Please use a PC Browser to access Register-Tadawul

Get It

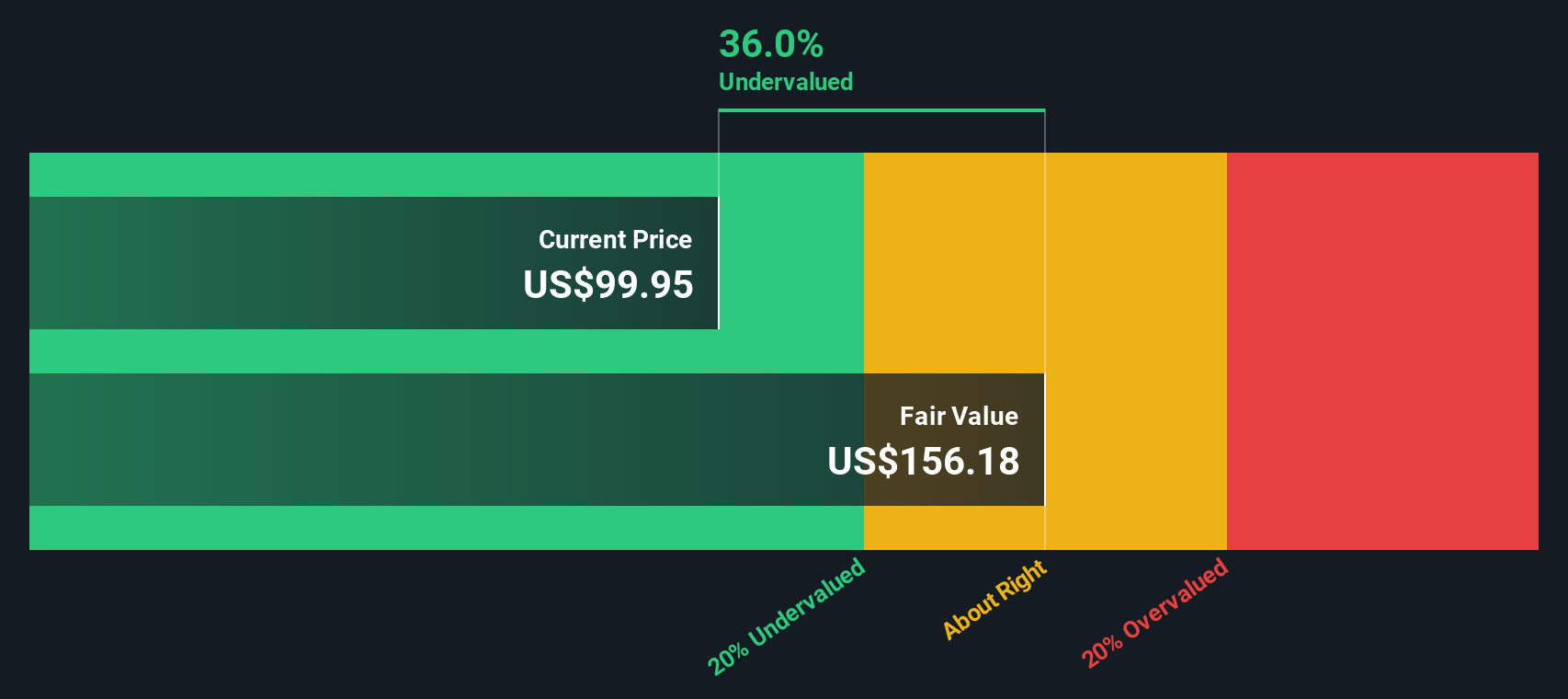

Is There Opportunity in Booz Allen Hamilton After Recent 20% Share Price Drop?

Booz Allen Hamilton Holding Corporation Class A BAH | 81.43 81.43 | -0.56% 0.00% Pre |

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future free cash flows and discounting those back to today’s dollars. This approach aims to capture the worth of all expected future cash the business will generate, bringing it to present value using a suitable discount rate.

For Booz Allen Hamilton, current free cash flow stands at $818 million. Analyst forecasts suggest free cash flow is expected to grow steadily, reaching $972 million by the fiscal year ending March 2028. Projections extended out over the next decade estimate free cash flow rising to about $1.27 billion by 2035, with early years based on analyst consensus and later years extrapolated from recent trends.

