Please use a PC Browser to access Register-Tadawul

Get It

Sezzle Inc. (NASDAQ:SEZL) Stocks Pounded By 25% But Not Lagging Industry On Growth Or Pricing

Sezzle Inc. Ordinary Shares SEZL | 70.35 | -4.74% |

Sezzle Inc. (NASDAQ:SEZL) shares have retraced a considerable 25% in the last month, reversing a fair amount of their solid recent performance. Regardless, last month's decline is barely a blip on the stock's price chart as it has gained a monstrous 2,362% in the last year.

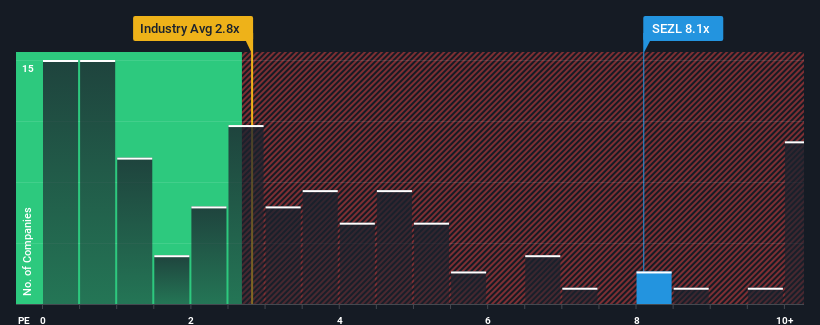

Although its price has dipped substantially, when almost half of the companies in the United States' Diversified Financial industry have price-to-sales ratios (or "P/S") below 2.9x, you may still consider Sezzle as a stock not worth researching with its 8.1x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Recent times have been advantageous for Sezzle as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Sezzle will help you uncover what's on the horizon.In order to justify its P/S ratio, Sezzle would need to produce outstanding growth that's well in excess of the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 49%. The latest three year period has also seen an excellent 113% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 38% during the coming year according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 4.3%, which is noticeably less attractive.

In light of this, it's understandable that Sezzle's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

A significant share price dive has done very little to deflate Sezzle's very lofty P/S. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Sezzle's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.