Mueller Industries (MLI) just posted its latest FY 2025 numbers, with Q3 revenue of US$1.1 billion and basic EPS of US$1.91 setting the tone alongside trailing twelve month EPS of US$6.81. Over recent quarters the company has seen revenue move from US$997.7 million in Q2 2024 to US$923.5 million in Q4 2024, then up to US$1.0 billion in Q1 2025 and US$1.1 billion by Q3 2025. Quarterly EPS ranged from US$1.23 to US$2.26 over the same stretch as net income shifted between US$137.7 million and US$245.9 million. With a trailing net profit margin of 18.1%, the latest release lands as a clean, margin focused update that gives investors plenty to weigh up.

See our full analysis for Mueller Industries.

With the headline figures on the table, the next step is to see how these results line up with the widely followed narratives around Mueller Industries, including where the story is reinforced and where the numbers push back against expectations.

NYSE:MLI Earnings & Revenue History as at Feb 2026

18.1% margin backed by higher trailing EPS

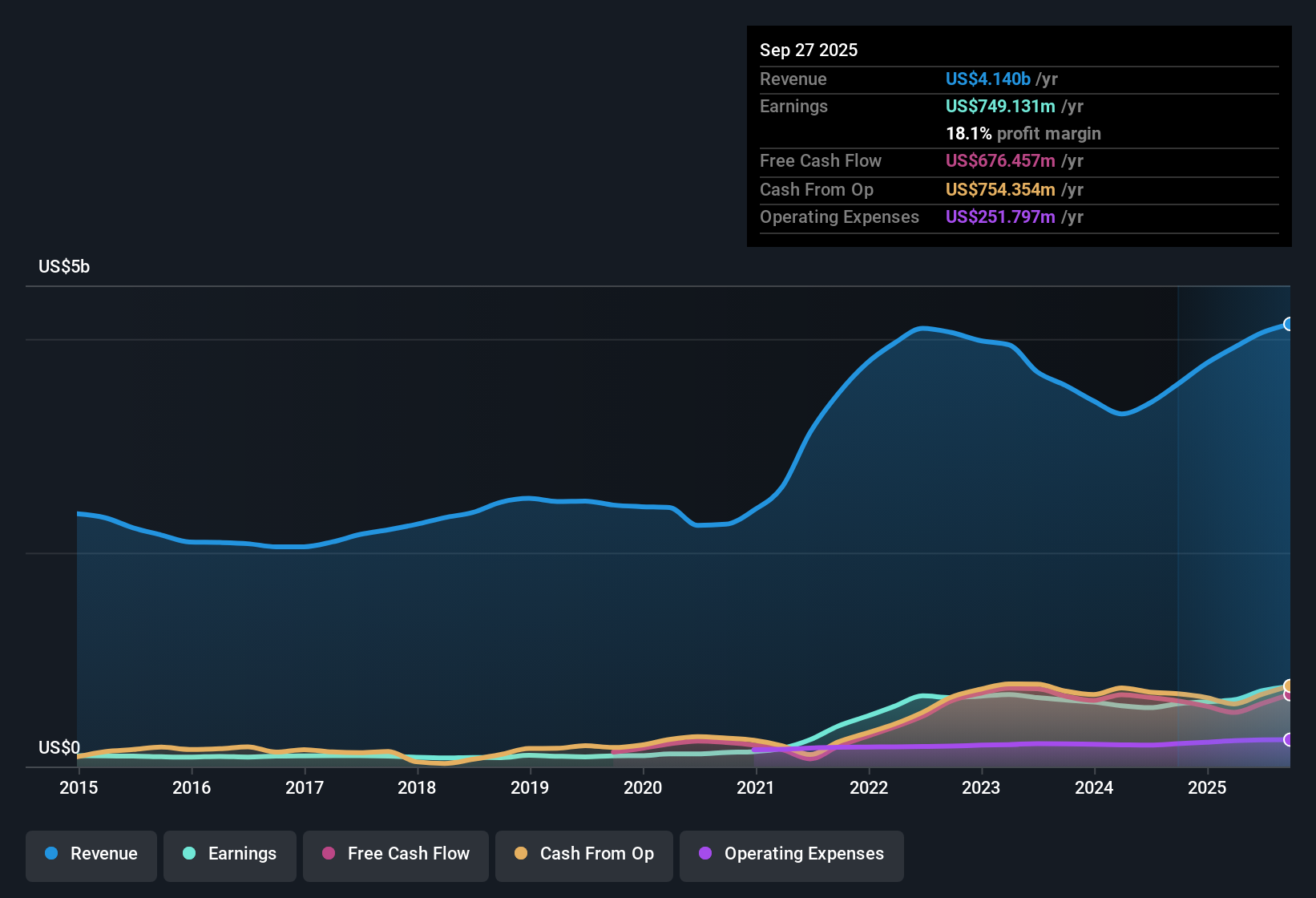

Over the last 12 months, Mueller Industries earned US$749.1 million of net income on US$4.1b of revenue, which translates to an 18.1% net margin and trailing EPS of US$6.81.

What stands out for the bullish narrative is that the 27.8% earnings growth over the year and 16.3% five year average earnings growth sit alongside that 18.1% margin. This supports the idea of a business supplying essential plumbing, metals, and climate components rather than one relying on one off gains.

Trailing revenue of US$4.1b and net income of US$749.1 million give some scale to the earnings base that bulls point to as a foundation for their view.

The margin comparison of 18.1% versus 16.4% the prior year is consistent with the bullish angle that profitability has been solid across the recent period covered by the data.

P/E of 18.3x versus industry 27.8x

The shares trade on a trailing P/E of 18.3x compared with the US Machinery industry at 27.8x and peers at 30x, with the stock price at US$123.65.

Supporters of the bullish view see this P/E gap and the DCF fair value of US$136.26 as evidence that the market is assigning a lower multiple than both peers and that model, even though trailing earnings grew 27.8% over the year.

