Please use a PC Browser to access Register-Tadawul

Get It

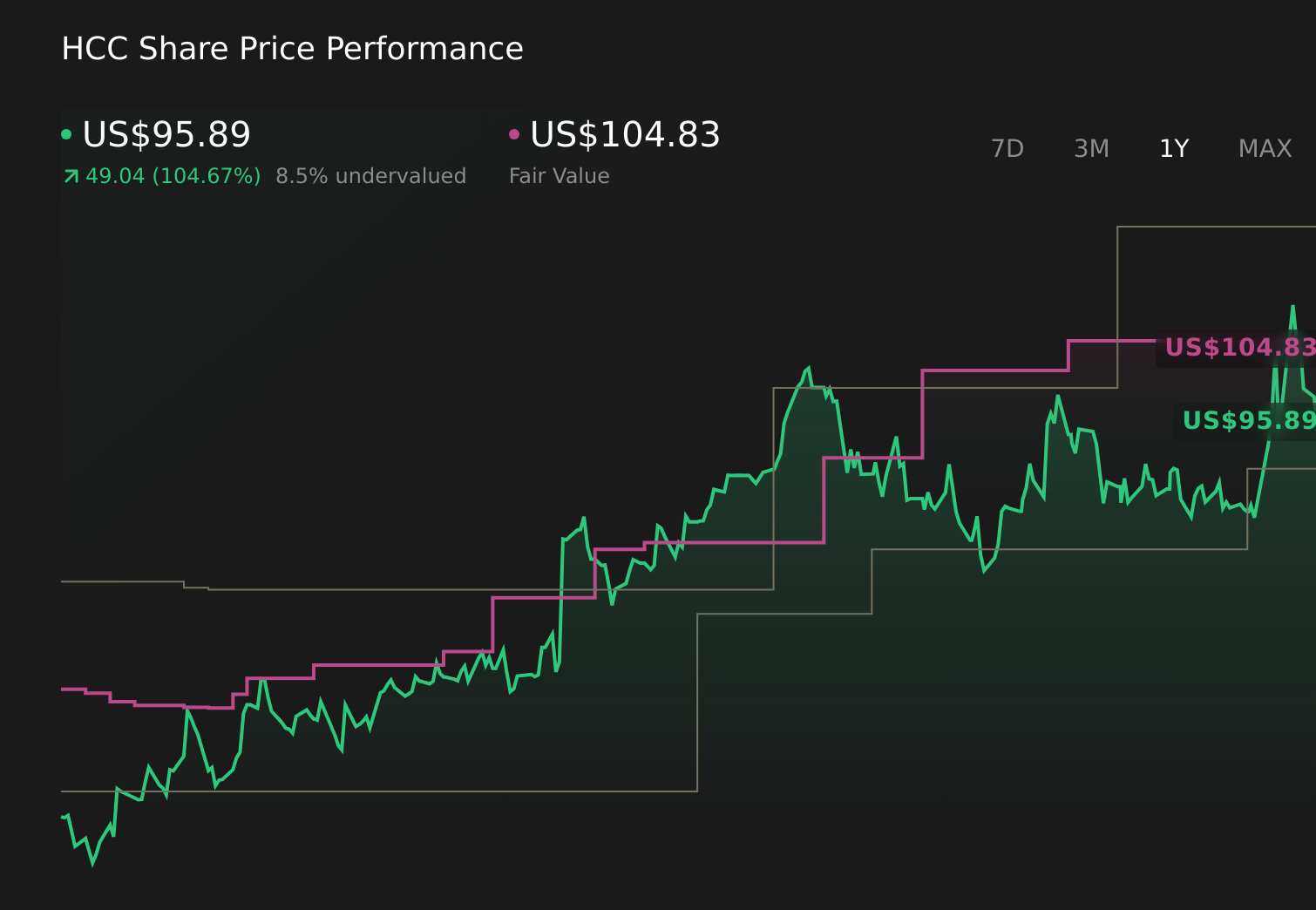

How Investors May Respond To Warrior Met Coal (HCC) After Blue Creek Boosts Output And 2026 Guidance

Warrior Met Coal, Inc. HCC | 81.13 81.13 | -2.53% 0.00% Pre |

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

To own Warrior Met Coal today, you need to believe that adding Blue Creek’s output can offset pricing and demand pressures in global steelmaking coal. The latest report shows Blue Creek already contributing meaningfully to Q4 2025 production, which supports the near term growth catalyst of higher volumes. The biggest risk remains whether global steel demand and pricing can absorb this extra supply without further compressing margins. So far, this update does not remove that concern.

The 2026 production and sales guidance of 12.0 to 13.0 million short tons and 12.5 to 13.5 million short tons, respectively, is the key new datapoint here. It frames just how quickly Warrior Met is leaning into Blue Creek and higher volumes after a year in which full year 2025 earnings fell to US$57.0 million. For investors, the guidance connects directly to the central catalyst of volume growth versus the persistent risk of weaker steel and coal pricing.

Yet even with Blue Creek ramping, investors should be aware that weaker steelmaking coal prices could still...

Warrior Met Coal's narrative projects $2.0 billion revenue and $636.5 million earnings by 2028.

Uncover how Warrior Met Coal's forecasts yield a $102.17 fair value, a 16% upside to its current price.

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$1.9 billion and earnings of roughly US$264 million by 2028, which is much more conservative than the baseline view. If you are weighing Blue Creek’s strong early production, it is worth recognizing that these pessimists see long term demand and margin risks very differently, and their expectations may shift again as they absorb this latest guidance.

Explore 3 other fair value estimates on Warrior Met Coal - why the stock might be worth 11% less than the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.