Please use a PC Browser to access Register-Tadawul

Get It

How Investors May Respond To JBT Marel (JBTM) Surging Sales and Margin Pressure in Q2 Results

JBT Marel Corporation JBTM | 127.00 | -2.47% |

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

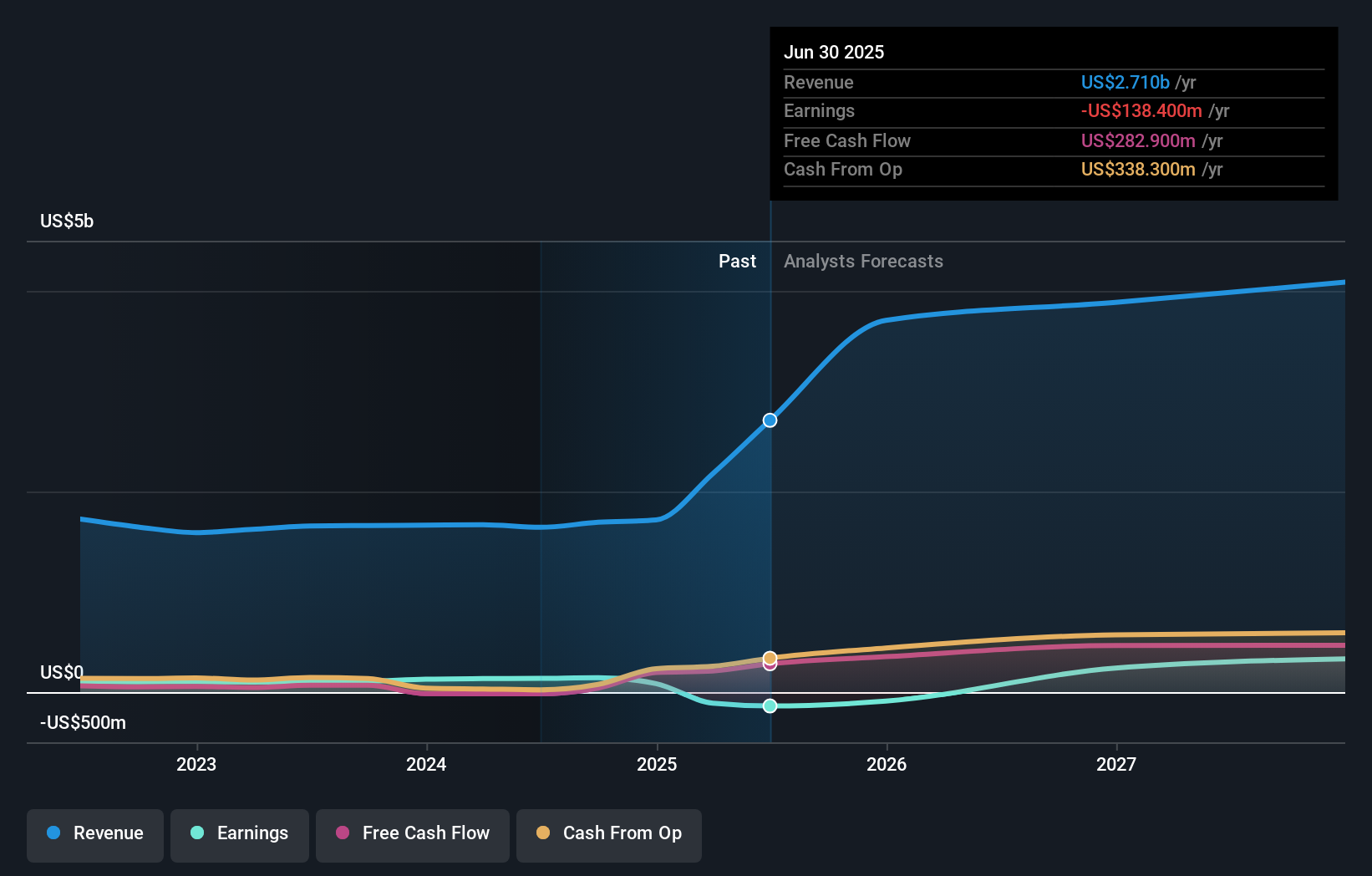

To be a shareholder in JBT Marel, you need confidence that the accelerating demand for automated food processing and persistent synergy gains from the JBT-Marel merger can eventually drive durable revenue and margin growth, despite current earnings volatility. The latest quarterly results, while showcasing robust top-line progress, leave the short-term margin recovery story unchanged, margin pressure remains the key risk, and integration milestones are the most important catalyst; neither is materially shifted by the recent dividend announcement.

The affirmation of full-year revenue guidance provided alongside the quarterly results stands out this quarter. By maintaining targets despite short-term earnings headwinds, management signals continued faith in the underlying order backlog and after-market momentum, factors that remain central to near-term performance triggers. In contrast, investors should not overlook ongoing concerns about interest payments outpacing earnings...

JBT Marel's outlook envisions $4.6 billion in revenue and $791.7 million in earnings by 2028. This scenario is based on a 19.0% annual revenue growth rate and an $930.1 million increase in earnings from the current loss of $-138.4 million.

Uncover how JBT Marel's forecasts yield a $149.42 fair value, a 10% upside to its current price.

Three members of the Simply Wall St Community place JBT Marel's fair value between US$86.42 and US$299.95 per share. Against this broad spectrum of views, margin headwinds from elevated tariffs and integration challenges may explain why opinions on the company's potential vary so much, highlighting the importance of reviewing multiple outlooks before forming your own.

Explore 3 other fair value estimates on JBT Marel - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Opportunities like this don't last. These are today's most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.