The roughly 9.3% gap between the US$123.65 share price and the US$136.26 DCF fair value sits alongside the lower P/E. Together, these are used to argue there is room for sentiment to close that difference.

At the same time, the peer average P/E of 30x versus 18.3x for Mueller Industries highlights how the valuation is sitting below other machinery names even with the reported 16.3% five year earnings growth rate.

To see how valuation and fundamentals line up with different long term views on the stock, read the full narrative range for bulls, bears, and balanced investors.

📊 Read the full Mueller Industries Consensus Narrative.

Quarterly EPS swings inside a rising 12 month line

Across the last six reported quarters, basic EPS moved between US$1.23 and US$2.26, while the trailing 12 month EPS climbed from US$4.94 at Q2 2024 to US$6.81 at Q3 2025.

For investors weighing the general market opinion that Mueller Industries behaves like a steady, cyclical industrial name, the mix of quarter to quarter EPS shifts and a higher trailing 12 month EPS line fits with the idea of an underlying business tied to ongoing demand for piping systems, industrial metals, and climate products rather than a company driven mainly by short lived spikes.

Quarterly net income ranging from US$137.7 million to US$245.9 million across the period shows that while the individual quarters move around, the trailing 12 month net income still reached US$749.1 million by Q3 2025.

The trailing 12 month revenue path from US$3.4b at Q2 2024 to US$4.1b at Q3 2025 provides the backdrop for that earnings and margin profile that investors are assessing against the sector.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Mueller Industries's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Mueller Industries’ results pair solid trailing margins with noticeable quarter to quarter EPS swings, which may leave some investors wanting a smoother earnings profile.

If that choppiness makes you cautious, use our stable growth stocks screener (2196 results) to quickly focus on companies that show steadier revenue and earnings through different parts of the cycle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.