Please use a PC Browser to access Register-Tadawul

Get It

PTC (PTC) Is Down 7.3% After Raising 2026 Guidance and Reporting Surging Earnings Growth

PTC Inc. PTC | 163.36 | +0.16% |

Find companies with promising cash flow potential yet trading below their fair value.

To be a shareholder in PTC, you need confidence in the company’s ability to keep growing recurring revenue by delivering AI-driven solutions that lock in large manufacturers as customers. The recent surge in quarterly earnings and raised 2026 guidance strengthens the view that AI adoption and digital transformation are acting as meaningful near-term growth catalysts. However, the most important short-term risk remains unpredictable deal timing due to global trade and policy uncertainty; the impact of the latest financial results on this risk is not material.

Among recent announcements, PTC’s launch of AI features for Onshape and Arena stands out as closely tied to its earnings momentum, these innovations are driving customer engagement, which directly informs the stronger topline guidance. Advances in the SaaS and AI strategy, combined with integration initiatives, have the potential to support higher contract values and margin expansion as recurring revenues build. But, unlike the optimism these launches generate, investors should be aware of the variable timing of large enterprise deals, which can quickly...

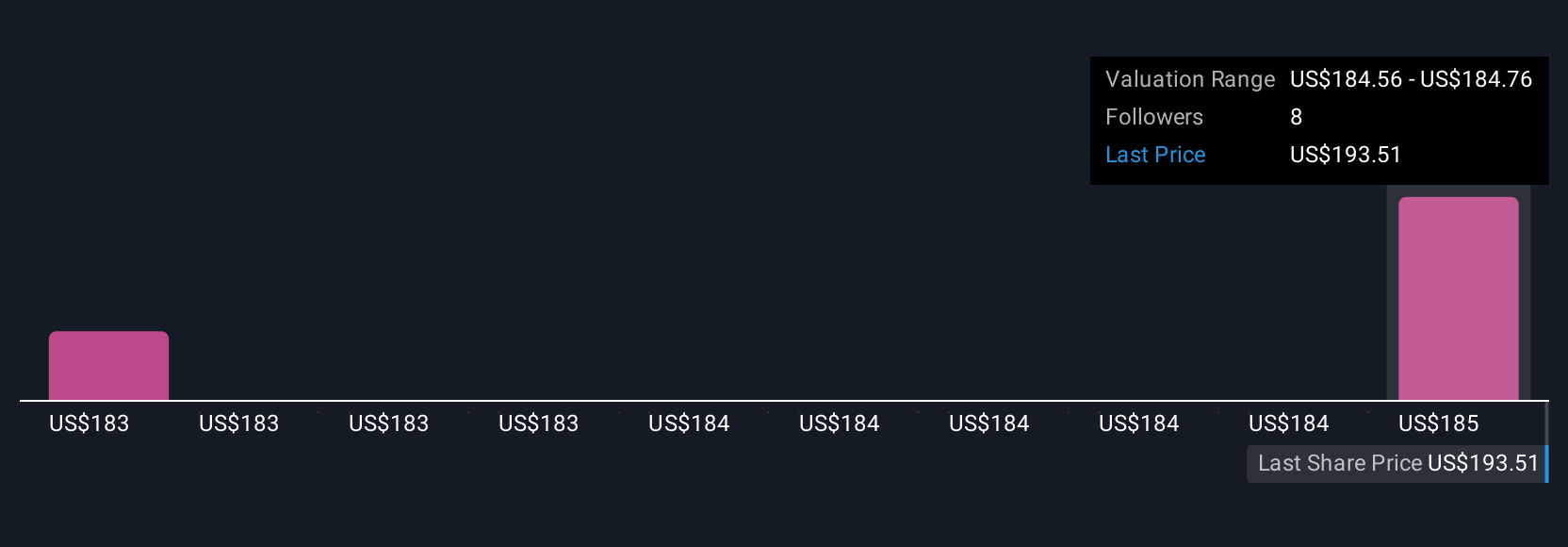

PTC's narrative projects $3.3 billion revenue and $814.8 million earnings by 2028. This requires 9.6% yearly revenue growth and a $302.1 million earnings increase from $512.7 million today.

Uncover how PTC's forecasts yield a $220.39 fair value, a 24% upside to its current price.

Fair value estimates from the Simply Wall St Community range from US$160 to over US$230,746 based on five individual forecasts. While some see current earnings momentum fueling further upside, others remain focused on persistent risks that could affect deal closure and future revenue stability, so make sure to weigh different viewpoints before making any decisions.

Explore 5 other fair value estimates on PTC - why the stock might be worth 10% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.