Please use a PC Browser to access Register-Tadawul

Get It

Is Parsons' (PSN) Revenue Guidance Cut Offset by New Contracts and Acquisitions?

Parsons PSN | 66.66 66.66 | -1.77% 0.00% Post |

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

To own Parsons stock, an investor needs to believe in the company’s ability to capitalize on large-scale defense and infrastructure spending, especially as government modernization and global security demands rise. The recent downward revision in revenue guidance highlights some near-term challenges, but the major contract wins in the Middle East help balance concerns, suggesting the most important catalysts and risks remain unchanged for now.

Among recent developments, Parsons' more than US$100 million in new Middle East contract wins is particularly relevant. These awards underpin efforts to diversify revenue beyond the U.S. federal market, reinforcing one of the main catalysts, reducing reliance on U.S. government cycles while broadening exposure to international mega projects and national security work.

Yet, in contrast to the positive contract momentum abroad, investors should be conscious of the risk tied to abrupt U.S. federal funding shifts and how sudden program changes might...

Parsons' narrative projects $7.4 billion revenue and $350.2 million earnings by 2028. This requires 3.7% yearly revenue growth and a $102.6 million earnings increase from $247.6 million.

Uncover how Parsons' forecasts yield a $91.11 fair value, a 6% upside to its current price.

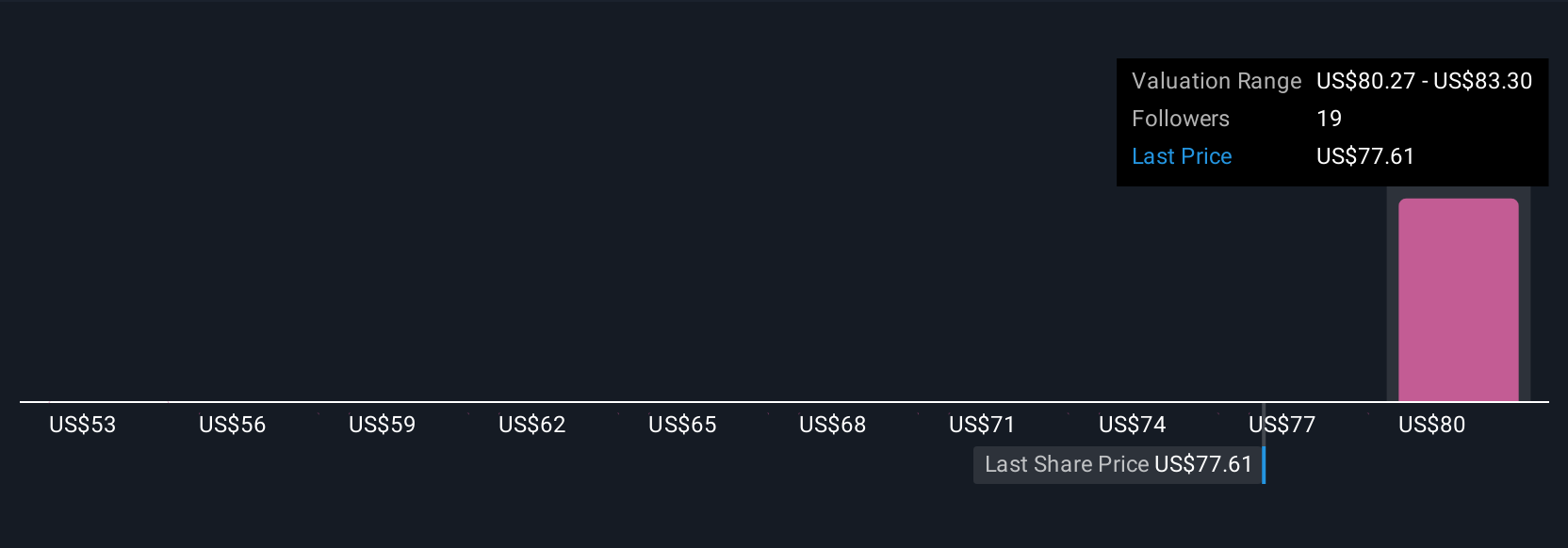

The Simply Wall St Community’s three fair value estimates for Parsons range from US$81.71 to US$115.70 per share. While some see potential for continued global expansion, others caution that reliance on government contracts may affect future returns, perspectives worth weighing side by side.

Explore 3 other fair value estimates on Parsons - why the stock might be worth just $81.71!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.