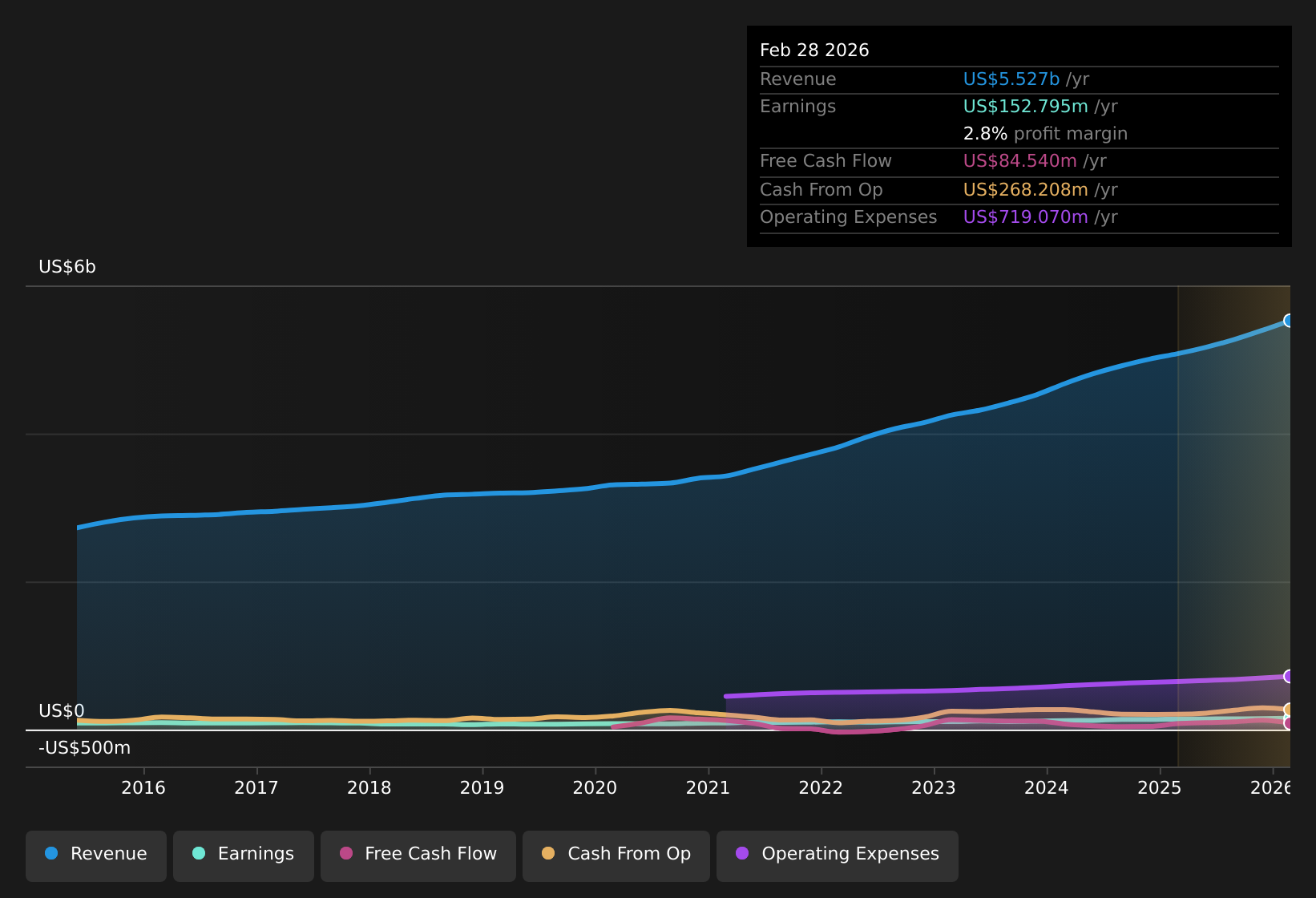

PriceSmart (PSMT) has just opened its 2026 financial year with Q1 same store sales growth of 8%, coming on the heels of Q4 2025 revenue of US$1.3 billion and basic EPS of US$1.02, alongside trailing twelve month EPS of US$4.82 on revenue of US$5.3 billion. The company has seen quarterly revenue move from US$1.26 billion in Q1 2025 to US$1.36 billion in Q2, then US$1.32 billion in Q3 and US$1.33 billion in Q4, while basic EPS over that stretch ranged from US$1.21 to US$1.45. This sets up Q1 2026 against a backdrop of steady top line and earnings delivery. With trailing net margins essentially flat and same store sales growth holding up, investors are likely to read this print through the lens of how efficiently PriceSmart is turning that sales base into sustainable profitability.

See our full analysis for PriceSmart.

With the headline numbers on the table, the next step is to see how this latest quarter lines up against the key bullish and bearish narratives that have formed around PriceSmart over the past year.

NasdaqGS:PSMT Earnings & Revenue History as at Jan 2026

8% same store sales growth backs expansion story

Same store sales growth stepped up to 8% in Q1 2026, compared with 7% in Q3 2025 and 6.7% in Q2 2025, while trailing twelve month revenue reached about US$5.3b.

Consensus narrative leans bullish on club rollouts and membership growth, and this sales trend gives some support but also raises a question on execution:

On the one hand, 8% same store sales growth, plus trailing twelve month sales of about US$5.3b, fits the view that new clubs, private label penetration near 28% of merchandise sales, and growing digital channels over 6% of merchandise sales are feeding a larger, more engaged customer base.

On the other hand, with analysts expecting revenue growth of about 8% a year, the current 8% same store number leaves limited room for missteps if new clubs or logistics upgrades in regions like Central America and Colombia do not keep pace with that assumption.

Margins at 2.7% keep profitability in focus

Trailing net profit margin sits at 2.7%, slightly below last year’s 2.8%, alongside trailing twelve month net income of about US$144.9m on US$5.3b of revenue.

Critics highlight FX and cost pressures as a bearish point, and the margin data partly lines up with that concern:

