Please use a PC Browser to access Register-Tadawul

Get It

O-I Glass (OI) Is Up 6.8% After Wave Of Analyst Upgrades Highlights Profit-Improvement Potential

O-I Glass Inc OI | 15.38 | +1.45% |

These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

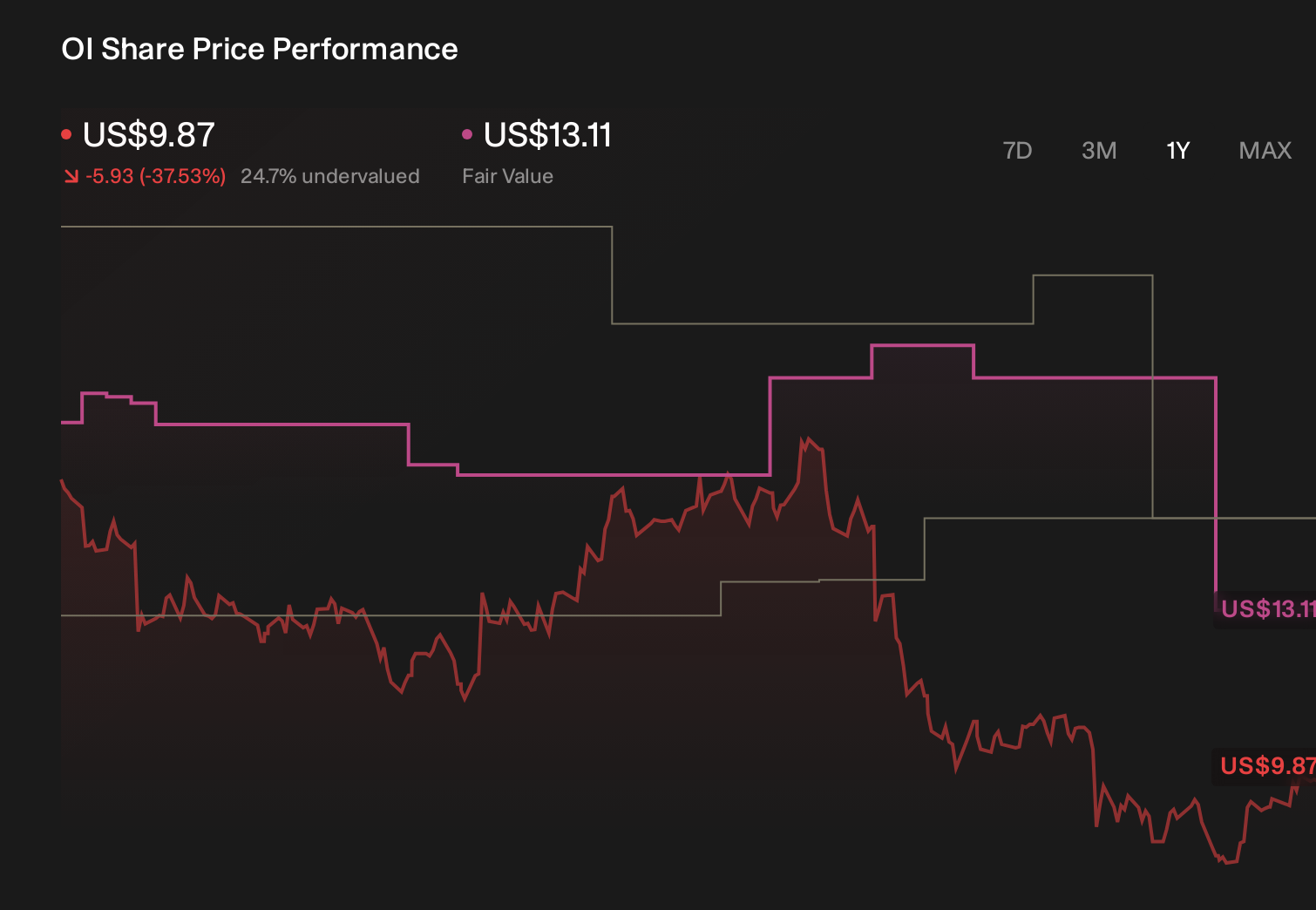

To own O-I Glass today, you need to believe that a leading global glass container producer can lift profitability mainly through internal efficiencies despite a tough packaging demand backdrop and recent earnings volatility. The cluster of analyst upgrades in early January 2026, led by Wells Fargo’s move to Overweight, supports that thesis but does not materially change the near term catalyst around self help profit improvement or the key risk of persistent volume softness in core markets.

The Wells Fargo upgrade, which raised its price target from US$15.00 to US$18.00, is especially relevant given O-I Glass’s recent results that showed modestly lower sales but a swing back to positive net income in Q3 2025. That combination of cost driven earnings progress and cautious commentary on a still challenging volume backdrop aligns closely with the current investment debate around whether efficiency gains can offset lingering demand and capacity risks.

Yet even as analysts turn more positive, investors should be aware that prolonged volume weakness in Europe could still...

O-I Glass' narrative projects $6.8 billion revenue and $385.1 million earnings by 2028. This requires 1.6% yearly revenue growth and a $640.1 million earnings increase from -$255.0 million today.

Uncover how O-I Glass' forecasts yield a $15.89 fair value, in line with its current price.

Two fair value estimates from the Simply Wall St Community span a wide range, from about US$15.89 to US$43.81 per share, showing how far apart individual views can be. When you set that against concerns about ongoing volume softness in key end markets, it underlines why many market participants are weighing both upside from internal improvements and the risk of weaker demand, and why it can help to explore several contrasting viewpoints.

Explore 2 other fair value estimates on O-I Glass - why the stock might be worth just $15.89!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.