Based on this 2-stage free cash flow to equity model, Booz Allen Hamilton’s intrinsic value is calculated at $166.39 per share. This figure is 52.0% higher than the current trading price, implying the stock is significantly undervalued according to the DCF analysis.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Booz Allen Hamilton Holding is undervalued by 52.0%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

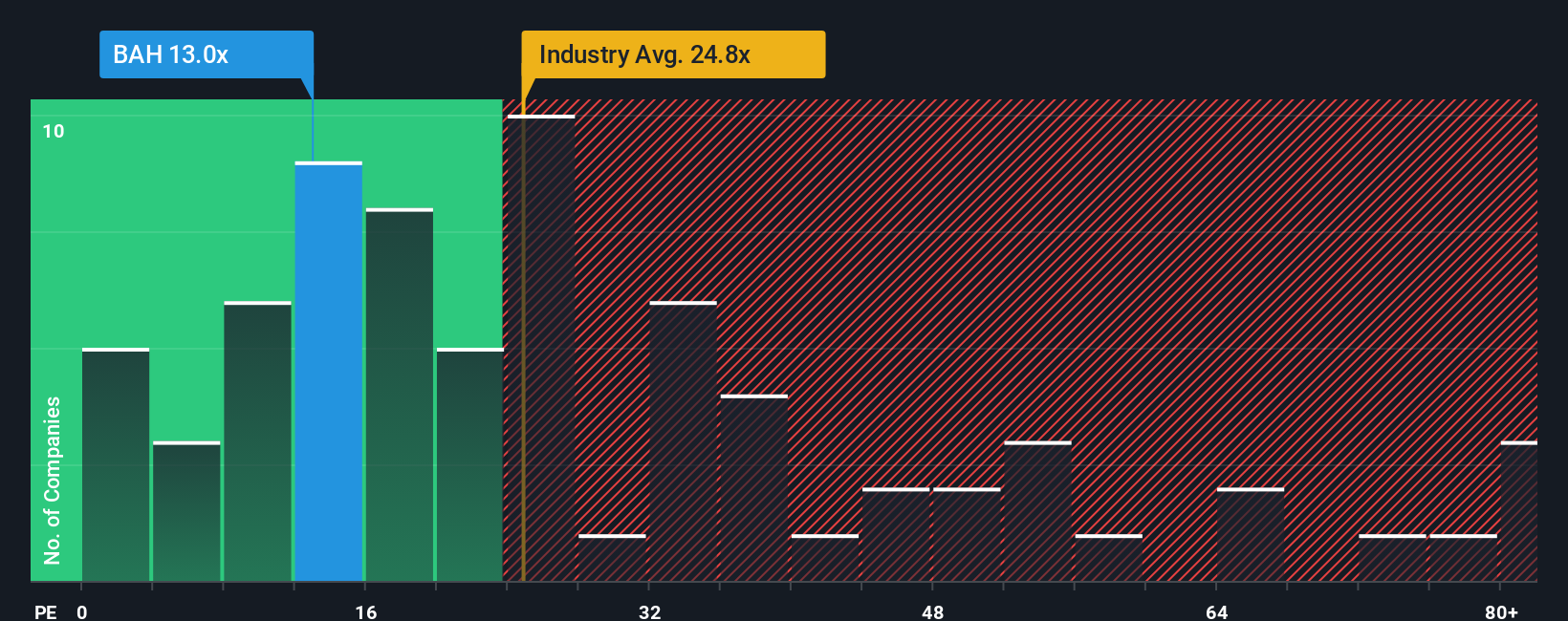

The Price-to-Earnings (PE) ratio is widely recognized as a go-to valuation metric for profitable companies like Booz Allen Hamilton Holding. It connects a company’s share price to its per-share earnings, giving investors a standardized way to compare value across businesses that are actually generating profits.

The "right" PE ratio for a stock depends on the market’s outlook for its future earnings growth as well as its risk profile. Higher growth prospects typically warrant higher PE ratios, while more uncertainty or risk can drag them down. So, looking only at headline PE numbers can sometimes be misleading without a deeper context.

Booz Allen Hamilton is currently trading at a PE ratio of 11.8x, well below the industry average of 23.7x and the average of its listed peers at 37.7x. While these figures suggest the stock is significantly undervalued, not all companies truly deserve industry-average multiples due to differences in growth outlook, profitability, or risk.

