Please use a PC Browser to access Register-Tadawul

Get It

Oracle Certification Could Be a Game Changer for Vertex (VERX)

Vertex VERX | 19.91 | +0.05% |

Find companies with promising cash flow potential yet trading below their fair value.

Owning shares in Vertex means believing in the ongoing digitization of enterprise tax compliance, regulatory mandates for e-invoicing, and the company's ability to embed its cloud solutions within leading ERP platforms. While the Oracle Validated Integration certification confirms product credibility and scalability, the most important short-term catalyst remains the pace of enterprise cloud ERP migrations. However, this news does not meaningfully change the biggest risk currently facing Vertex: elongated enterprise sales cycles slowing revenue growth.

One recent announcement closely tied to this news was Vertex's June selection to join Oracle's enhanced partner program. This partnership strengthens Vertex's integration with Oracle ERP, supporting its push to win migration-driven adoption as cloud modernization efforts gather momentum, a key element in maintaining growth despite challenging sales cycles. In contrast, investors should be aware that risks also remain if...

Vertex's outlook anticipates $1.1 billion in revenue and $71.6 million in earnings by 2028. This is based on forecast annual revenue growth of 14.6% and a $122 million increase in earnings from the current $-50.4 million.

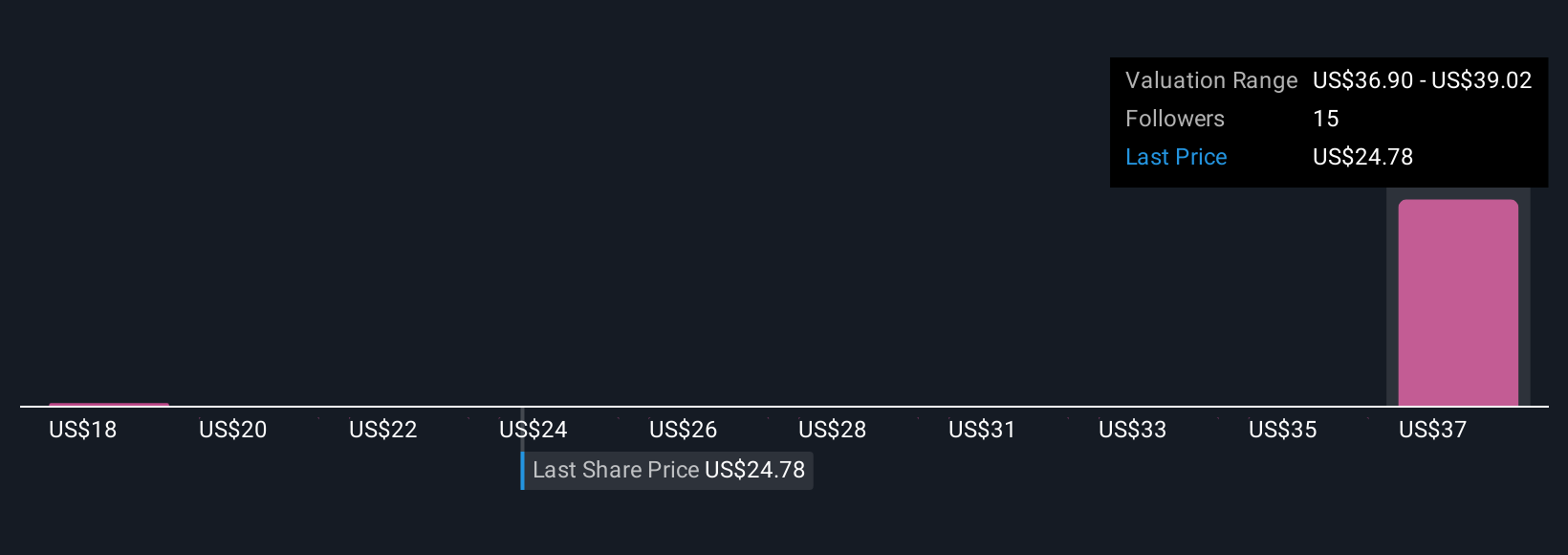

Uncover how Vertex's forecasts yield a $37.23 fair value, a 51% upside to its current price.

Simply Wall St Community members provided three fair value estimates for Vertex ranging from US$17.84 to US$39.12 per share. Despite these varied viewpoints, slowing enterprise sales cycles bring important considerations for the company’s near-term momentum and underline the value of exploring multiple perspectives.

Explore 3 other fair value estimates on Vertex - why the stock might be worth as much as 58% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.