Please use a PC Browser to access Register-Tadawul

Get It

MainStreet Bancshares (MNSB) Return To Profitability Tests Cautious Community Narratives

MainStreet Bancshares, Inc. MNSB | 21.41 | -0.37% |

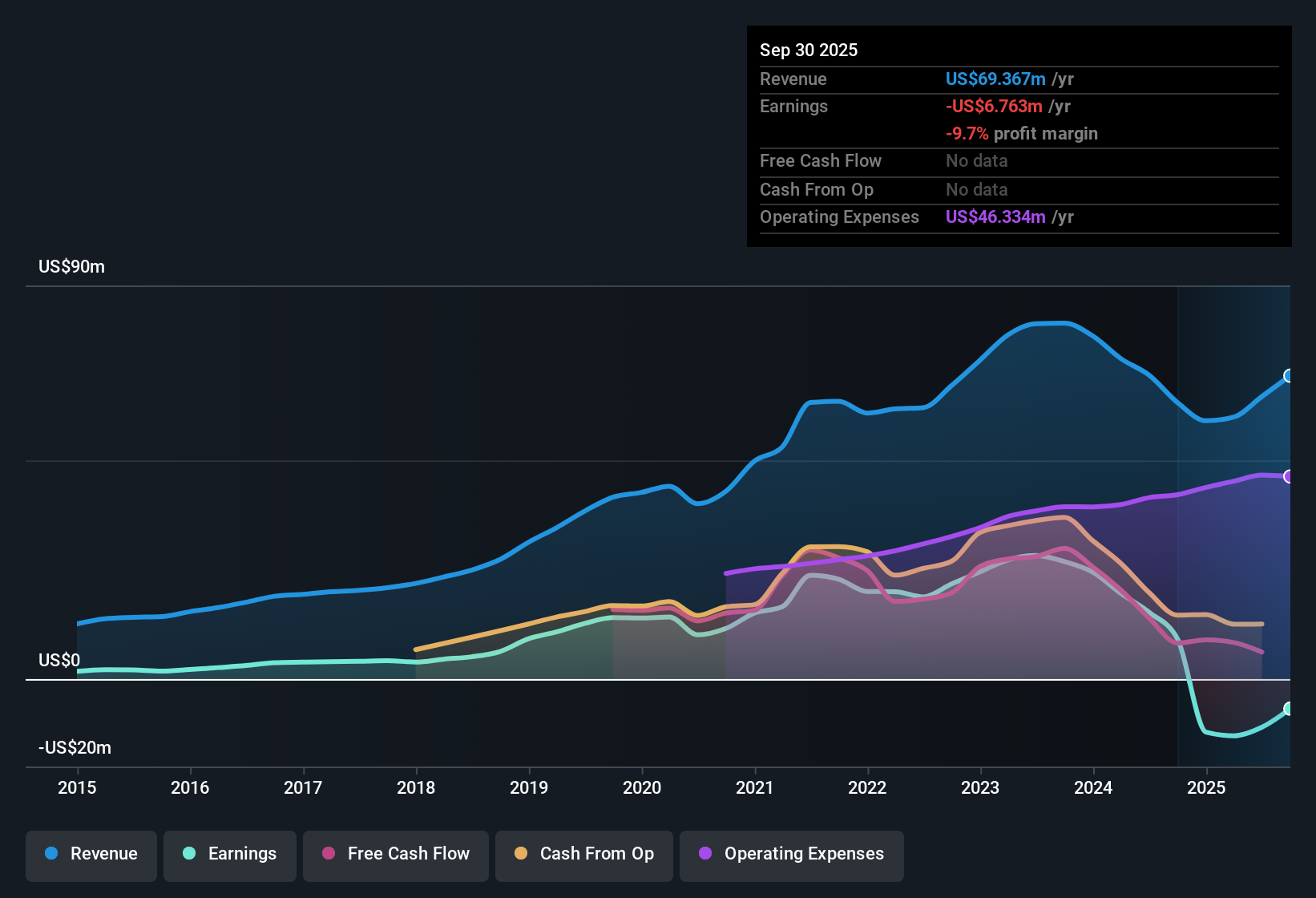

MainStreet Bancshares (MNSB) closed FY 2025 with fourth quarter revenue of US$17.7 million and EPS of US$0.46, alongside net income of US$3.5 million. These results put fresh numbers behind its recent return to profitability. The company has seen quarterly revenue move from US$13.4 million and EPS of a US$2.20 loss in Q4 2024 to US$17.7 million and EPS of US$0.46 in Q4 2025. Trailing twelve month EPS shifted from a loss of US$1.60 to a profit of US$1.76, setting up a discussion that is increasingly about the quality and resilience of margins rather than just getting back into the black.

See our full analysis for MainStreet Bancshares.With the latest results on the table, the next step is to see how these margin trends line up with the widely followed narratives around MainStreet Bancshares and where the fresh data challenges the current story.

To see how this earnings turn feeds into different long term growth stories and valuation angles, check the full market narrative around MNSB and how investors are framing the next few years. 📊 Read the full MainStreet Bancshares Consensus Narrative.

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on MainStreet Bancshares's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Despite the progress on profitability, questions around non performing loans, less than fully covered reserves and potentially weak dividend coverage highlight pressure on MainStreet Bancshares' balance sheet strength.

If you want banks where credit quality and resilience appear tighter, use our solid balance sheet and fundamentals stocks screener (389 results) to focus on companies with stronger cushions and fewer financial health red flags.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.