Intapp (INTA): Reviewing Valuation After Earnings, New Guidance, and Share Buyback Completion

Intapp, Inc. INTA | 0.00 |

Intapp (INTA) just released first-quarter earnings, updated its revenue guidance for the next quarter and full fiscal year, and wrapped up a significant share buyback. These announcements influence the investment landscape for current and prospective shareholders.

Intapp’s stock has experienced a significant shift this year, with a year-to-date share price return of -40.28% and a one-year total shareholder return of -35.28%, highlighting a challenging period for investors despite new guidance and a major buyback. Still, momentum has picked up recently, as shown by its 4.5% share price gain over the last three months, which suggests sentiment may be starting to improve in response to the latest updates and renewed management confidence.

If you’re looking for your next investing idea beyond software, now’s a good time to broaden your horizon and discover fast growing stocks with high insider ownership

With the share price still well below analyst targets and double-digit revenue growth, is Intapp undervalued at these levels, or has the market already factored in all future upside? Could this be a true buying opportunity?

Most Popular Narrative: 36.9% Undervalued

Analyst consensus suggests Intapp’s fair value is $61.13, substantially above the latest closing price of $38.60. This signals optimism in the company’s growth prospects and hints at a wide gap between market price and narrative expectations.

Intapp's recent investments in AI capabilities, including the launch of Intapp DealCloud Activator and the transformed Intapp Time product, are designed to drive client engagement and operational efficiencies. These innovations are expected to bolster revenue by enhancing product appeal and encouraging cloud adoption among existing and potential clients.

What assumptions power such a lofty valuation? The narrative leans heavily on future earnings turnarounds, breakthrough AI adoption, and aggressive top-line expansion. Interested in the specifics about revenue, profit margins, and what truly shapes this valuation target? Unpack the core drivers behind the bullish thesis and see what surprises are embedded in this story.

Result: Fair Value of $61.13 (UNDERVALUED)

However, Intapp’s success remains tied to seamless cloud migration and effective partner execution. These factors could challenge anticipated growth if they fall short.

Another View: Market Multiples Challenge the Bullish Narrative

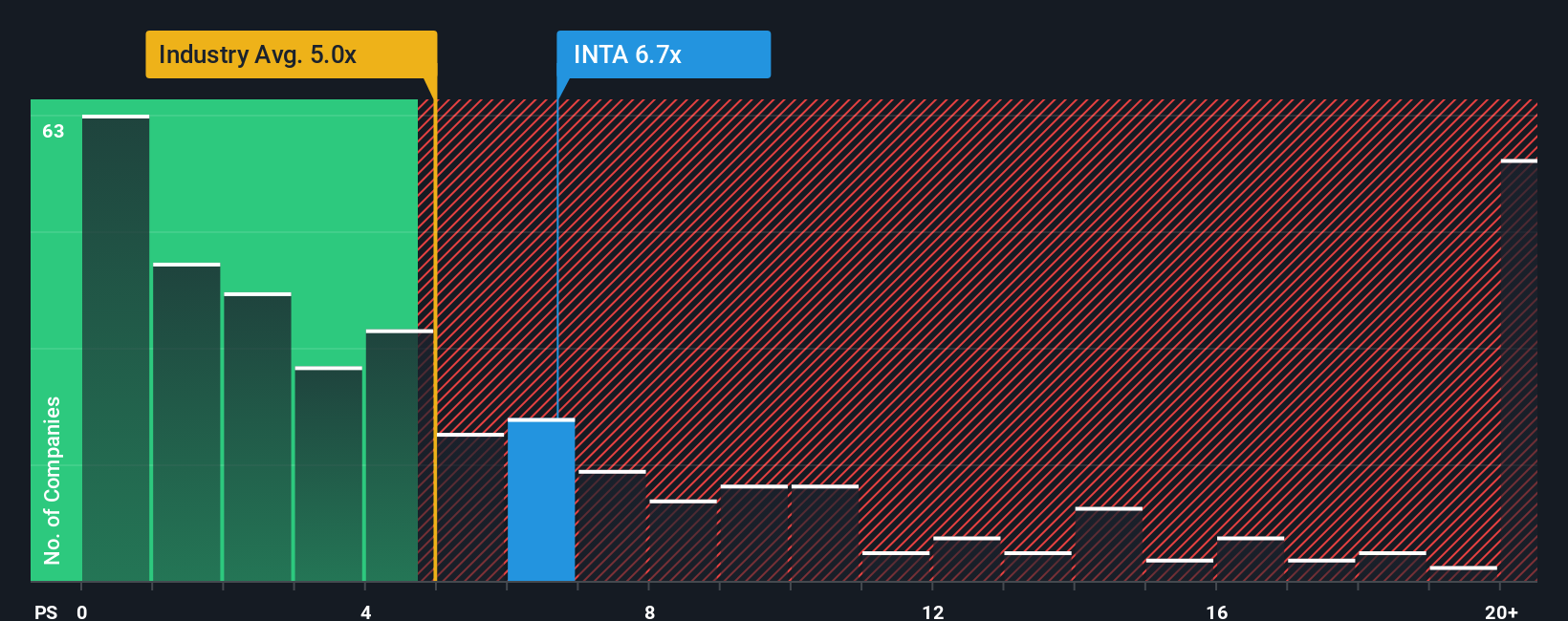

Looking beyond the fair value estimate, Intapp’s current price-to-sales ratio stands at 6x. This is higher than both the US software industry average of 5.1x and the peer group’s 5.2x. It is also above the estimated fair ratio of 5x. This suggests the stock is pricing in elevated growth expectations, adding valuation risk if future performance does not match up. Are investors being too optimistic, or is the market correctly anticipating a stronger turnaround?

Build Your Own Intapp Narrative

If our perspective differs from yours or you’d rather dig into the details on your own, you can build your personalized narrative in under three minutes with Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Intapp.

Looking for More Smart Investment Ideas?

Jump on today’s opportunities with stocks that could energize your portfolio. The right move now can help you stay ahead of the crowd tomorrow.

- Capture reliable income streams and grow your wealth steadily with these 17 dividend stocks with yields > 3%, which offers yields above 3%.

- Capitalize on groundbreaking developments shaping medicine by joining these 32 healthcare AI stocks, a group that is shaking up the healthcare sector through transformative AI innovation.

- Ride the next digital transformation wave by tapping into these 82 cryptocurrency and blockchain stocks, which is making real progress in cryptocurrency and blockchain advancements.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.