Please use a PC Browser to access Register-Tadawul

Get It

Progyny (PGNY): Assessing Valuation as White House IVF Coverage Push Sparks Investor Interest

Progyny PGNY | 26.71 26.71 | +2.69% 0.00% Pre |

The White House has unveiled plans to encourage employers to make in vitro fertilization coverage available as a standalone benefit. Progyny (PGNY), a leader in fertility benefits, saw its stock jump nearly 7% following the news.

Progyny’s strong jump this week follows a year marked by big swings and renewed optimism, with its 1-year total shareholder return reaching nearly 28%. Momentum is gathering, as heightened interest in fertility policy changes has clearly boosted sentiment. Despite recent volatility, investors are keeping their eyes on long-term growth potential.

If you’re interested in more innovative healthcare stocks riding industry shifts, there are plenty of discovery opportunities in our curated list: See the full list for free.

With shares rallying and attention on coming policy changes, are investors seizing a real bargain in Progyny, or is all this optimism already accounted for in the current stock price, leaving little room for future upside?

Progyny’s fair value according to the prevailing narrative sits notably above its last close, suggesting room for price appreciation if bullish assumptions take hold. The difference between market skepticism and narrative confidence sets the scene for further debate.

Sustained high levels of employer interest in women's health and family-building benefits, supported by a recent national study and 81% of HR leaders prioritizing these services, point toward robust long-term demand, especially as employers seek to attract and retain talent. This broadening acceptance and adoption are likely to expand revenue and topline growth over time.

Curious what drives this bold valuation call? Unpack the projections behind the fair value. It hinges on aggressive future earnings, expanding margins, and premium pricing compared to the industry. Which of these key levers shapes the bullish outlook? Dive into the narrative for the critical details.

Result: Fair Value of $28.25 (UNDERVALUED)

However, broad-based employer cost-cutting or intensifying competition could curb Progyny’s growth and challenge the bullish outlook outlined above.

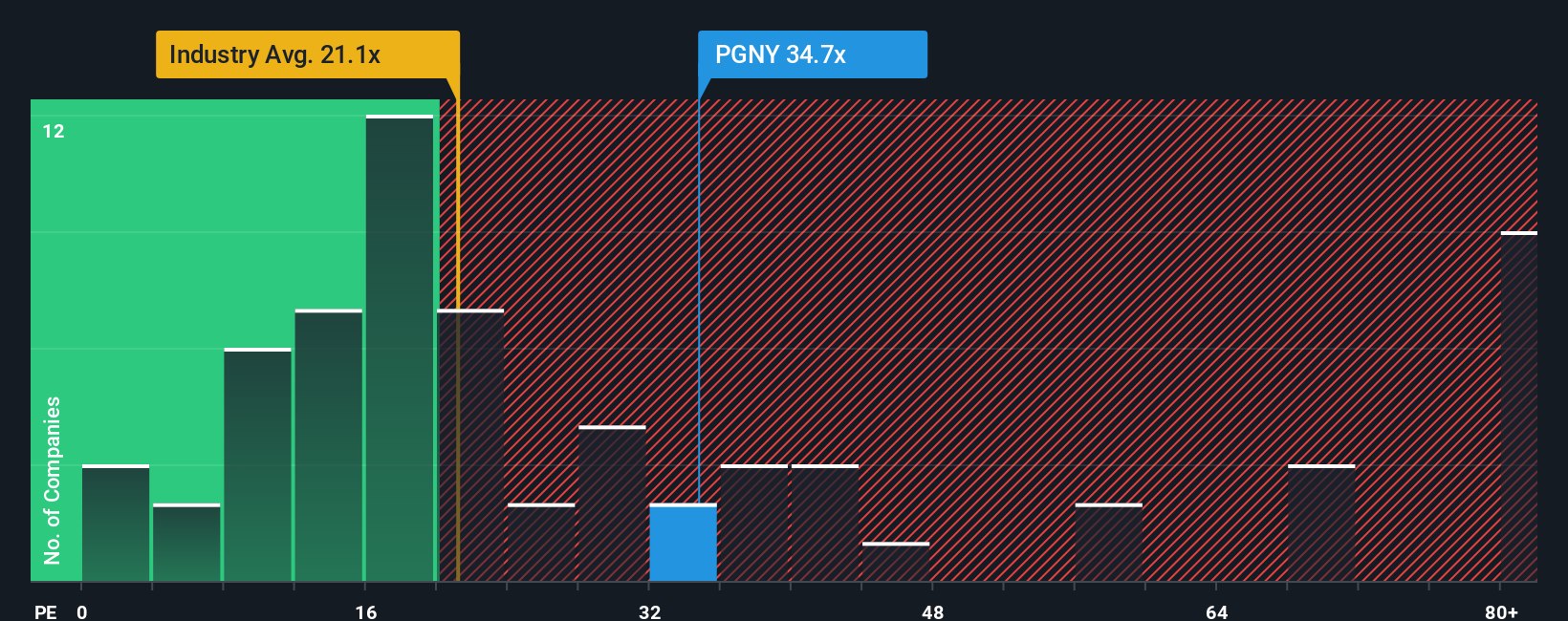

While the prevailing narrative suggests Progyny is undervalued, a look at its price-to-earnings ratio raises questions. Shares trade at 34.5 times earnings, well above both the US Healthcare industry average of 20.8x, peers at 22.9x, and even above the fair ratio of 25.4x. This premium hints at higher expectations, but also means the stock could be at risk if results disappoint. Is the market pricing in too much optimism, or does Progyny's growth potential justify paying up?

If you want to take a different angle or dive deeper into the numbers yourself, you’re free to build a fresh perspective in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Progyny.

Don’t let big opportunities pass you by. Broaden your portfolio using hand-picked stock ideas you might overlook, all rooted in robust fundamental research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.