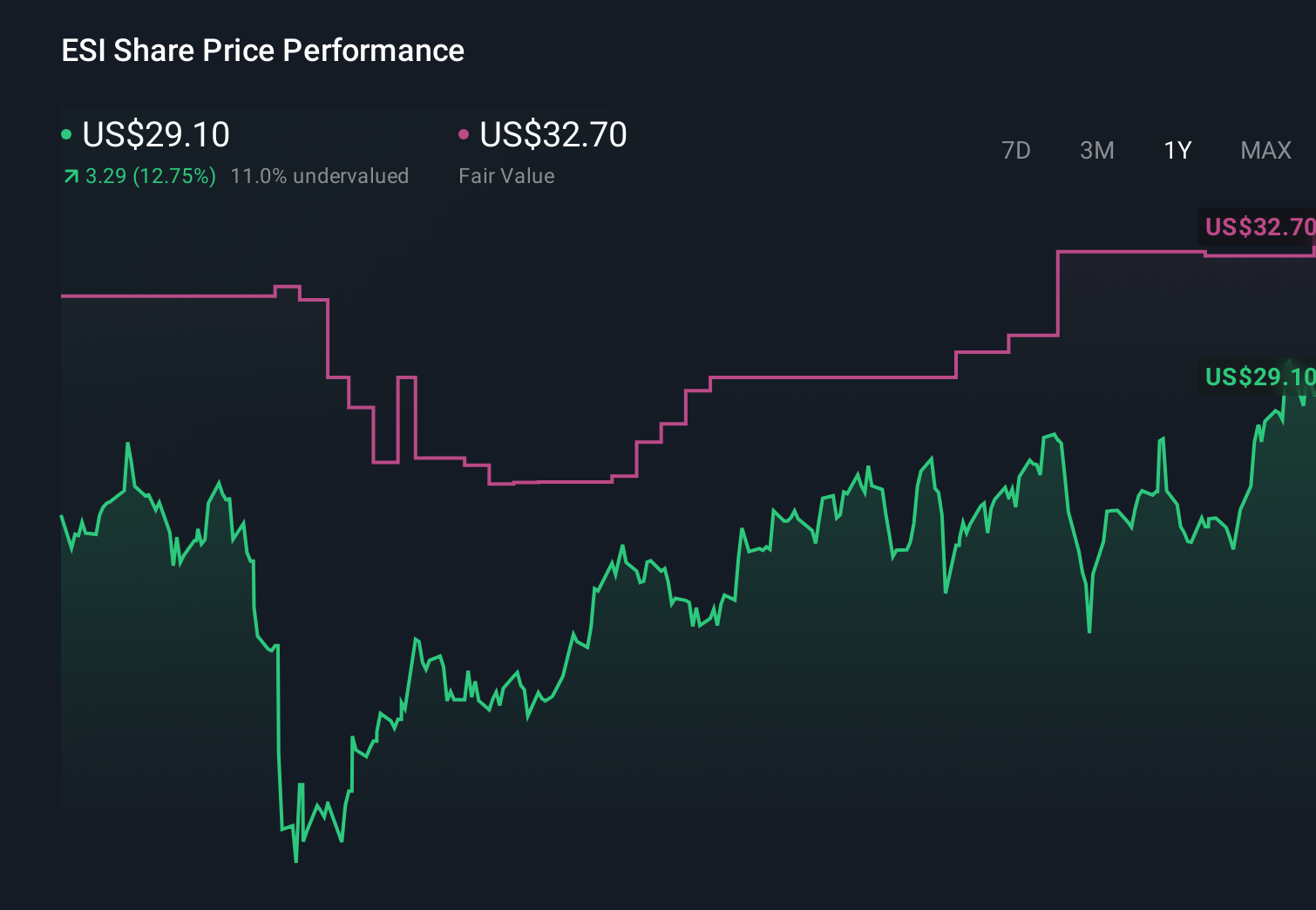

To own Element Solutions, you need to believe in its role as a specialty materials supplier to structurally important end markets like high performance computing and EVs, while accepting exposure to cyclical demand and margin swings. The recent oil driven pullback looks more like a sector shock than a change in that core thesis, but it does underline the near term risk that higher feedstock costs could compress margins if pricing and efficiency actions lag.

The most recent quarterly results for Q4 2025, which showed higher sales of US$676.2 million but lower net income of US$6.1 million year on year, are particularly relevant in this context, as they already point to pressure on profitability before the latest spike in input costs. For investors watching catalysts, the tension between revenue growth in targeted end markets and tighter margins is now front and center.

But even with those growth drivers, investors should be aware that...

Element Solutions' narrative projects $2.8 billion revenue and $438.6 million earnings by 2028. This requires 3.9% yearly revenue growth and about a $198 million earnings increase from $240.4 million today.

Uncover how Element Solutions' forecasts yield a $38.50 fair value, a 18% upside to its current price.

Two members of the Simply Wall St Community currently place Element Solutions’ fair value between US$36.19 and US$38.50, reflecting a tight cluster of views rather than a wide spread. Against that backdrop, the recent sector wide concern about input cost driven margin compression gives you a concrete risk to weigh as you compare these community estimates with your own expectations for the business.

Explore 2 other fair value estimates on Element Solutions - why the stock might be worth as much as 18% more than the current price!

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.