Please use a PC Browser to access Register-Tadawul

Get It

Undervalued Small Caps With Insider Activity To Watch In October 2025

Granite Ridge Resources, Inc. Common Stock GRNT | 5.05 | -1.75% |

As the U.S. stock market navigates a landscape marked by record highs for the S&P 500 and Nasdaq, small-cap stocks present intriguing opportunities amid broader economic uncertainties such as the ongoing government shutdown. With major indices showing mixed results and gold prices fluctuating, investors are keenly observing sectors that may offer value in these volatile times. In this environment, identifying promising small-cap stocks often involves looking at companies with strong fundamentals and potential insider activity, which can signal confidence from those closest to the business.

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Limbach Holdings | 31.7x | 2.0x | 38.26% | ★★★★★★ |

| PCB Bancorp | 9.4x | 2.8x | 36.67% | ★★★★★☆ |

| Peoples Bancorp | 10.1x | 1.9x | 44.10% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 0.8x | 27.42% | ★★★★★☆ |

| Citizens & Northern | 11.3x | 2.8x | 41.57% | ★★★★☆☆ |

| First Northern Community Bancorp | 9.8x | 2.8x | 47.46% | ★★★★☆☆ |

| Thryv Holdings | NA | 0.7x | 35.73% | ★★★★☆☆ |

| Shore Bancshares | 9.9x | 2.6x | -77.56% | ★★★☆☆☆ |

| Arrow Financial | 14.5x | 3.1x | 21.51% | ★★★☆☆☆ |

| Farmland Partners | 6.9x | 8.4x | -42.56% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

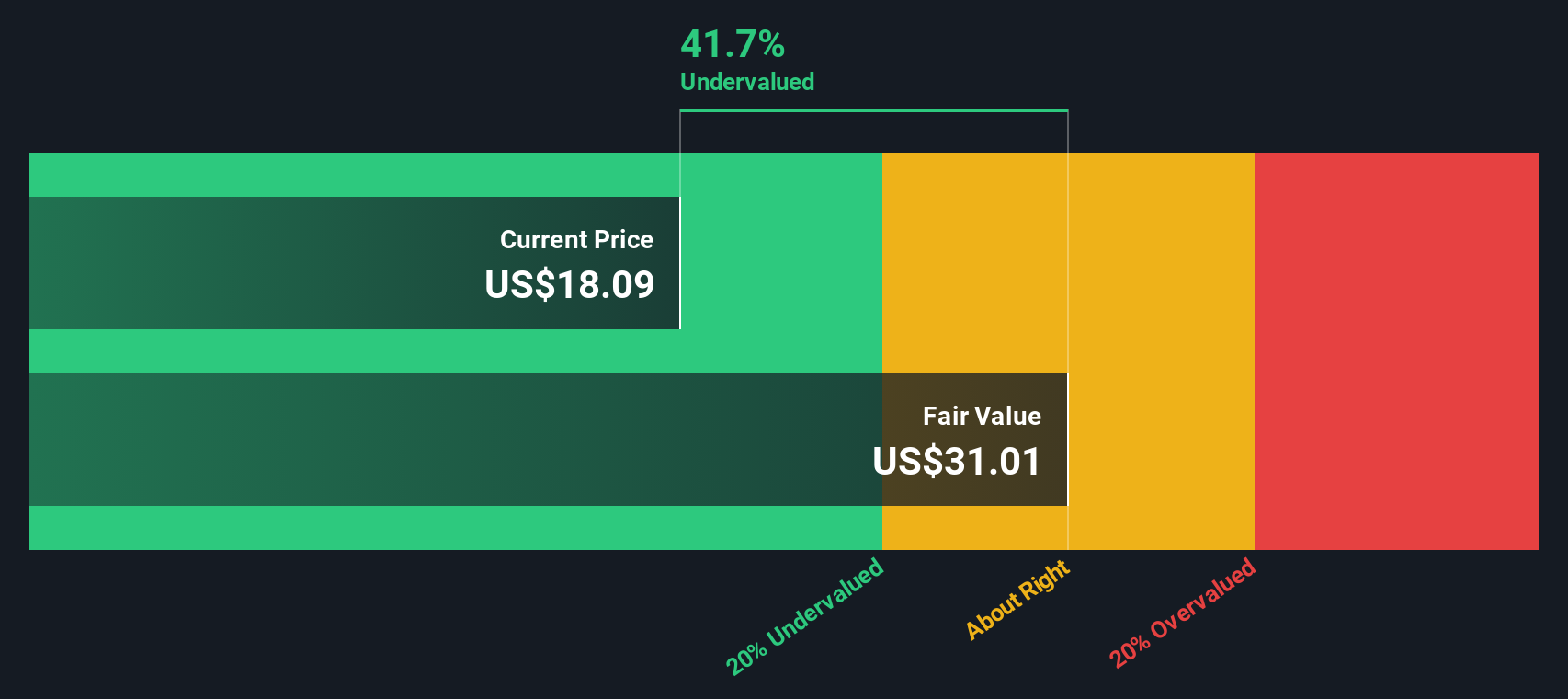

Simply Wall St Value Rating: ★★★☆☆☆

Overview: FinWise Bancorp operates as a financial institution providing banking services, with a market capitalization of $0.13 billion.

