Please use a PC Browser to access Register-Tadawul

Get It

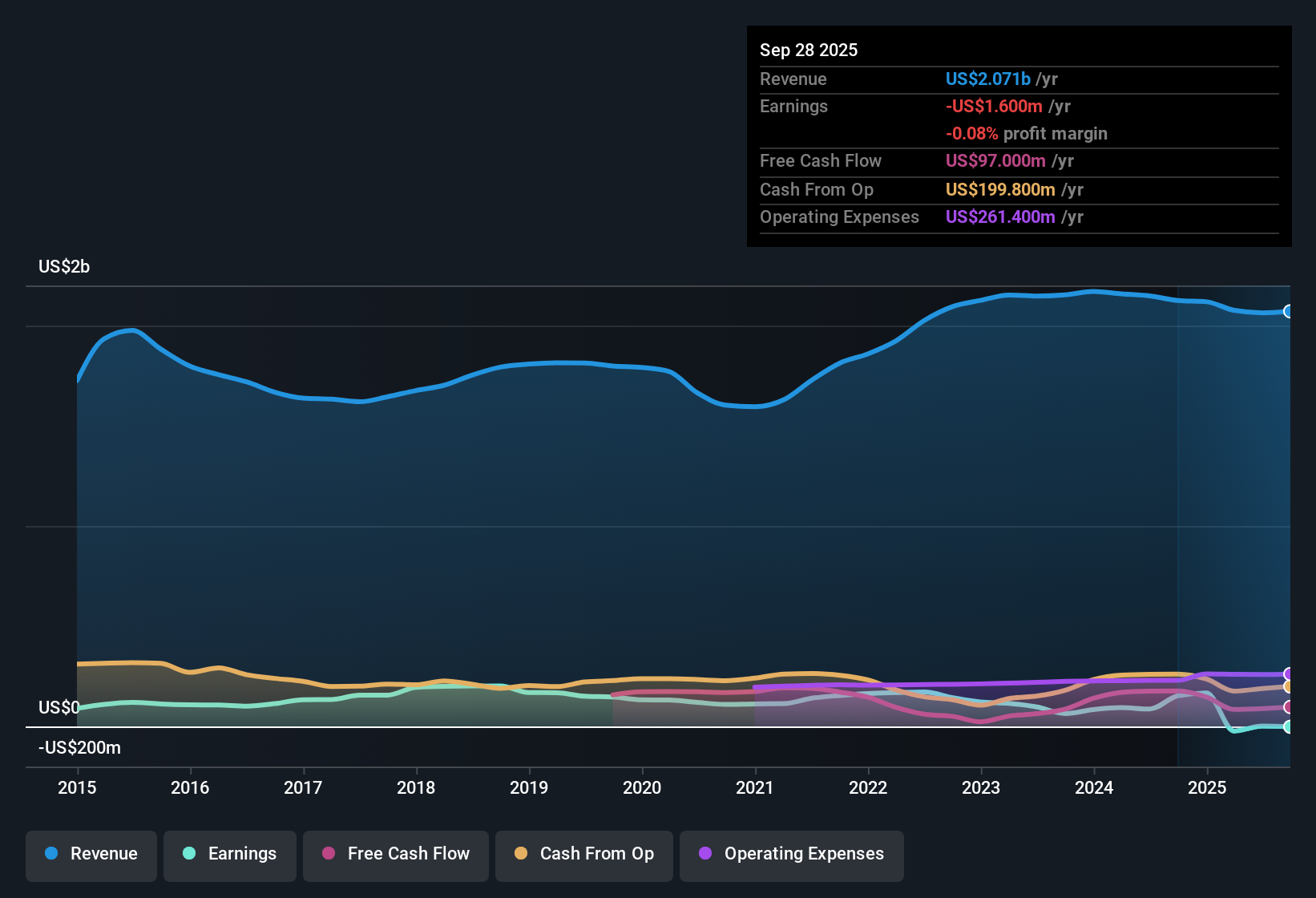

Minerals Technologies (MTX): Losses Deepen 19.9% Annually, Investor Focus Shifts to Profitability Path

Minerals Technologies Inc. MTX | 61.94 61.94 | +0.65% 0.00% Pre |

Minerals Technologies (MTX) is currently unprofitable, with losses deepening at an annual rate of 19.9% over the past five years. Looking forward, revenue is forecast to grow 3.4% each year and the company is expected to transition to profitability within three years. Earnings are projected to surge 246.7% annually. With these growth forecasts and a share price of $59.71, which sits below the consensus analyst target, investors are watching closely as MTX aims to return to the black and capitalize on its value-oriented positioning.

See our full analysis for Minerals Technologies.Now, let’s see how these latest earnings line up against the key narratives that have shaped community and market expectations for MTX.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Minerals Technologies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a different take on the data? Share your perspective and craft your own narrative in just a few minutes with ease: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Minerals Technologies.

Despite ambitious profit margin targets and upside potential, MTX’s exposure to declining paper demand and legal uncertainties introduces questions about its ability to deliver dependable growth.

If you want to sidestep these industry-specific risks, use stable growth stocks screener (2098 results) to focus on companies proving consistent gains and resilient earnings across market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.