Please use a PC Browser to access Register-Tadawul

Get It

How Investors May Respond To Global-E Online (GLBE) Targeting First Full-Year Profitability in 2025

Global-E Online Ltd. GLBE | 40.15 40.50 | +0.10% +0.87% Pre |

Find companies with promising cash flow potential yet trading below their fair value.

To own Global-E Online shares, investors need confidence in sustained cross-border e-commerce growth, the company's ability to deepen merchant relationships, and success expanding in regions like APAC and LATAM. While the recent announcement of targeting full-year GAAP profitability in 2025 is an encouraging milestone and may act as a near-term catalyst for sentiment, it does not meaningfully change the core risks, especially the ongoing reliance on major partners like Shopify and the competitive pressure in its space.

Among recent company announcements, Global-E's renewed 3-year partnership with Shopify stands out. This agreement solidifies a direct-to-consumer channel, ensuring Global-E continues to power international e-commerce for some of the largest merchants, which is crucial as competition and customer concentration remain at the forefront of both opportunity and risk for the business. Yet, it also amplifies the inherent exposure to any changes in partnership terms or strategy.

But investors should not overlook the possibility that if Shopify reduces its dependency on Global-E or pursues insourcing, the resulting volatility could...

Global-E Online's outlook calls for $1.7 billion in revenue and $328.6 million in earnings by 2028. This scenario assumes 25.6% annual revenue growth and a $357 million swing in earnings from the current -$28.4 million.

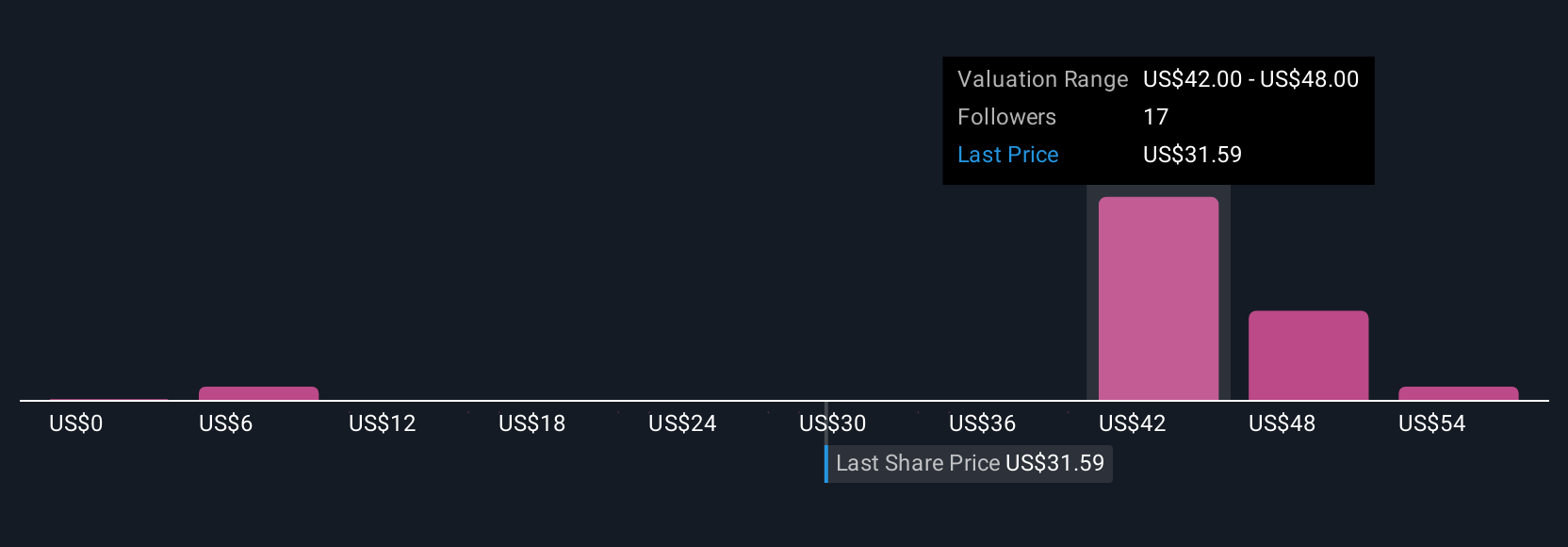

Uncover how Global-E Online's forecasts yield a $47.69 fair value, a 30% upside to its current price.

Simply Wall St Community members have submitted 11 fair value estimates on Global-E ranging from US$11.82 to US$118.19, underscoring wide-ranging outlooks. While many anticipate robust revenue gains ahead, continued dependence on partners like Shopify is a key factor influencing whether those growth targets are achieved; examine the full spectrum of peer perspectives for a well-rounded view.

Explore 11 other fair value estimates on Global-E Online - why the stock might be worth less than half the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.