Please use a PC Browser to access Register-Tadawul

Get It

IZEA Worldwide, Inc. (NASDAQ:IZEA) Shares May Have Slumped 26% But Getting In Cheap Is Still Unlikely

IZEA Worldwide, Inc. IZEA | 3.44 3.44 | +3.30% 0.00% Pre |

The IZEA Worldwide, Inc. (NASDAQ:IZEA) share price has fared very poorly over the last month, falling by a substantial 26%. Longer-term, the stock has been solid despite a difficult 30 days, gaining 25% in the last year.

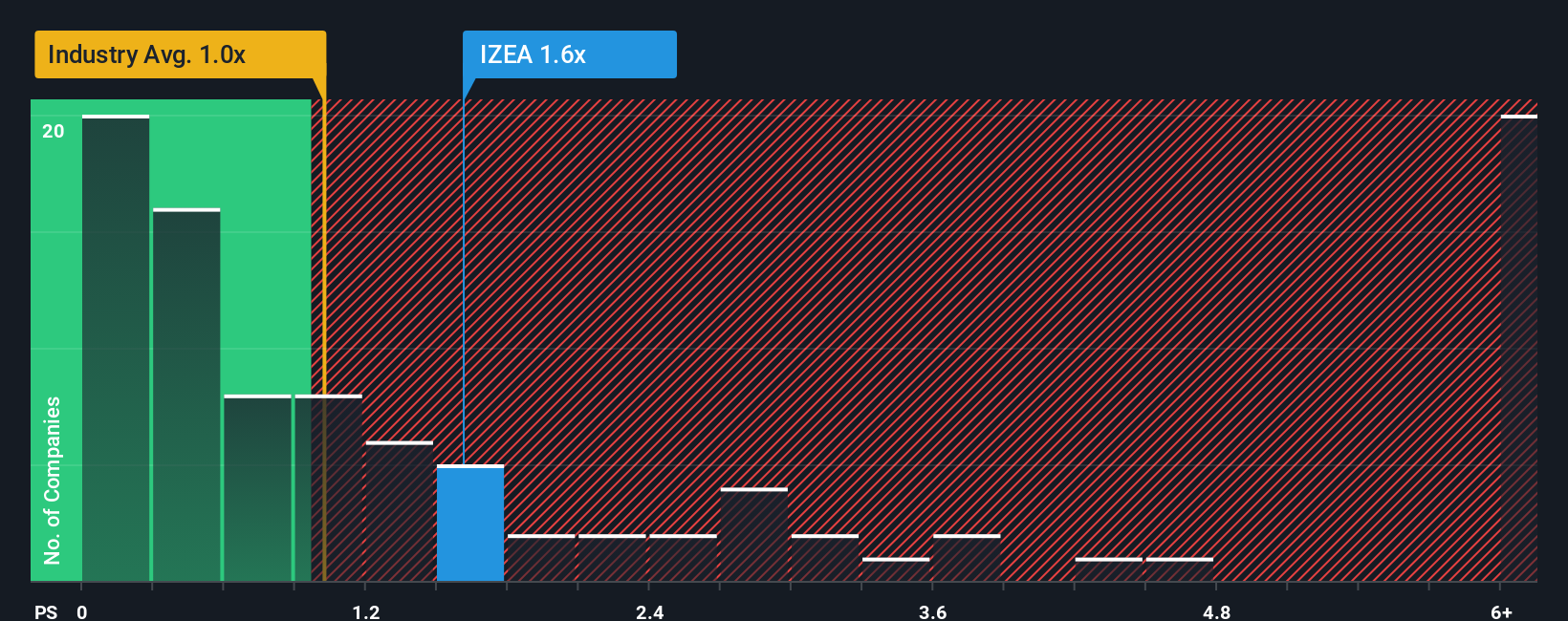

Although its price has dipped substantially, given close to half the companies operating in the United States' Interactive Media and Services industry have price-to-sales ratios (or "P/S") below 1x, you may still consider IZEA Worldwide as a stock to potentially avoid with its 1.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

IZEA Worldwide could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. If not, then existing shareholders may be very nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on IZEA Worldwide.There's an inherent assumption that a company should outperform the industry for P/S ratios like IZEA Worldwide's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 7.1%. Still, lamentably revenue has fallen 15% in aggregate from three years ago, which is disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue growth is heading into negative territory, declining 1.3% over the next year. That's not great when the rest of the industry is expected to grow by 18%.

With this information, we find it concerning that IZEA Worldwide is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a very good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

IZEA Worldwide's P/S remain high even after its stock plunged. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of IZEA Worldwide's analyst forecasts revealed that its shrinking revenue outlook isn't drawing down its high P/S anywhere near as much as we would have predicted. Right now we aren't comfortable with the high P/S as the predicted future revenue decline likely to impact the positive sentiment that's propping up the P/S. At these price levels, investors should remain cautious, particularly if things don't improve.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.