Please use a PC Browser to access Register-Tadawul

Get It

nLIGHT’s Capacity Expansion for Defense Lasers Might Change The Case For Investing In nLIGHT (LASR)

NLIGHT, INC. LASR | 56.01 | +0.59% |

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

To own nLIGHT, you need to believe its coherent beam-combined laser technology can translate defense demand into a sustainably larger, higher‑quality revenue base, even while the company remains unprofitable. The Longmont expansion is a clear signal that management expects continued, if not stronger, HEL orders from the U.S. Department of War and allied programs, and it could reinforce recent revenue momentum that already prompted raised Q4 2025 guidance. In the near term, key catalysts remain further contract awards, proof that higher capacity is actually filled, and continued progress in narrowing losses. On the risk side, the stock’s rich sales multiple, large insider selling and dependence on government budgets all look more important as the valuation has already rerated sharply. This new capacity raises the stakes on execution.

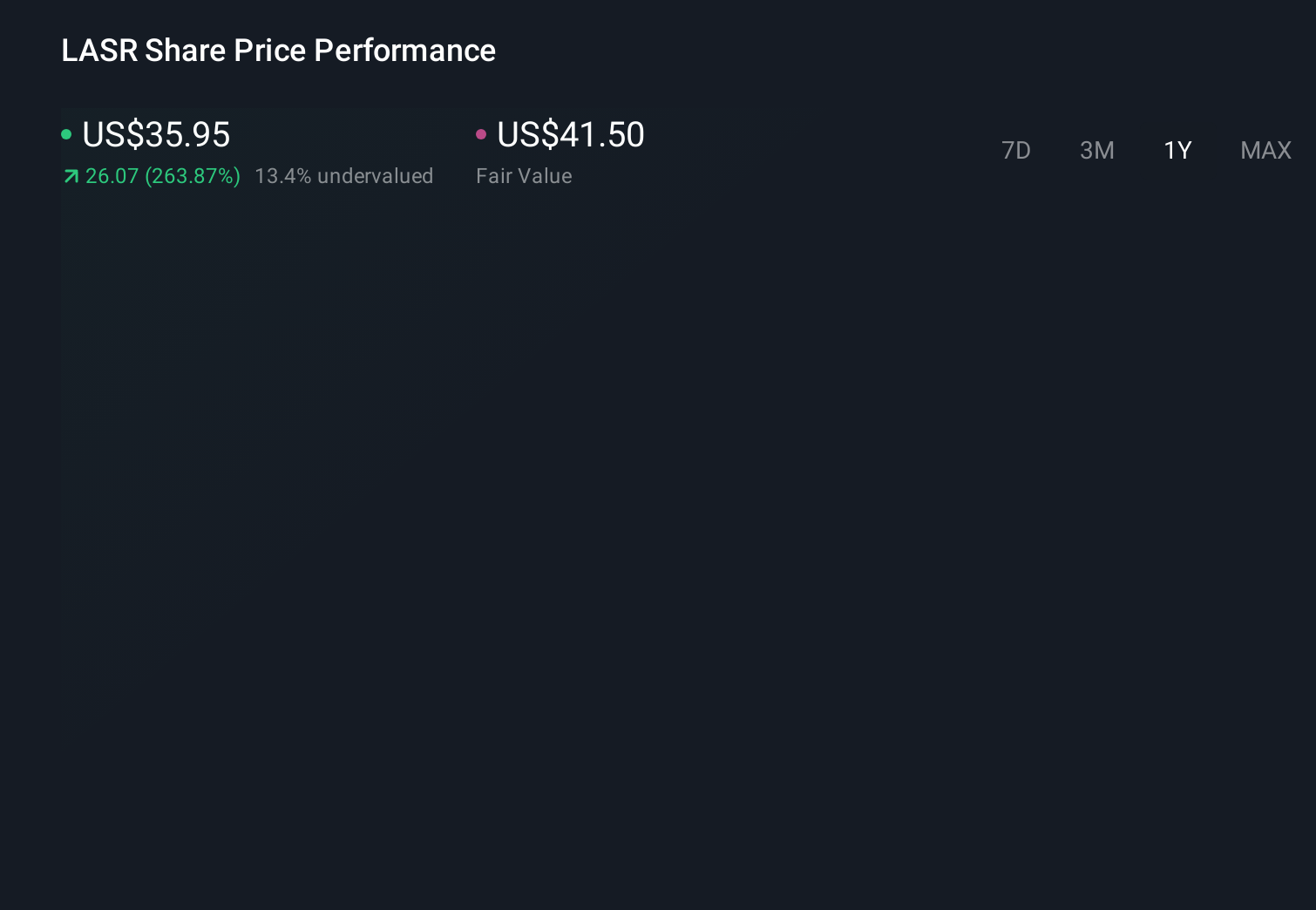

However, capacity is only an advantage if demand actually shows up. In light of our recent valuation report, it seems possible that nLIGHT is trading beyond its estimated value.

Three fair value views from the Simply Wall St Community span about US$17.70 to US$47.43, showing how far apart expectations sit. Set against nLIGHT’s steep valuation, ongoing losses and fresh capacity ramp, that spread underlines why it can pay to study several perspectives before forming your own view on the company’s prospects.

Explore 3 other fair value estimates on nLIGHT - why the stock might be worth as much as $47.43!

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.