Please use a PC Browser to access Register-Tadawul

Get It

Strong Q3 Results and Share Buyback Might Change the Case for Investing in New York Times (NYT)

New York Times Company Class A NYT | 79.31 | +1.60% |

Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

To be a shareholder of The New York Times Company today, you likely need confidence in its ability to keep growing digital subscriptions and monetizing trusted journalism, even as new challenges from AI-driven content tools threaten audience reach and differentiation. Recent third-quarter earnings reflected solid revenue and earnings increases, but this performance alone does not materially change the short-term catalyst, continued digital subscriber growth remains the most important driver, while external tech disruption by platforms like Google and ChatGPT is still the clearest risk to watch.

The company’s latest update on its share repurchase program is particularly relevant, confirming that NYT has now acquired more than 4 million shares for US$207 million since early 2023. While buybacks provide visible capital returns to shareholders and may help offset dilution, their influence relies heavily on the company’s ability to keep expanding its digital subscriber base in the face of intensifying platform competition and content commoditization.

Yet, in contrast to a period of consistent subscriber momentum, investors should be aware of the growing risk from technology platforms limiting publisher reach...

New York Times' narrative projects $3.2 billion revenue and $487.8 million earnings by 2028. This requires 6.7% yearly revenue growth and a $167.4 million earnings increase from $320.4 million today.

Uncover how New York Times' forecasts yield a $63.50 fair value, in line with its current price.

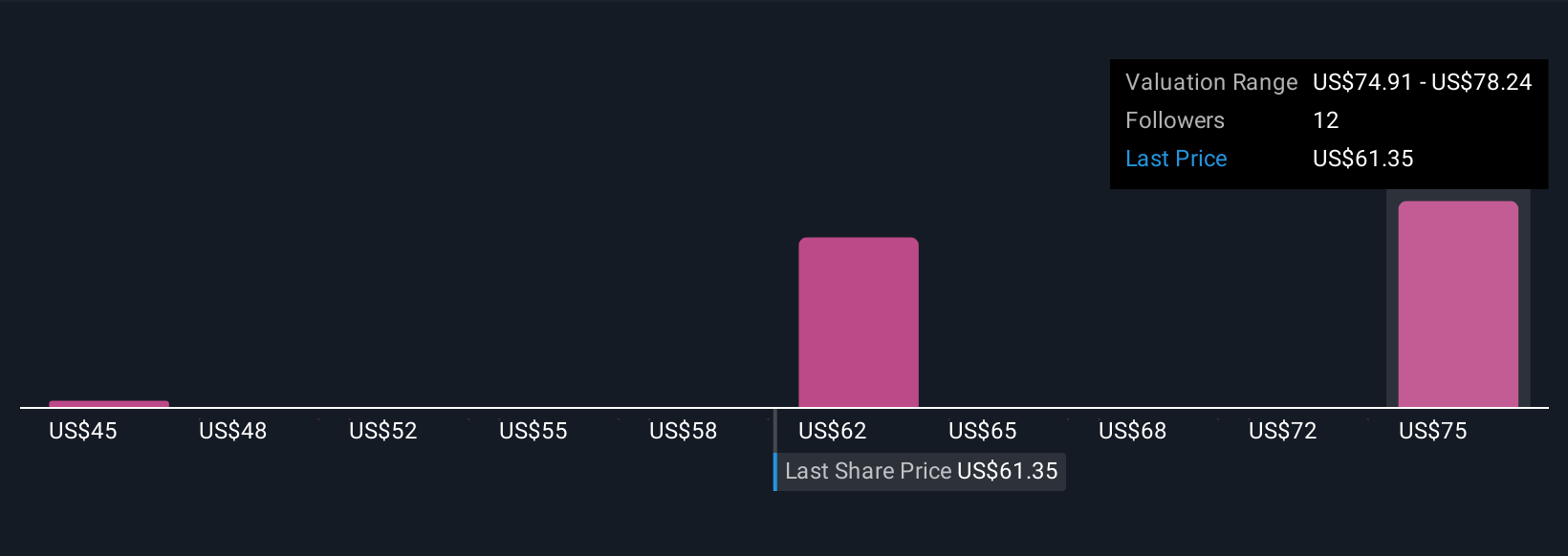

Simply Wall St Community members estimate NYT’s fair value from US$44.95 to US$83.83, showing wide divergence across three viewpoints. With digital subscription growth seen as a key catalyst, the variety of opinions highlights how perspectives on NYT’s future performance can differ, explore several viewpoints before forming your own conclusions.

Explore 3 other fair value estimates on New York Times - why the stock might be worth as much as 31% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.