Please use a PC Browser to access Register-Tadawul

Get It

Is Grainger's (GWW) Revised Earnings Outlook Reshaping the Long-Term Investment Case?

W.W. Grainger, Inc. GWW | 1197.65 | +1.23% |

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

To be a Grainger shareholder is to believe in the company’s established position as a leading MRO distributor benefiting from long-term infrastructure demand and supply chain digitalization trends. The recent Q2 results, with higher sales and ongoing buybacks, but slightly reduced earnings guidance, do not materially alter short-term catalysts, such as the company's capture of infrastructure-related demand, nor do they fundamentally change key risks like margin pressures from inflation or cost pass-through challenges.

Among the recent announcements, Grainger’s reaffirmed US$2.26 per share quarterly dividend stands out in the context of business resilience. This steady dividend, alongside robust cash flow and share repurchases, aligns with the company’s focus on rewarding shareholders, even as margin pressures and earnings volatility remain near-term considerations.

Yet, in contrast, investors should stay attentive to persistent cost inflation and gross margin pressure, which could have an outsized impact if supply chain complexity...

W.W. Grainger's outlook anticipates $21.3 billion in revenue and $2.3 billion in earnings by 2028. This is based on a projected annual revenue growth rate of 6.7% and an increase in earnings of $0.4 billion from the current $1.9 billion.

Uncover how W.W. Grainger's forecasts yield a $1047 fair value, a 10% upside to its current price.

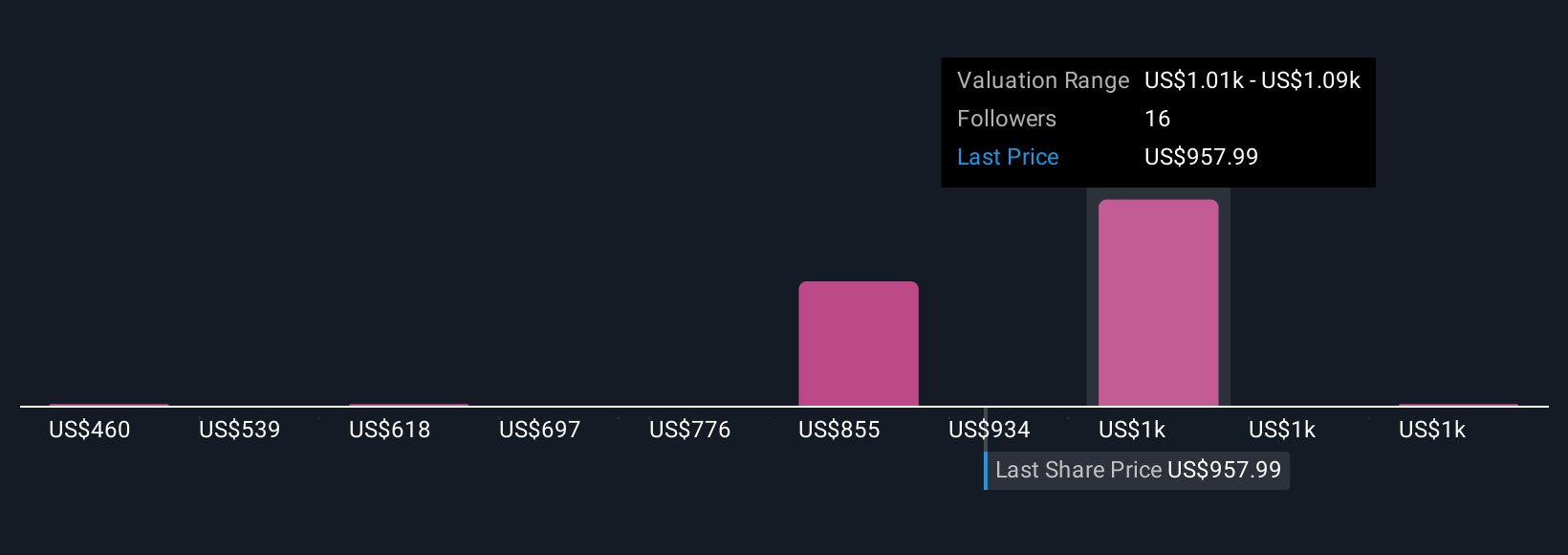

Simply Wall St Community members offered five fair value estimates for Grainger, ranging from US$460 to US$1,250 per share. While opinions differ widely, the recurring risk of margin compression due to inflation and pricing pressures remains a key concern that could influence results ahead.

Explore 5 other fair value estimates on W.W. Grainger - why the stock might be worth as much as 32% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.