Please use a PC Browser to access Register-Tadawul

Get It

JPMorgan Chase (JPM) Expands Solo 401(k) Amid Buyback and Earnings Updates

JPMorgan Chase & Co. JPM | 315.55 317.29 | -1.40% +0.55% Pre |

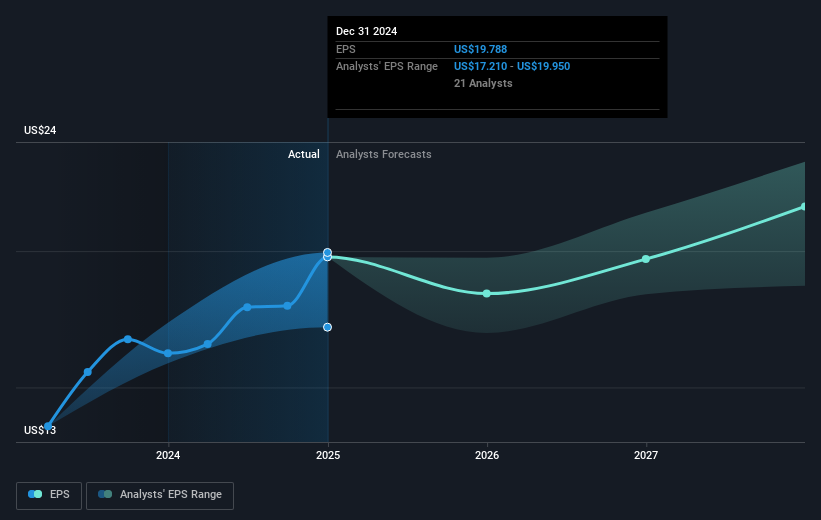

JPMorgan Chase (JPM) recently launched the Solo 401(k) and expanded its Everyday 401(k), reflecting its focus on retirement solutions for small business owners. Additionally, the company's share repurchase program saw significant activity, totaling $7.1 billion in the last quarter. These initiatives occurred alongside volatile stock trading amid criticism of Federal Reserve Chair Jerome Powell by former President Trump. JPM's share price increased by 25% this quarter as the market digested mixed earnings from financial institutions and broader market trends, suggesting these efforts added momentum to the company's performance.

The recent introduction of JPMorgan Chase's Solo 401(k) and expansion of its Everyday 401(k), along with the active share repurchase program, could influence the narrative by potentially boosting future revenue through a more robust retirement solutions offering. Despite higher credit loss allowances and expenses, these initiatives suggest an ongoing commitment to growing key business segments, which might cushion the impact on future earnings. Share repurchases further indicate confidence in capital allocation, potentially enhancing shareholder value while stabilizing earnings.

Over the past five years, JPMorgan Chase shares have delivered a substantial total return of 229.64%, highlighting strong long-term performance. This period of growth contrasts with the recent focus on credit loss provisions and expense increases, raising questions about the sustainability of such returns if profitability pressures persist.

In the past year, JPMorgan Chase has outperformed both the US market, which returned 10%, and the US Banks industry, which returned 18.6%, showing its relative resilience. However, the projected challenges, such as reduced net interest income due to expected rate cuts, could exert pressure on revenue and earnings forecasts.

The current share price of US$286.55 shows a marginal discount of approximately 2.36% to the consensus analyst price target of US$293.32. Given varied analyst perspectives, with price targets ranging from a bearish US$195.37 to a bullish US$330.00, assessing the impact of recent developments and external conditions on the company's future performance remains pivotal. These factors would influence consensus forecasts for revenue and earnings as analysts weigh recent strategic moves against macroeconomic headwinds.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.