Please use a PC Browser to access Register-Tadawul

Get It

Ultragenyx Pharmaceutical (NASDAQ:RARE) Is Carrying A Fair Bit Of Debt

Ultragenyx Pharmaceutical, Inc. RARE | 36.23 | +0.08% |

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Ultragenyx Pharmaceutical Inc. (NASDAQ:RARE) makes use of debt. But is this debt a concern to shareholders?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

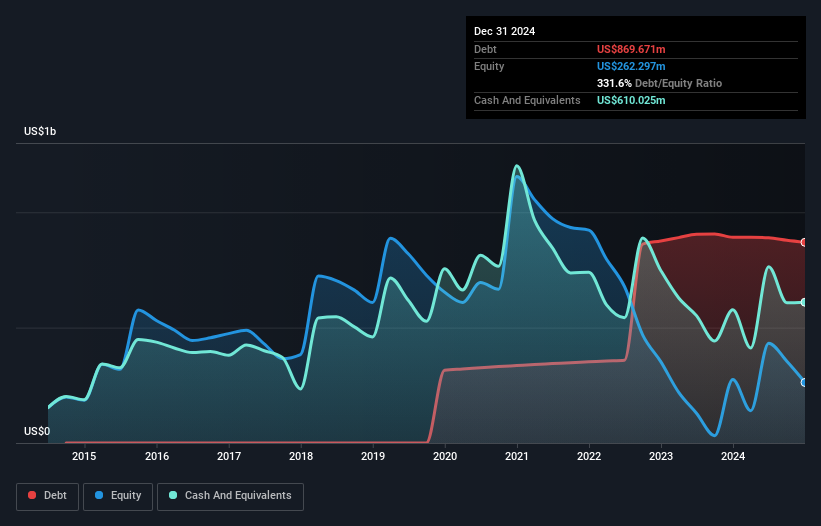

As you can see below, Ultragenyx Pharmaceutical had US$869.7m of debt, at December 2024, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$610.0m in cash, and so its net debt is US$259.6m.

According to the last reported balance sheet, Ultragenyx Pharmaceutical had liabilities of US$344.2m due within 12 months, and liabilities of US$897.0m due beyond 12 months. Offsetting these obligations, it had cash of US$610.0m as well as receivables valued at US$123.6m due within 12 months. So it has liabilities totalling US$507.5m more than its cash and near-term receivables, combined.

Given Ultragenyx Pharmaceutical has a market capitalization of US$3.00b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Ultragenyx Pharmaceutical can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Ultragenyx Pharmaceutical reported revenue of US$560m, which is a gain of 29%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Despite the top line growth, Ultragenyx Pharmaceutical still had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable US$536m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$434m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.