Bears point to FX and liquidity issues in markets like Trinidad and Honduras, and trailing margins at 2.7% against 2.8% last year show limited buffer if unrealized losses on U.S. dollar assets or higher landed costs keep weighing on earnings.

At the same time, trailing EPS of US$4.82, five year earnings growth of 10.8% a year, and a 1.89% dividend suggest the business is still earning enough on its cost base to support ongoing investment in logistics and digital sales even with slightly tighter margins.

Stay on top of how FX pressures and cost trends could reshape the cautious view on PriceSmart’s profitability story.

🐻 PriceSmart Bear Case

Premium valuation versus US$86.45 DCF fair value

With the share price at US$133.43, PriceSmart is trading above a stated DCF fair value of US$86.45 and on a P/E of 27.7x versus peer and industry averages of 20.4x and 23.5x.

Supporters with a bullish tilt often point to high quality earnings and a 1.89% dividend, and the current multiples underline how much confidence is already built in:

Earnings grew 5.7% over the last year and 10.8% a year over five years, which lines up with a case that the company has been able to grow profit from its US$5.3b revenue base while paying a regular dividend.

Against that, the gap between US$133.43 and the US$86.45 DCF fair value and the premium P/E versus peers show that expectations around forecast earnings growth of about 14.3% a year are embedded in the price, so any slowdown from the recent 8% revenue growth forecast or flat margins could put that premium under scrutiny.

Bulls argue that club growth and membership strength justify today’s premium tag, but the DCF gap tells a more cautious valuation story.

🐂 PriceSmart Bull Case

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for PriceSmart on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the data and turn it into a clear narrative: Do it your way

A great starting point for your PriceSmart research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

PriceSmart’s 2.7% net margin, slight compression from 2.8%, and share price premium to a stated US$86.45 DCF fair value leave limited room for disappointment.

If that kind of tight margin and premium pricing makes you uneasy, use our these 881 undervalued stocks based on cash flows to focus on companies where earnings power and valuation look better aligned today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.