Please use a PC Browser to access Register-Tadawul

Get It

Omnicell (OMCL) Is Up 10.2% After Reporting Q2 Revenue Growth and Updated 2025 Guidance - What's Changed

Omnicell, Inc. OMCL | 43.86 | +1.32% |

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

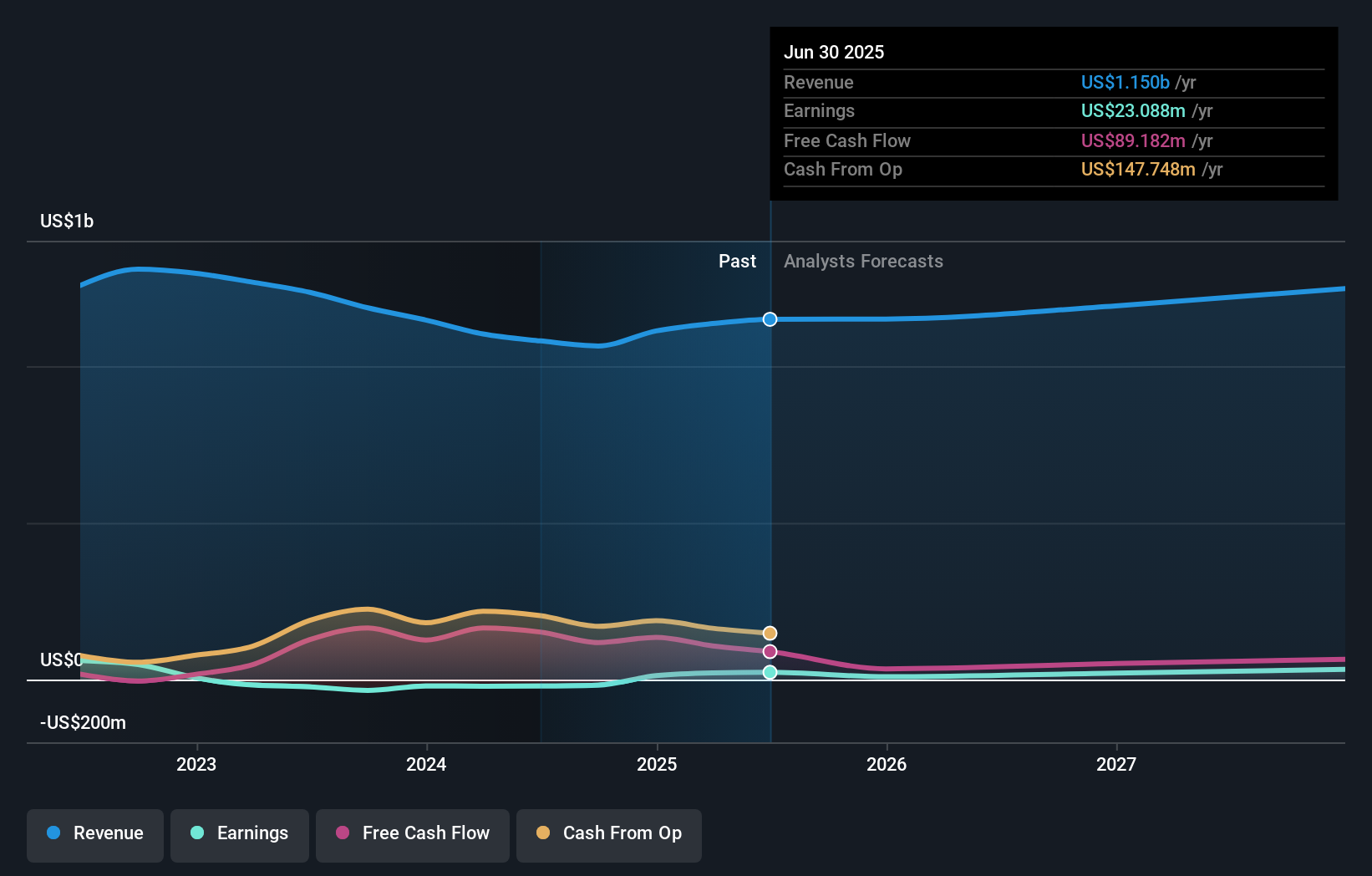

Owning Omnicell stock relies on the belief that healthcare systems will continue prioritizing automation and medication management, fueling steady growth in high-margin recurring revenues. The latest Q2 results, featuring higher revenues and improved net income, do help ease concern over profitability, but tariff risks and margin pressures from supply chain shifts remain the dominant short-term catalyst and risk; the outlined guidance does not meaningfully change that assessment.

Among recent announcements, the new share buyback program stands out, reflecting the company’s focus on shareholder value during an ongoing period of margin volatility. While buybacks can help support the share price or offset dilution, their significance is mostly symbolic when weighed against underlying operating hurdles and earnings unpredictability tied to tariffs and hardware market cycles.

However, investors should be aware that behind these financial improvements, the risk from ongoing US-China tariffs and Omnicell’s heavy China supply chain exposure remains...

Omnicell's outlook forecasts $1.2 billion in revenue and $10.5 million in earnings by 2028. This is based on a 2.9% annual revenue growth rate and a $10.7 million decrease in earnings from the current $21.2 million.

Uncover how Omnicell's forecasts yield a $43.83 fair value, a 41% upside to its current price.

Retail investors in the Simply Wall St Community all set Omnicell’s fair value at US$43.83, well above the recent market price. With tariff-related cost headwinds still at the forefront, opinions can differ widely, explore multiple viewpoints before making up your mind.

Explore another fair value estimate on Omnicell - why the stock might be worth just $43.83!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.