Please use a PC Browser to access Register-Tadawul

Get It

Palo Alto Networks (PANW): Evaluating Valuation After Strong Earnings and New AI Security Partnerships

Palo Alto Networks, Inc. PANW | 168.91 168.91 | -0.17% 0.00% Pre |

Palo Alto Networks (PANW) delivered a strong quarterly earnings report, outpacing market forecasts thanks to continued revenue growth driven by its platform-centric model and steady expansion in subscription sales. The company’s fresh partnerships and next-generation AI security initiatives are also drawing renewed attention from investors and industry analysts alike.

Palo Alto Networks’ run of upbeat financials and headline-making alliances has not shielded the shares from volatility. Despite all the innovation and growth buzz, the stock has pulled back sharply this month, with a 1-month share price return of -13.68% and a year-to-date share price gain of just 2.4%. That said, long-term holders have still been well rewarded, as the total shareholder return sits at 113.8% over three years and 273.5% over five years. This suggests that momentum may be regrouping after a hot streak.

If you want to see which other technology leaders are at the forefront of cybersecurity, AI, and cloud, it’s worth checking out See the full list for free..

With shares recently sliding despite strong growth and ongoing innovation, the key question for investors is whether current weakness presents a rare window to buy into Palo Alto Networks at a compelling valuation, or if the market has already accounted for its impressive future prospects.

The widely-followed narrative points to a fair value that sits notably above Palo Alto Networks' last close price. This suggests a significant upside potential if consensus projections play out as planned.

Ongoing industry consolidation, as enterprises seek to simplify and maximize the effectiveness of their security stack, has strengthened the trend towards platformization. This has resulted in larger multi-platform deal sizes, improved cross-sell, higher net retention rates (120%), and near zero churn among platformized clients. All of these factors support future margin expansion and earnings growth.

Want to uncover the formula behind this bullish valuation? The fair value calculation is built on ambitious projections of growing recurring revenues, expanding margins, and transformative developments in cybersecurity AI. The narrative's confidence rests on assumptions you'd never guess from just looking at headline numbers. See which financial leap fuels the next phase of growth.

Result: Fair Value of $219.75 (UNDERVALUED)

However, significant integration challenges or regulatory hurdles could disrupt growth expectations and quickly alter the bullish outlook currently priced into Palo Alto Networks shares.

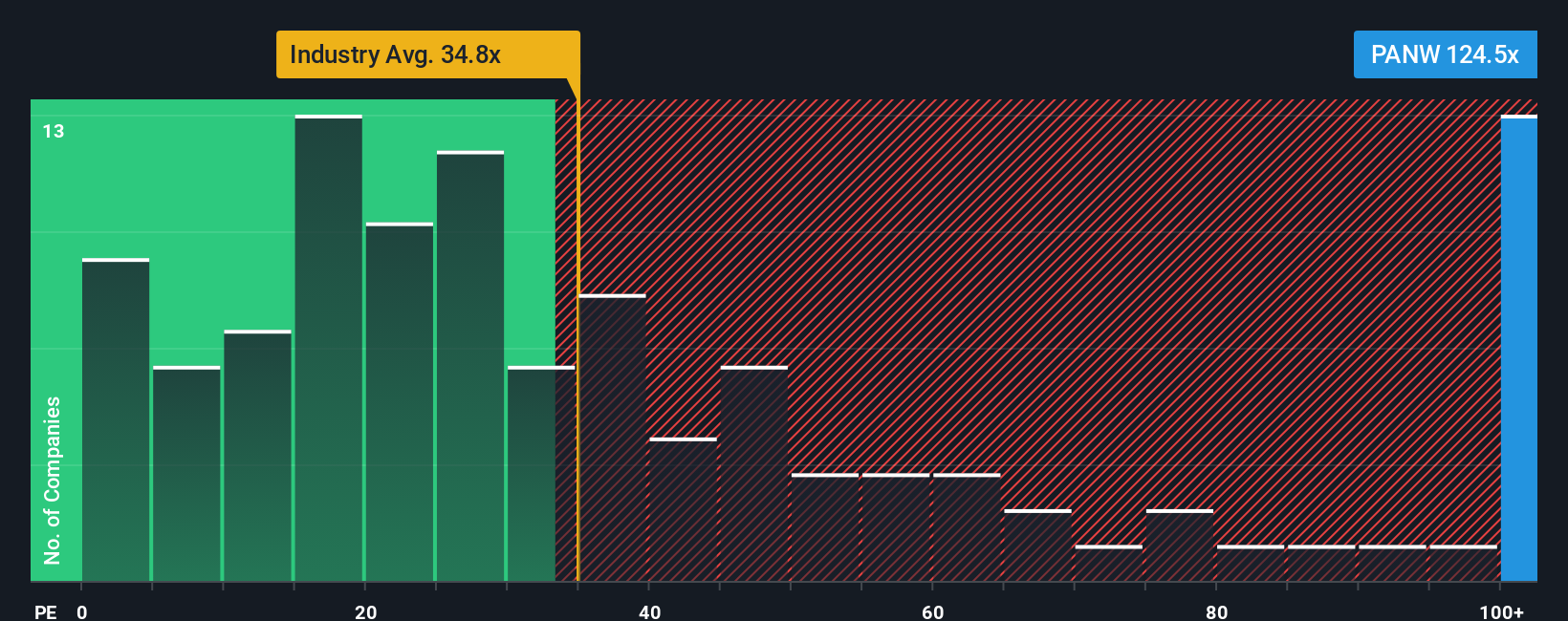

Checking Palo Alto Networks’ price against what similar companies fetch, the stock trades at a hefty 112.2x earnings, which is well above both the US Software industry average of 29x and its peers at 48.7x. Even the fair ratio suggests it could be as low as 46.4x. With such a gap, are investors pricing in too much future success, or could the company eventually grow into these expectations?

If you want to dig into the numbers and shape your own outlook, it only takes a few minutes to assemble a personal case for Palo Alto Networks. Do it your way

A great starting point for your Palo Alto Networks research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Don't let opportunity pass you by. Elevate your investing strategy by finding standout stocks tailored to your goals with these high-potential starting points from Simply Wall Street:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.