Please use a PC Browser to access Register-Tadawul

Get It

Should Falling Freight Rates Signal a Shift in Matson (MATX) Investors' Long-Term Outlook?

Matson, Inc. MATX | 119.39 119.39 | -2.59% 0.00% Pre |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To be a shareholder in Matson, you need to believe in the company’s ability to generate stable long-term cash flows from its protected US shipping routes, even when industry cycles turn negative. The recent warning from Jefferies about freight rates falling below break-even levels highlights persistent near-term earnings pressure, which could weigh on sentiment and makes freight rate recovery the key catalyst, while the biggest risk now is sustained industry-wide price weakness. If freight rates stay soft for a prolonged period, this could materially impact Matson’s earnings and its narrative as a consistent compounder; otherwise, if rates recover, the headlines will matter less than trade flow trends in Matson’s core markets.

With Jefferies’ call coming just after Matson revised its third quarter outlook, the company's recent Q2 guidance, which flagged lower year-on-year Ocean Transportation earnings due to reduced rates and volumes, directly aligns with current concerns. While this guidance had already reset near-term expectations, the latest analyst caution spotlights the real-time volatility that continues to challenge even the best-positioned operators like Matson.

In contrast, the risk that increasingly volatile spot rates and industry overcapacity could continue to pressure margins is something shareholders should be watchful for...

Matson's outlook anticipates $3.4 billion in revenue and $289.2 million in earnings by 2028. This assumes a 0.3% annual revenue decline and a $204.9 million decrease in earnings from the current $494.1 million.

Uncover how Matson's forecasts yield a $115.00 fair value, a 16% upside to its current price.

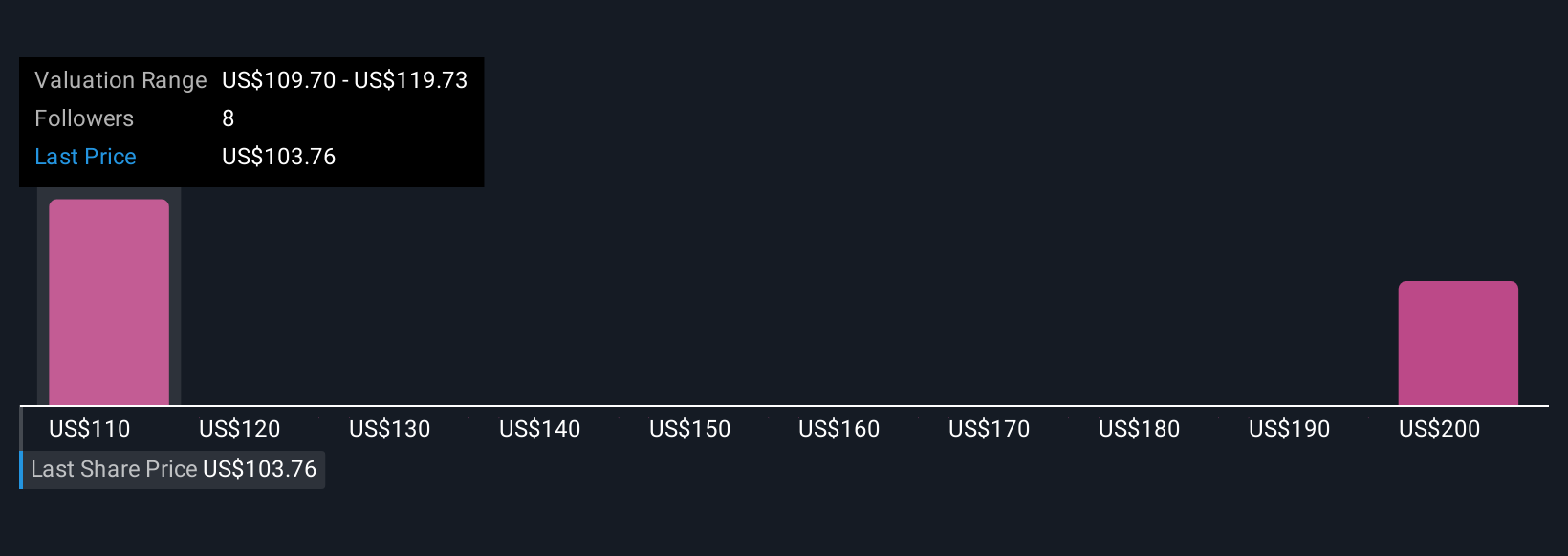

Seven Simply Wall St Community members estimate Matson’s fair value between US$92 and US$210 per share. While some anticipate robust upside, recent warnings on industry-wide freight rates falling below profitable levels could change the foundation of these valuations, make sure to compare multiple viewpoints before deciding your stance.

Explore 7 other fair value estimates on Matson - why the stock might be worth 7% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.