Please use a PC Browser to access Register-Tadawul

Get It

Should HNI’s (HNI) Post-Merger Debt Exchange Reshape How Investors View Its Balance Sheet?

HNI Corporation HNI | 52.55 | +2.28% |

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

To be a shareholder of HNI right now, you likely need to believe in its ability to grow earnings amid an uncertain market for traditional office furnishings and capitalize on operational improvements following the Steelcase acquisition. The recent exchange offer for Steelcase notes is a constructive step for debt transparency but does not materially change the core short-term catalyst: HNI’s ability to convert operational synergies into higher earnings. Similarly, the biggest risk, ongoing demand uncertainty in office and residential markets, remains unchanged by this move.

The most directly relevant prior announcement is HNI’s September 5, 2025, establishment of a US$425,000,000 revolving credit facility alongside term loans totaling up to US$1,300,000,000. This announcement underscores HNI’s recent focus on optimizing its capital structure and preparing for post-acquisition integration and flexibility, tying in with how funding and debt management relate to HNI’s ability to realize synergies and achieve targeted earnings growth in the near term.

Yet, in contrast to these efforts to strengthen financial flexibility, there remains the risk investors should be aware of if workplace demand continues to...

HNI's outlook anticipates $2.9 billion in revenue and $234.7 million in earnings by 2028. This is based on a projected annual revenue growth rate of 4.2% and an earnings increase of $86.7 million from the current $148.0 million.

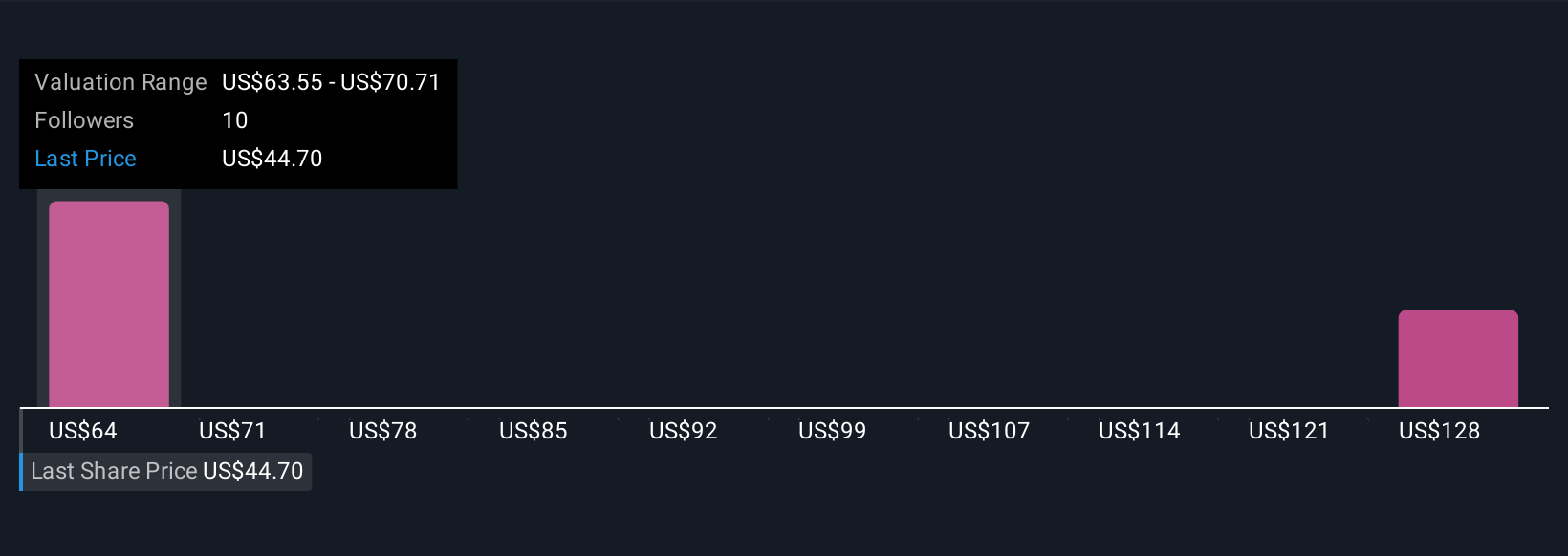

Uncover how HNI's forecasts yield a $66.75 fair value, a 45% upside to its current price.

Simply Wall St Community members have posted four individual fair value estimates ranging from US$48.80 to US$136.22 per share. While many believe HNI’s synergy capture and operational gains could support growth, opinions differ widely on what that might mean for future returns so consider the full breadth of these perspectives.

Explore 4 other fair value estimates on HNI - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.