Please use a PC Browser to access Register-Tadawul

Get It

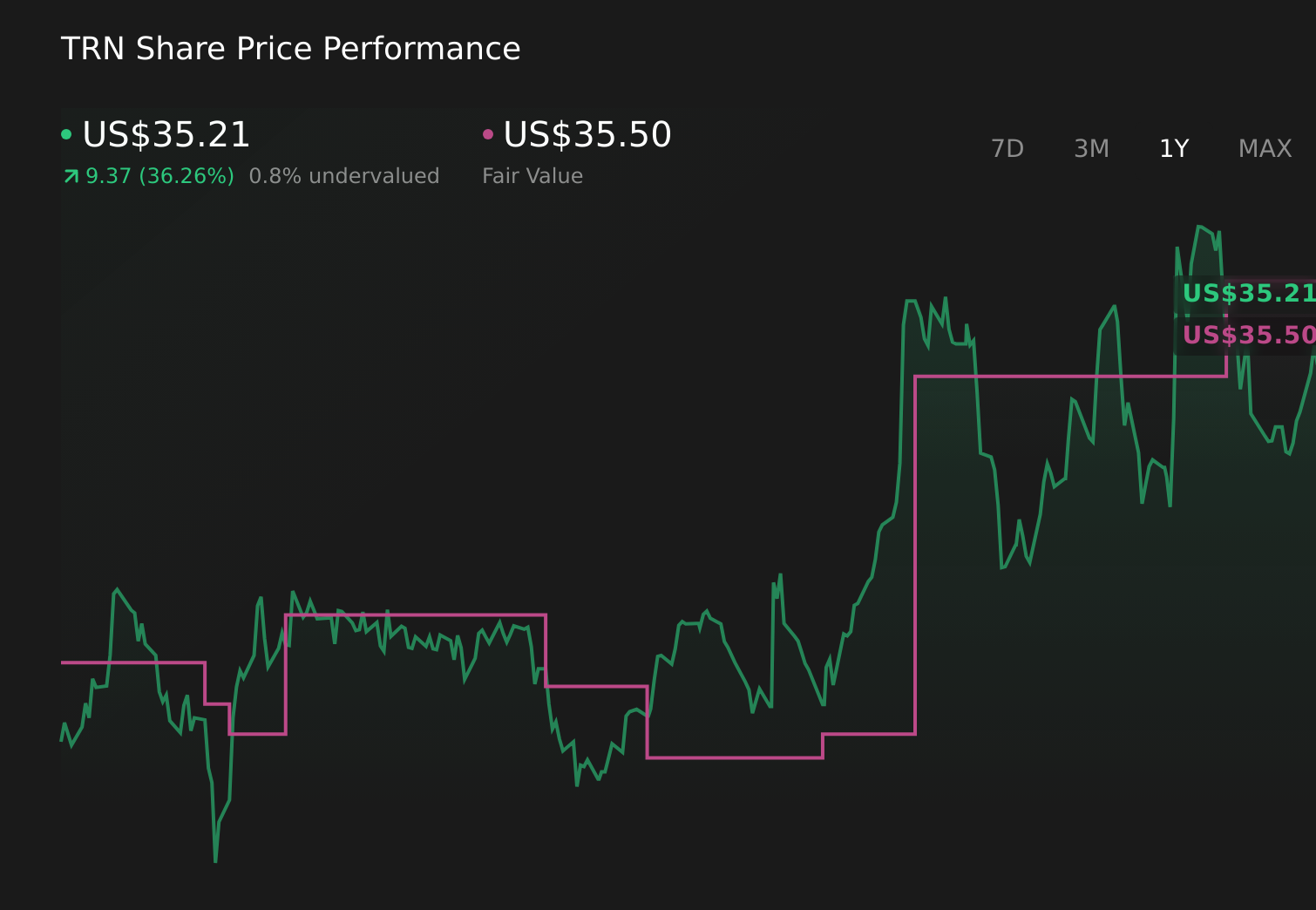

Trinity Industries (TRN) Is Up 5.1% After Raising 2025 EPS Guidance To $3.05–$3.20 - What's Changed

Trinity Industries, Inc. TRN | 34.97 | +2.40% |

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

To own Trinity, you need to believe that rail remains an essential freight backbone and that Trinity can convert that role into steadier earnings, despite its exposure to cyclical energy and agriculture demand. The higher 2025 EPS guidance supports the near term earnings catalyst, but it does not remove key risks around railcar demand, customer spending delays, and cost pressures, which can still weigh on orders, margins, and cash flows.

The December 2025 dividend increase to US$0.31 per share, marking seven consecutive years of raises, lines up with management’s more confident earnings outlook and the new 2025 guidance range. Together, the higher EPS target and steadily rising dividend signal that Trinity is leaning on income-focused shareholders while it works through industry capacity, cost, and demand challenges that remain central to the stock’s risk profile.

But investors should also be aware of how dependent Trinity still is on railcar replacement demand and what happens if ...

Trinity Industries' narrative projects $2.6 billion revenue and $207.4 million earnings by 2028. This requires 1.3% yearly revenue growth and about a $98.8 million earnings increase from $108.6 million today.

Uncover how Trinity Industries' forecasts yield a $25.50 fair value, a 10% downside to its current price.

Two fair value estimates from the Simply Wall St Community span roughly US$16.16 to US$25.50 per share, underscoring how far opinions can spread. When you set those side by side with Trinity’s heightened reliance on a railcar market recovery to lift utilization and margins, it becomes clear why you may want to compare several viewpoints before deciding how this stock fits into your portfolio.

Explore 2 other fair value estimates on Trinity Industries - why the stock might be worth 43% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.