Please use a PC Browser to access Register-Tadawul

Get It

Is Photronics (PLAB) Using Its Buyback And Guidance To Quietly Reframe Its EPS Story?

Photronics, Inc. PLAB | 34.50 34.50 | +2.83% 0.00% Pre |

Find 46 companies with promising cash flow potential yet trading below their fair value.

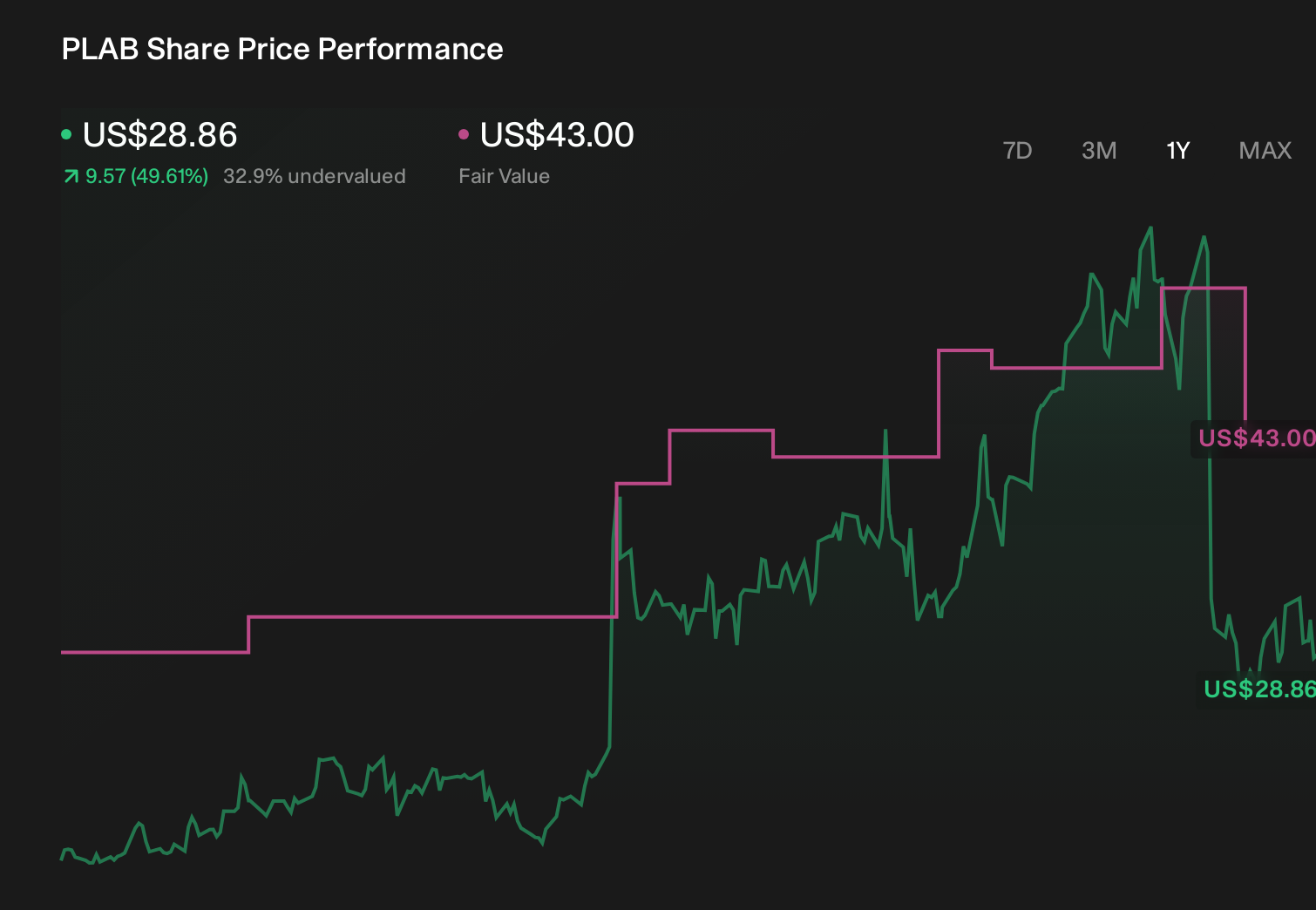

To own Photronics today, you need to be comfortable with a business that ties its fortunes to semiconductor and display mask demand, while managing heavy investment needs and cyclical swings in orders. The latest first quarter results and second quarter revenue guidance do not materially change the near term story: the key catalyst remains how effectively Photronics converts its advanced capacity investments into resilient earnings per share, while the biggest risk is that volatile design activity and limited backlog visibility translate into choppy quarterly results.

The most relevant update here is management’s second quarter fiscal 2026 revenue guidance of US$212 million to US$220 million, which effectively resets near term expectations after a first quarter of US$225.07 million in sales. With the multi year buyback now completed and no recent repurchases in the latest tranche, the focus shifts back to how topline delivery against this guidance supports earnings per share in a business where short booking windows can quickly reveal emerging softness in...

Photronics’ narrative projects $950.2 million revenue and $131.6 million earnings by 2028. This requires 3.5% yearly revenue growth and a roughly $23.1 million earnings increase from $108.5 million today.

Uncover how Photronics' forecasts yield a $42.00 fair value, a 23% upside to its current price.

Eight members of the Simply Wall St Community value Photronics between US$19.43 and US$42 per share, highlighting very different views on its earnings power. You can weigh those against the risk that Photronics’ limited 1 to 3 week order backlog makes quarterly revenue and profit swings more abrupt than many investors might expect.

Explore 8 other fair value estimates on Photronics - why the stock might be worth 43% less than the current price!

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.