This is where the Simply Wall St "Fair Ratio" comes into play. The Fair Ratio, which is 20.2x in Booz Allen Hamilton’s case, adjusts for key company-specific factors such as earnings growth, profit margins, industry trends, risk, and market capitalization. By doing so, it paints a more tailored and balanced picture than simply stacking the company up against peers or the broader sector alone.

Comparing the Fair Ratio (20.2x) to Booz Allen Hamilton’s current PE (11.8x) tells us the stock is trading significantly below what would be considered fair value based on its fundamentals. This indicates a notable undervaluation that could warrant a closer look from investors seeking value opportunities.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1424 companies where insiders are betting big on explosive growth.

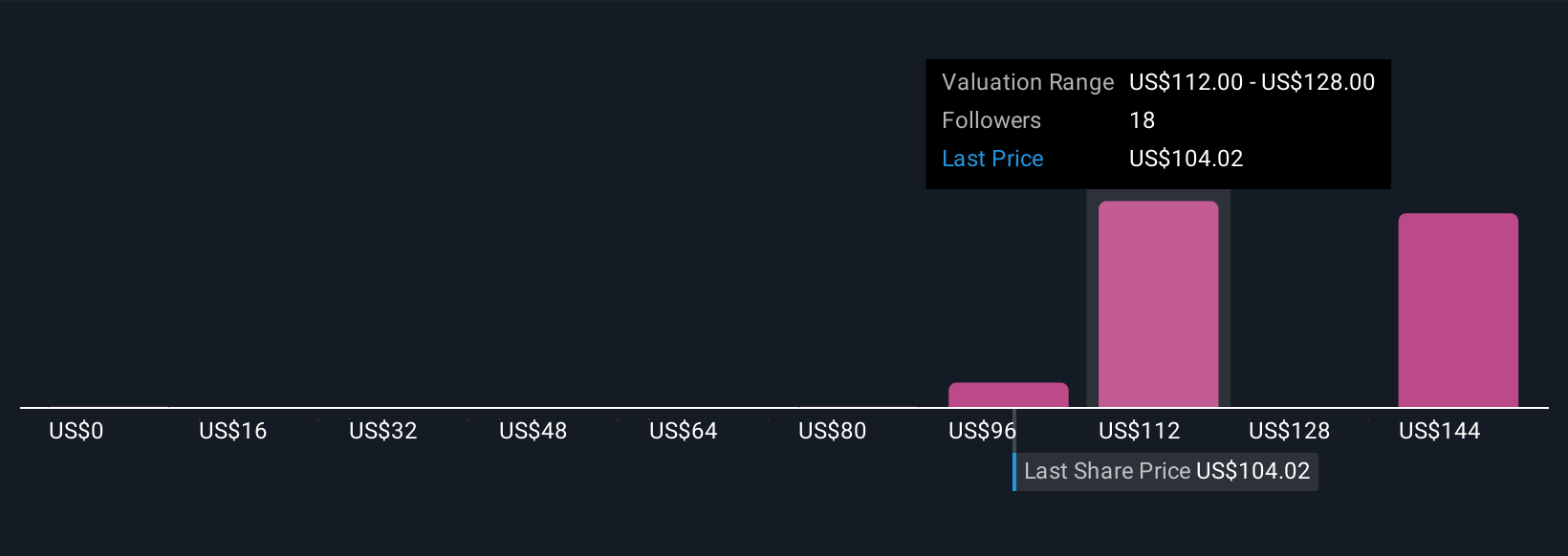

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. Narratives are a simple but powerful way to connect your view of Booz Allen Hamilton Holding’s future to the numbers by telling your version of the company’s story. You set out what you think will happen to revenue, earnings, and margins, then instantly see the impact on fair value.

Unlike traditional models, a Narrative turns your assumptions and opinions into a dynamic forecast, linking the story you believe in with a tangible valuation. This makes investment decision-making more accessible, as millions of users do on Simply Wall St’s Community page, whether you are a first-time investor or a seasoned pro.

Narratives also help clarify buy or sell opportunities by showing how your fair value compares to the current share price. When news or earnings updates arrive, your Narrative updates automatically so you can invest with confidence.

For example, one investor might see Booz Allen Hamilton securing new defense contracts and project a fair value above $160 per share, while another sees risks from contract delays and estimates value closer to $89. Narratives make it easy to turn your outlook into a concrete investment stance.

Do you think there's more to the story for Booz Allen Hamilton Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.