Please use a PC Browser to access Register-Tadawul

Get It

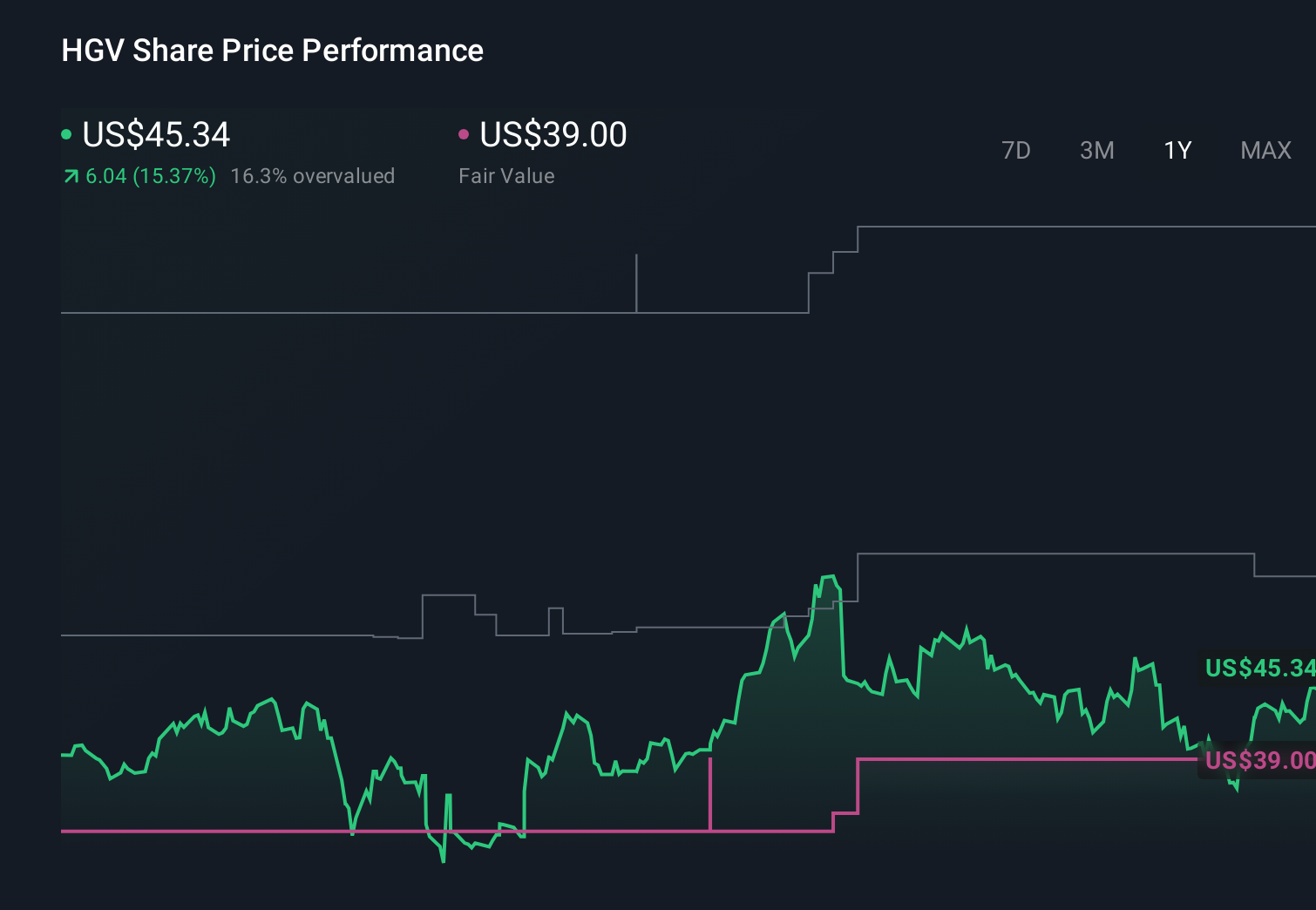

How Softer Timeshare Demand and Higher Leverage Could Impact Hilton Grand Vacations (HGV) Investors

Hilton Grand Vacations, Inc. HGV | 48.54 | +0.77% |

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

To own Hilton Grand Vacations, you need to believe in the resilience of its timeshare and membership model despite softer tour volumes, slower member-point growth and high leverage. The key near term catalyst remains the company’s ability to stabilize demand without eroding margins, while the most immediate risk is that weaker profitability meets an already elevated net-debt-to-EBITDA position. Recent data on softer demand and declining returns on invested capital directly heighten this balance sheet and credit risk.

Among recent announcements, the company’s US$375 million securitization of timeshare loans in May 2024 stands out in this context. While it improved liquidity and helped pay down other debt, it also reinforces how dependent the business is on capital markets access at reasonable rates, especially when cash generation is pressured by weaker member-point growth and softer tour activity.

Yet behind the brand strength and membership appeal, investors should also be aware of the rising tension between elevated debt and...

Hilton Grand Vacations' narrative projects $6.4 billion revenue and $785.5 million earnings by 2028. This requires 12.6% yearly revenue growth and an earnings increase of about $728.5 million from $57.0 million today.

Uncover how Hilton Grand Vacations' forecasts yield a $51.70 fair value, a 7% upside to its current price.

Four fair value estimates from the Simply Wall St Community span from about US$51.70 to over US$54,000, showing just how far apart investor opinions can be. Against this backdrop, recent signs of slowing demand and high leverage give you clear reasons to compare several viewpoints before deciding how Hilton Grand Vacations might fit into your portfolio.

Explore 4 other fair value estimates on Hilton Grand Vacations - why the stock might be worth just $51.70!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.