Investors Don't See Light At End Of SNDL Inc.'s (NASDAQ:SNDL) Tunnel And Push Stock Down 25%

Sundial Growers SNDL | 1.36 | +2.26% |

Unfortunately for some shareholders, the SNDL Inc. (NASDAQ:SNDL) share price has dived 25% in the last thirty days, prolonging recent pain. The recent drop has obliterated the annual return, with the share price now down 8.3% over that longer period.

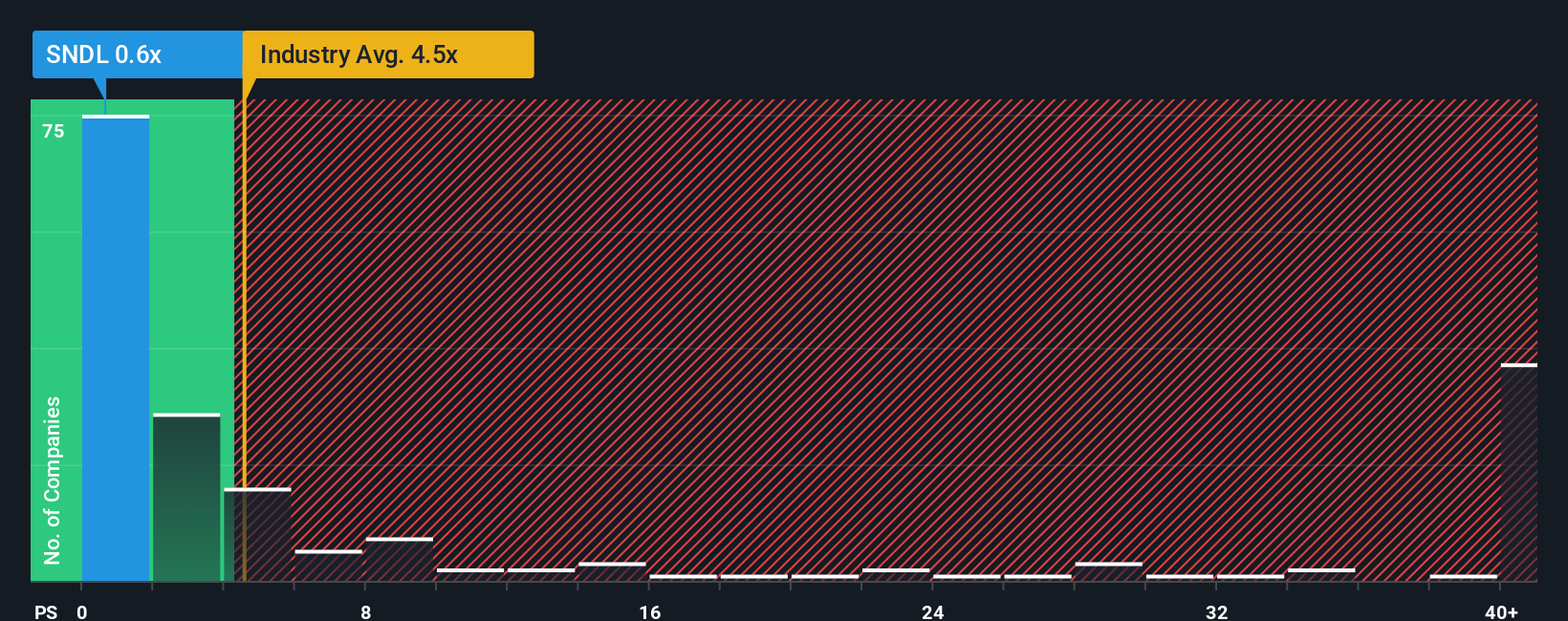

Since its price has dipped substantially, SNDL's price-to-sales (or "P/S") ratio of 0.6x might make it look like a strong buy right now compared to the wider Pharmaceuticals industry in the United States, where around half of the companies have P/S ratios above 4.5x and even P/S above 25x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

What Does SNDL's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, SNDL has been relatively sluggish. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on SNDL.Do Revenue Forecasts Match The Low P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as depressed as SNDL's is when the company's growth is on track to lag the industry decidedly.

If we review the last year of revenue growth, the company posted a worthy increase of 4.4%. This was backed up an excellent period prior to see revenue up by 92% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next three years should generate growth of 3.0% per year as estimated by the two analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 32% per annum, which is noticeably more attractive.

In light of this, it's understandable that SNDL's P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Having almost fallen off a cliff, SNDL's share price has pulled its P/S way down as well. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of SNDL's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.