Please use a PC Browser to access Register-Tadawul

Get It

Should Upward Earnings Revisions and Market Leadership in Multifamily Deals Require Action From CBRE Group (CBRE) Investors?

CBRE Group Inc Class A CBRE | 161.54 | +1.68% |

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

To be a shareholder in CBRE Group, you need to believe in the company’s ability to maintain market leadership in commercial real estate services while successfully driving growth in resilient segments like multifamily capital markets. The latest upward revision in earnings estimates supports the main short-term catalyst, continued deal momentum and operational expansion, but does not materially diminish exposure to interest rate volatility, which remains the key risk to near-term earnings consistency.

Of the recent announcements, the closure of $1.63 billion in multifamily deals by CBRE’s Boston team in 2024, and early 2025’s leading performance, provides tangible evidence of the strong pipeline and deep client relationships that underpin the current optimism around earnings. This momentum illustrates how success in a high-demand vertical can reinforce the company’s broader growth outlook, despite economic headwinds and shifting capital markets dynamics.

However, despite these strengths, investors should be aware that interest rate swings could still...

CBRE Group's narrative projects $50.0 billion revenue and $2.3 billion earnings by 2028. This requires 9.5% yearly revenue growth and a $1.2 billion increase in earnings from the current $1.1 billion.

Uncover how CBRE Group's forecasts yield a $169.73 fair value, a 3% upside to its current price.

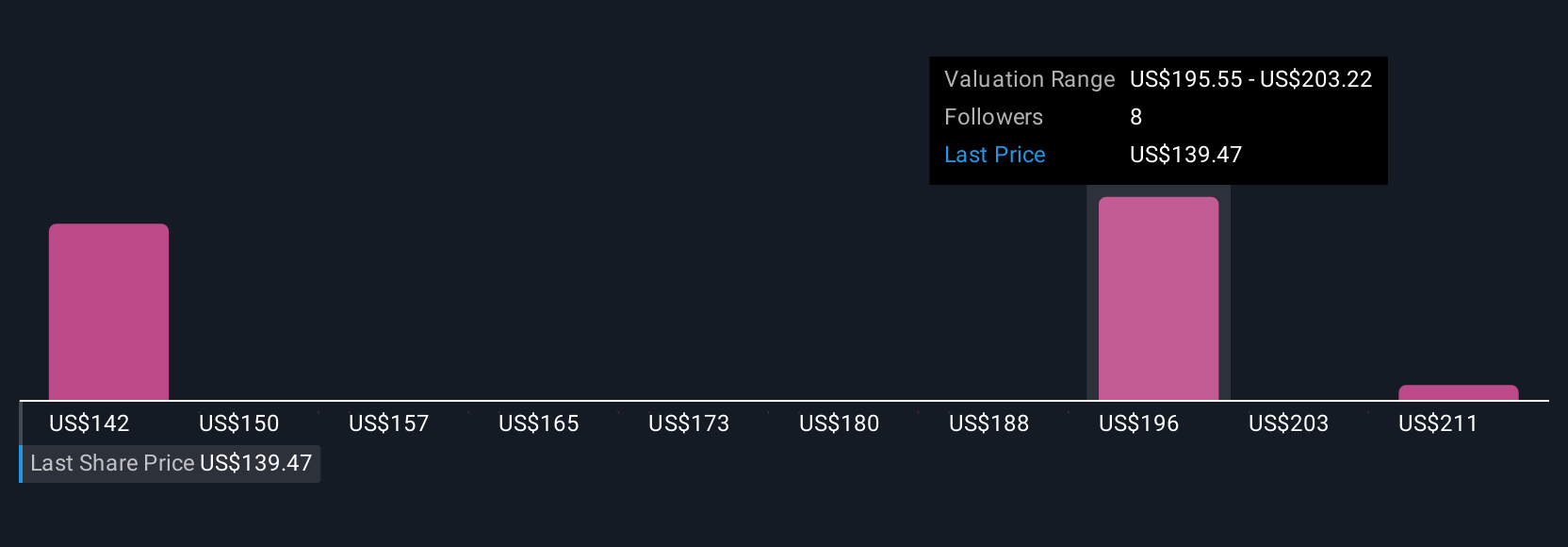

The Simply Wall St Community’s 3 fair value estimates for CBRE Group range widely from US$155.37 to US$218.54 per share. Amid strong earnings momentum, it’s clear that opinions can differ and there is value in exploring multiple viewpoints.

Explore 3 other fair value estimates on CBRE Group - why the stock might be worth as much as 33% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.