Please use a PC Browser to access Register-Tadawul

Get It

Some Owlet, Inc. (NYSE:OWLT) Shareholders Look For Exit As Shares Take 31% Pounding

Owlet, Inc. Class A OWLT | 11.79 | +4.52% |

Owlet, Inc. (NYSE:OWLT) shares have retraced a considerable 31% in the last month, reversing a fair amount of their solid recent performance. Of course, over the longer-term many would still wish they owned shares as the stock's price has soared 127% in the last twelve months.

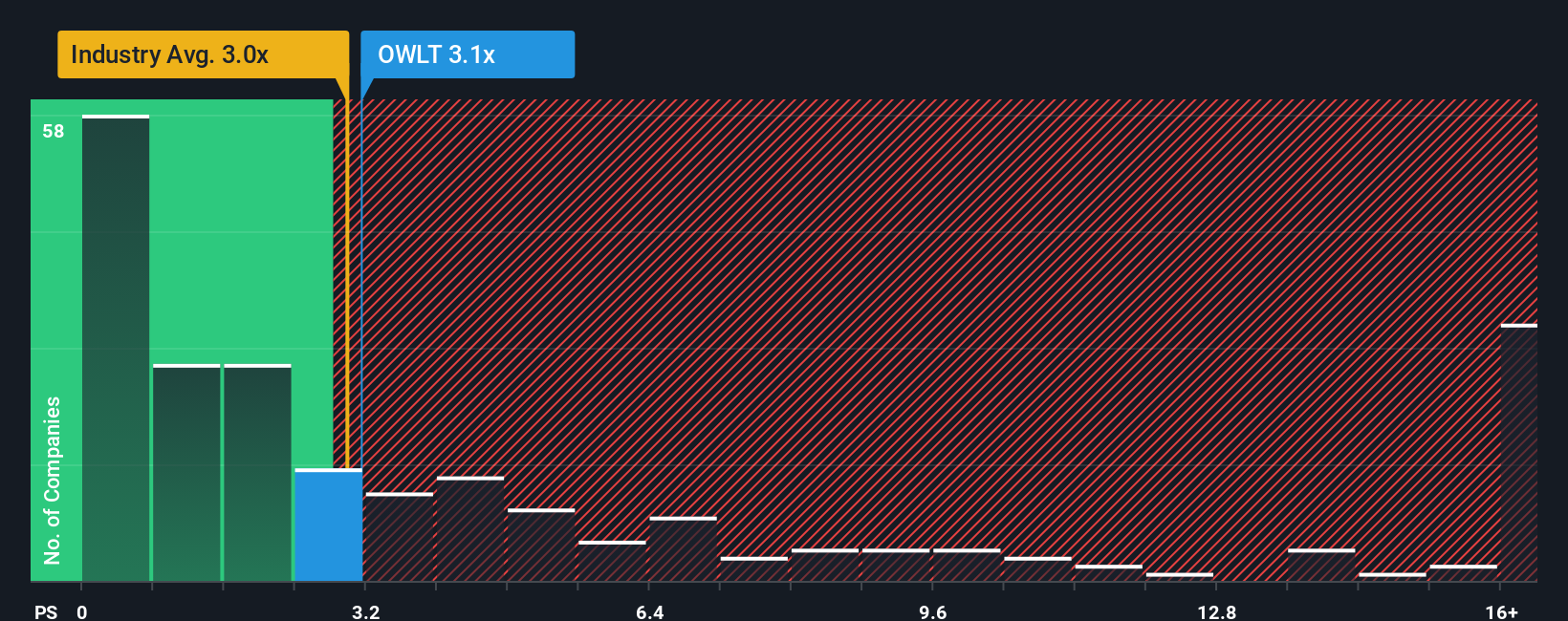

Even after such a large drop in price, it's still not a stretch to say that Owlet's price-to-sales (or "P/S") ratio of 3.1x right now seems quite "middle-of-the-road" compared to the Medical Equipment industry in the United States, where the median P/S ratio is around 3x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

With revenue growth that's superior to most other companies of late, Owlet has been doing relatively well. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on Owlet will help you uncover what's on the horizon.In order to justify its P/S ratio, Owlet would need to produce growth that's similar to the industry.

Taking a look back first, we see that the company grew revenue by an impressive 27% last year. Pleasingly, revenue has also lifted 82% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the five analysts covering the company suggest revenue should grow by 23% over the next year. With the industry predicted to deliver 54% growth, the company is positioned for a weaker revenue result.

With this information, we find it interesting that Owlet is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

Following Owlet's share price tumble, its P/S is just clinging on to the industry median P/S. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

When you consider that Owlet's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.