Please use a PC Browser to access Register-Tadawul

Get It

Under Armour (UAA) Valuation Check As Earnings Optimism And Analyst Interest Build

Under Armour, Inc. Class A UAA | 6.12 | -2.08% |

Under Armour (UAA) is back in focus as traders look ahead to its upcoming quarterly earnings report, with recent analyst commentary and fresh coverage helping to put the stock under a brighter spotlight.

Under Armour shares have seen a sharp short term rebound, with a 30 day share price return of 16.64% and a 90 day share price return of 35.01%. However, the 1 year total shareholder return of 26.11% and 5 year total shareholder return of 70.19% remain weak. This suggests that recent momentum is building off a much tougher longer term backdrop as investors reassess the risk and earnings outlook ahead of the upcoming report.

If you are weighing Under Armour against other names in the sector, this could be a useful moment to scan auto manufacturers and see how different consumer facing brands are being priced today.

With Under Armour trading at US$6.17 against an average analyst target of about US$6.22 and an intrinsic value estimate that suggests a premium, you have to ask yourself: is there real upside left here, or is the market already pricing in any future growth?

Compared to Under Armour's last close at $6.17, the most followed narrative points to a fair value of about $5.87, implying only a small valuation gap and a lot riding on execution.

The ongoing transformation to a brand-first strategy, with a focus on premiumization, tighter SKU assortments, and greater brand storytelling, positions Under Armour to increase average selling prices, improve full-price sell-through, and reduce reliance on discounting, which should positively impact net margins and long-term earnings growth.

Curious what kind of revenue trajectory, margin rebuild and future earnings multiple sit behind that fair value number? The full narrative spells out the entire earnings bridge, step by step.

Result: Fair Value of $5.87 (OVERVALUED)

However, there are clear pressure points too, including tariff-related margin headwinds and ongoing weakness in footwear that could challenge the brand’s turnaround story.

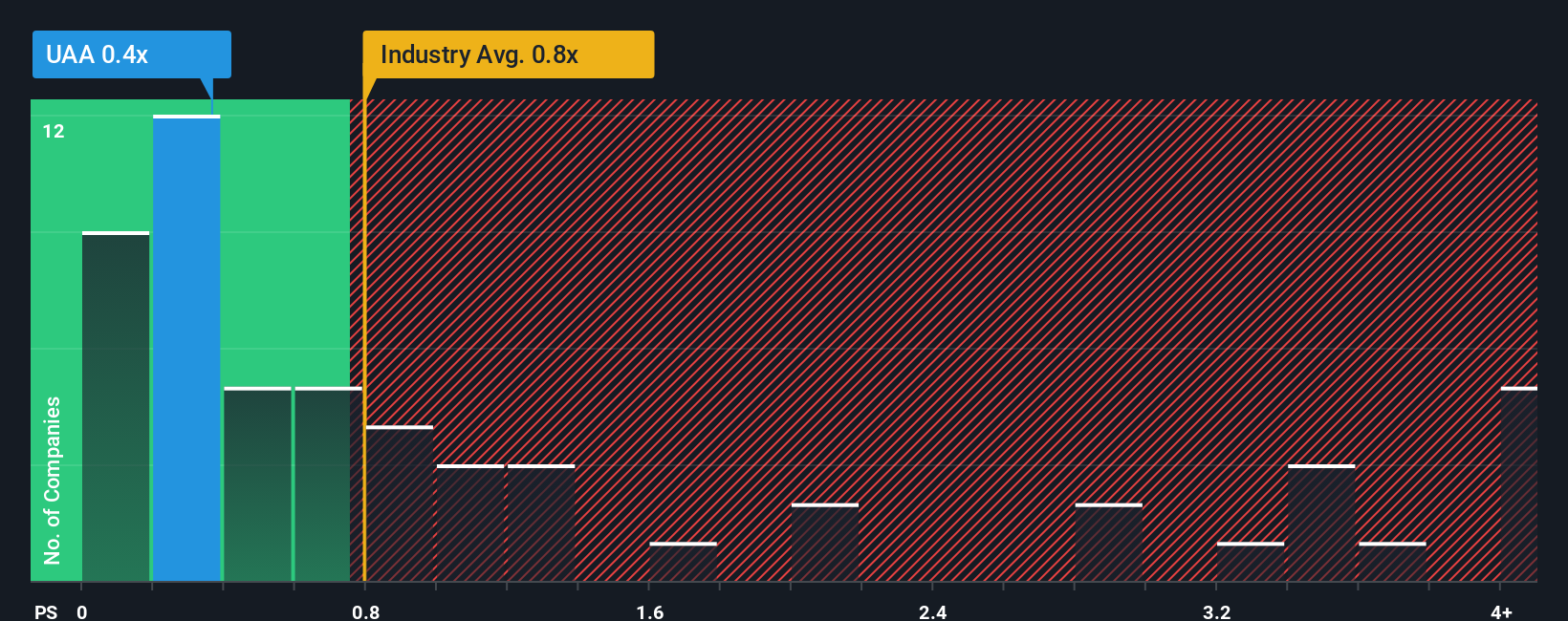

While the most followed narrative flags Under Armour as about 5.1% overvalued on fair value of $5.87 versus the $6.17 share price, the P/S ratio paints a different picture. At 0.5x sales, the stock trades below both the US Luxury industry average of 0.7x and its own fair ratio of 1x. This comparison suggests the market could move closer to that higher multiple over time.

So you have one model indicating the price is a little rich and another hinting at a discount. This raises a simple question: which signal do you trust more when the story is this mixed?

If you see the story differently or simply prefer running your own numbers, you can stress test every assumption and build a tailored view in minutes using Do it your way.

A great starting point for your Under Armour research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

If Under Armour has prompted fresh questions about where to put your money next, do not stop here. Broaden your watchlist now so you are not reacting late.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.