Please use a PC Browser to access Register-Tadawul

Get It

Is It Time To Reassess Celsius Holdings (CELH) After Its Recent Share Price Volatility

Celsius Holdings, Inc. CELH | 39.65 39.89 | -4.48% +0.60% Post |

Celsius Holdings scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

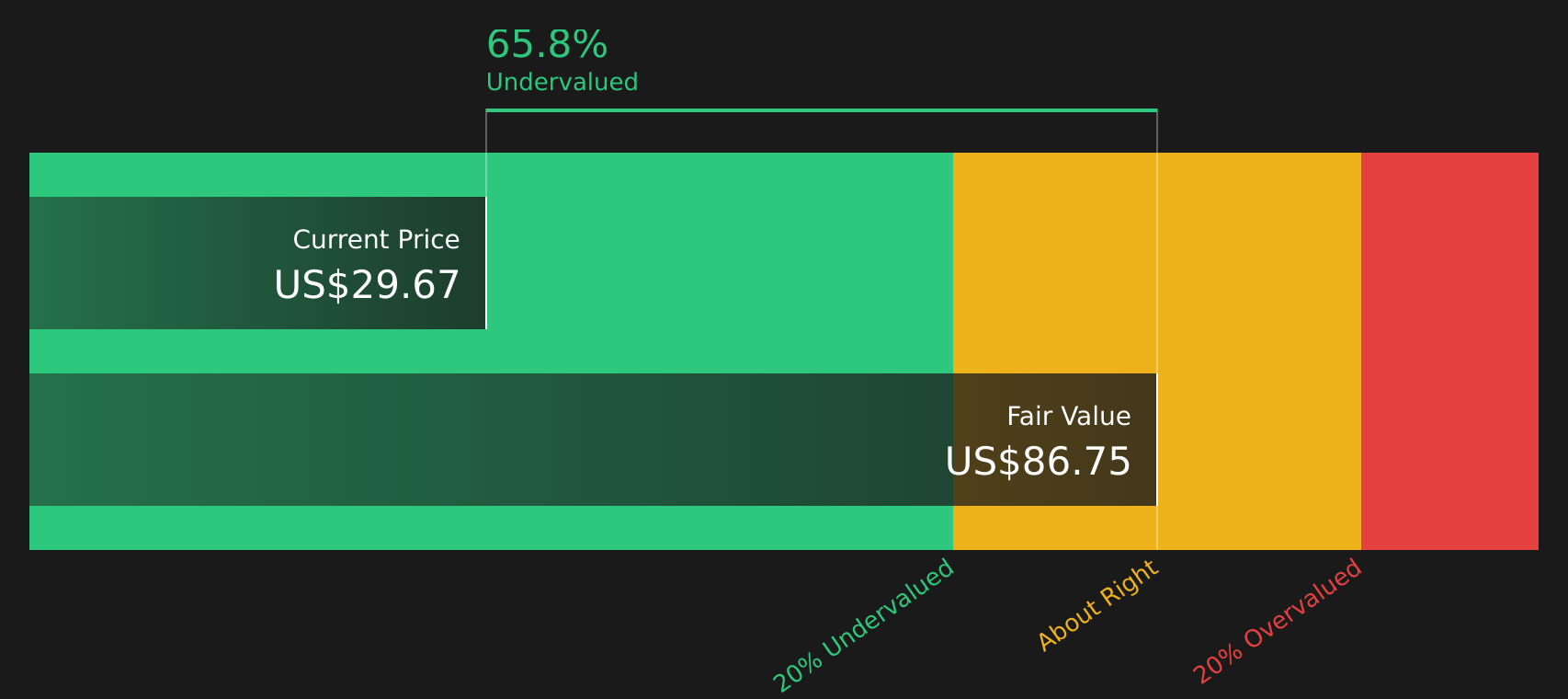

A Discounted Cash Flow, or DCF, model takes projected future cash flows and then discounts them back to today using a required rate of return to estimate what the business might be worth in total right now.

For Celsius Holdings, the model uses last twelve month free cash flow of about $322.2 million and a 2 Stage Free Cash Flow to Equity approach. Analysts have explicit forecasts for the next few years, with projected free cash flow in 2028 of $734.95 million. Beyond those analyst estimates, Simply Wall St extrapolates additional years, with discounted cash flow projections provided through 2035.

Adding these discounted cash flows together and adjusting for the share count leads to an estimated intrinsic value of about $108.08 per share, based on this DCF model description of cash flow projections. Compared with the recent share price of $45.57, this implies a DCF based discount of 57.8%, which indicates that the shares are trading below this model’s estimate of fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Celsius Holdings is undervalued by 57.8%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

For profitable consumer companies, P/S is often a useful cross check because it ties the share price directly to the revenue investors are paying for, regardless of short term swings in margins or one off items in earnings.

In simple terms, higher growth and lower perceived risk usually justify a higher P/S multiple, while slower growth and higher uncertainty tend to point to a lower, more conservative range. That is why comparing a company only to a single sector average can be misleading for a business with different prospects or risk levels.

Celsius currently trades on a P/S of 4.66x, compared with the Beverage industry average of 2.21x and a peer average of 1.72x. Simply Wall St’s Fair Ratio for Celsius, which blends in factors like earnings growth, profit margins, industry, market cap and company specific risks, is 3.16x. This Fair Ratio aims to be a more tailored yardstick than a broad industry or peer comparison, because it adjusts the expected multiple for the company’s own profile rather than assuming it should match the rest of the group.

On this basis, Celsius’ actual P/S of 4.66x sits above the Fair Ratio of 3.16x, suggesting the shares are trading at a richer level than this model would indicate.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St you can use Narratives, which are short, structured stories that link your view of Celsius Holdings to specific assumptions for future revenue, earnings and margins, and then to a fair value you can compare with the current price. Each Narrative lives on the Community page where millions of investors share their views, and the fair value updates automatically when new news or earnings arrive. For Celsius you might see one Narrative that lines up with the most optimistic fair value of US$80.00 and another that is closer to the lowest analyst view of about US$41.79. By choosing which story you agree with, you can quickly decide if today’s price near the recent US$45.57 level looks high, low or about right for your own decision making.

For Celsius Holdings, however, we will make it really easy for you with previews of two leading Celsius Holdings Narratives:

These are short, data backed stories created from analyst expectations so you can quickly see which version of the future feels closer to your own view before you go any further.

Fair value in this bullish Narrative: US$64.00

Implied discount vs the recent US$45.57 share price: about 28.8% undervalued using this Narrative framework

Assumed annual revenue growth: 21.81%

Fair value in this bearish Narrative: about US$41.79

Implied premium vs the recent US$45.57 share price: about 9.1% overvalued using this Narrative framework

Assumed annual revenue growth: 19.19%

Both Narratives use explicit assumptions for revenue, margins, P/E and discount rates, so the next step is to decide which story feels closer to how you see Celsius playing out, then adjust those inputs to reflect your own expectations before acting on the stock.

Do you think there's more to the story for Celsius Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.