Could Instacart's (CART) Surge in Partnerships Reveal a Shift in Its Long-Term Competitive Strategy?

Simply Wall St 02/11 05:38

Shareholders May Not Be So Generous With ARC Document Solutions, Inc.'s (NYSE:ARC) CEO Compensation And Here's Why

ARC Document Solutions, Inc. ARC | 0.00 |

CEO Suri Suriyakumar has done a decent job of delivering relatively good performance at ARC Document Solutions, Inc. (NYSE:ARC) recently. As shareholders go into the upcoming AGM on 1st of May, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for ARC Document Solutions

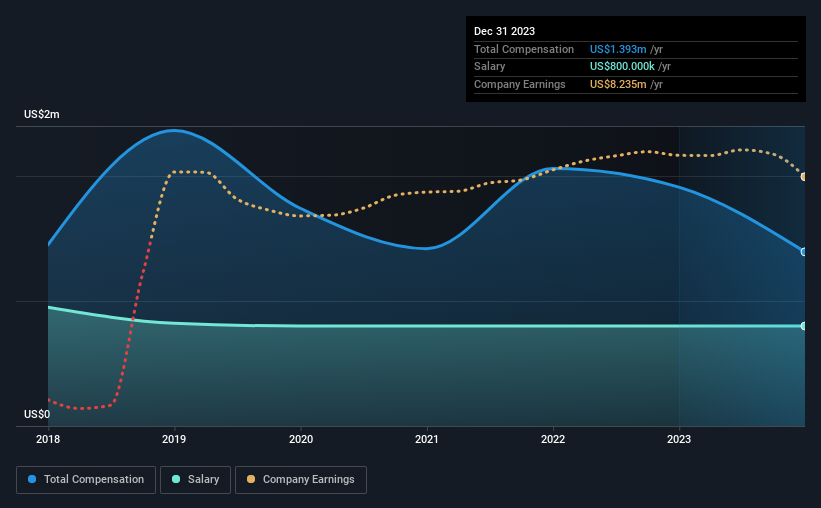

Our data indicates that ARC Document Solutions, Inc. has a market capitalization of US$118m, and total annual CEO compensation was reported as US$1.4m for the year to December 2023. We note that's a decrease of 27% compared to last year. In particular, the salary of US$800.0k, makes up a fairly large portion of the total compensation being paid to the CEO.

For comparison, other companies in the American Commercial Services industry with market capitalizations below US$200m, reported a median total CEO compensation of US$748k. Accordingly, our analysis reveals that ARC Document Solutions, Inc. pays Suri Suriyakumar north of the industry median. Moreover, Suri Suriyakumar also holds US$13m worth of ARC Document Solutions stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$800k | US$800k | 57% |

| Other | US$593k | US$1.1m | 43% |

| Total Compensation | US$1.4m | US$1.9m | 100% |

On an industry level, roughly 22% of total compensation represents salary and 78% is other remuneration. ARC Document Solutions is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

ARC Document Solutions, Inc. has seen its earnings per share (EPS) increase by 9.8% a year over the past three years. In the last year, its revenue is down 1.7%.

We would argue that the lack of revenue growth in the last year is less than ideal, but the modest improvement in EPS is good. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Boasting a total shareholder return of 42% over three years, ARC Document Solutions, Inc. has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for ARC Document Solutions that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.