Please use a PC Browser to access Register-Tadawul

Get It

Should Corpay’s (CPAY) New Partnership With BLAST Prompt Investors to Revisit Its Global Expansion Strategy?

Corpay, Inc. CPAY | 317.53 | -1.25% |

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

To be a shareholder in Corpay, investors need to believe in the company’s ability to drive sustained growth through expanding global payment flows and consistent enterprise adoption. While the recent BLAST partnership highlights Corpay’s competitive positioning in cross-border payments, it does not materially change the most important near-term catalyst: continued enterprise wins and technology adoption. The most significant risk remains the potential for new payment ecosystems to reduce Corpay's transaction volumes and yields. Among Corpay’s latest announcements, the recently completed share buyback, representing nearly 40 percent of outstanding shares since 2016, stands out as particularly relevant. Although returning capital to shareholders may signal management’s confidence and support earnings per share, it does not offset underlying risks of industry disruption or compressing margins. Yet, in contrast to these strong client wins, investors should also consider the risk that evolving fintech and payment ecosystems could...

Corpay's outlook anticipates $5.7 billion in revenue and $1.8 billion in earnings by 2028. This is based on an expected annual revenue growth rate of 10.9% and reflects an $0.8 billion increase in earnings from the current $1.0 billion.

Uncover how Corpay's forecasts yield a $350.00 fair value, a 26% upside to its current price.

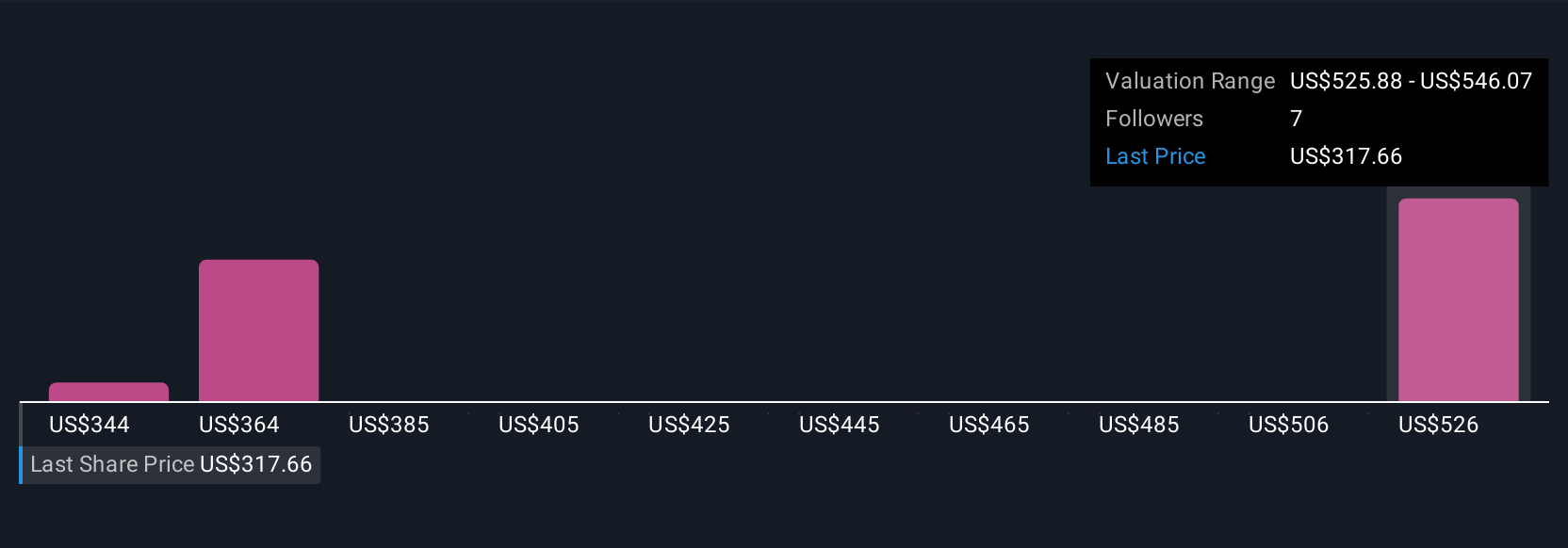

Fair value estimates from the Simply Wall St Community range widely from US$344.17 to US$515.56 based on five different perspectives. While many see compelling value, the persistent risk that disruptive payment models may erode Corpay’s margins remains a crucial factor for future performance.

Explore 5 other fair value estimates on Corpay - why the stock might be worth just $344.17!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.