Please use a PC Browser to access Register-Tadawul

Get It

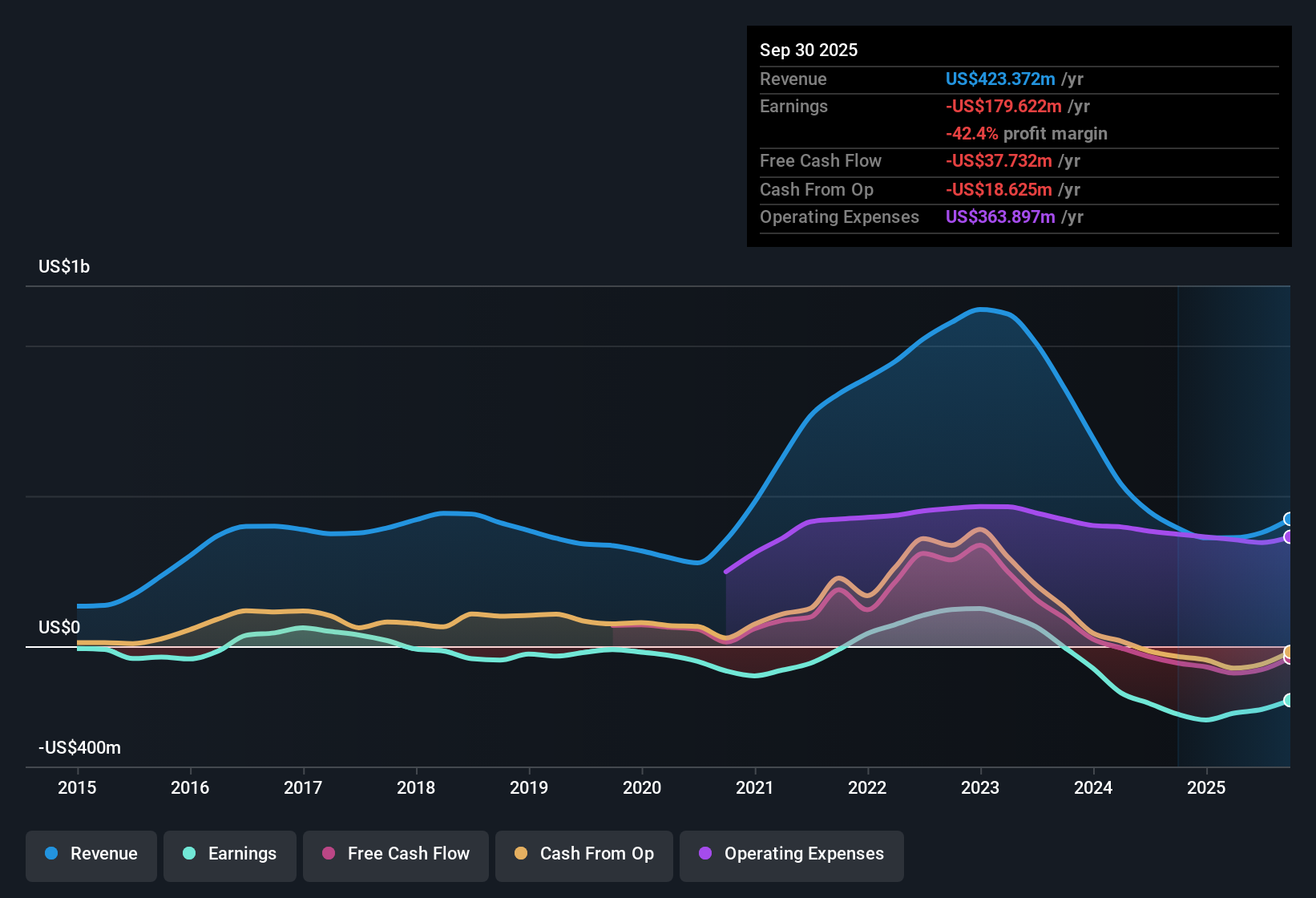

MaxLinear (MXL) Margin Loss Deepens, Challenging Bullish Narratives Despite Forecast 15.1% Revenue Growth

MaxLinear, Inc. Class A MXL | 17.41 | -6.25% |

MaxLinear (MXL) is set to outpace the broader US market with forecasted revenue growth of 15.1% per year, compared to a 10% industry average. Even with this top-line momentum, the company has remained unprofitable, and losses have deepened over the past five years at an average rate of 38.3% per year, with no meaningful improvement in margins. Shares currently trade at $15.62, well below the estimated fair value of $33.90, while the Price-To-Sales ratio of 3.2x sits under the industry’s 5.3x average but slightly above peers at 2.9x. Investors are weighing the rewards of discounted valuation and faster growth against persistent unprofitability and rising losses.

See our full analysis for MaxLinear.Next, we’ll see how the latest financial results stack up against the narratives that investors and analysts have built around MaxLinear. Sometimes these results reinforce existing perspectives, while other times they reshape them.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for MaxLinear on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Think you have a different take on MaxLinear's results? Share your perspective and shape your own view directly. Get started in just a few minutes. Do it your way

A great starting point for your MaxLinear research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

MaxLinear’s attractive revenue growth is overshadowed by persistent losses and ongoing margin pressure, making profitability uncertain for the foreseeable future.

If steady performance and predictable earnings matter to you, focus on companies showing consistent expansion and financial resilience by using our stable growth stocks screener (2098 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.