Operations: FinWise Bancorp's revenue primarily stems from its banking operations, with a gross profit margin consistently at 100%. The net income margin has shown variability, reaching as high as 43.09% in early 2022 but declining to around 18.35% by mid-2025. Operating expenses have increased over time, with general and administrative expenses forming a significant portion of these costs.

PE: 18.2x

FinWise Bancorp, a smaller player in the financial sector, is gaining attention after being added to the S&P Global BMI Index on September 21, 2025. The company reported improved second-quarter results with net income rising to US$4.1 million from US$3.18 million a year earlier and earnings per share increasing as well. Despite challenges with high non-performing loans at 7.4% and low allowances at 41%, insider confidence is reflected through recent share purchases this year, hinting at potential growth prospects with forecasted earnings growth of 32.88% annually.

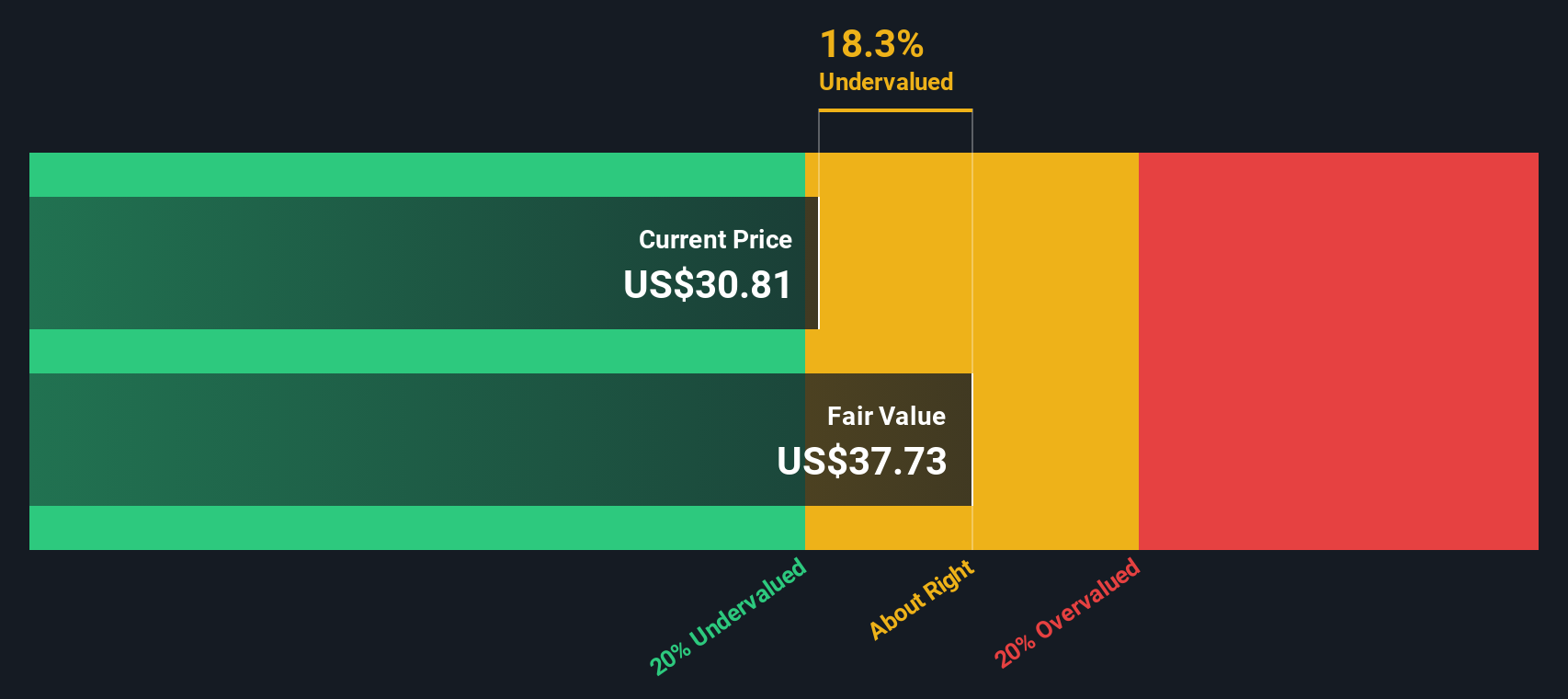

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Washington Trust Bancorp operates as a financial services company providing commercial banking and wealth management services, with a market capitalization of approximately $0.76 billion.

Operations: The company generates revenue primarily from Commercial Banking and Wealth Management Services, with recent figures showing $73.33 million and $40.58 million respectively. Operating expenses have consistently been a significant portion of the revenue, with General & Administrative Expenses alone reaching approximately $122.87 million by mid-2025. The net income margin has shown a downward trend recently, turning negative in late 2024 and early 2025, indicating challenges in profitability despite maintaining a gross profit margin of 100%.

PE: -21.1x

Washington Trust Bancorp, a smaller player in the financial sector, showcases potential for growth with earnings projected to rise by 111.03% annually. Recent insider confidence is evident as they acquired shares between May and June 2025. The company reported net income of US$13.25 million for Q2 2025, up from US$10.82 million the previous year, alongside a completed share buyback of 10,000 shares for US$0.3 million. Strategic leadership changes aim to bolster commercial banking activities further enhancing its appeal in the market segment it serves.

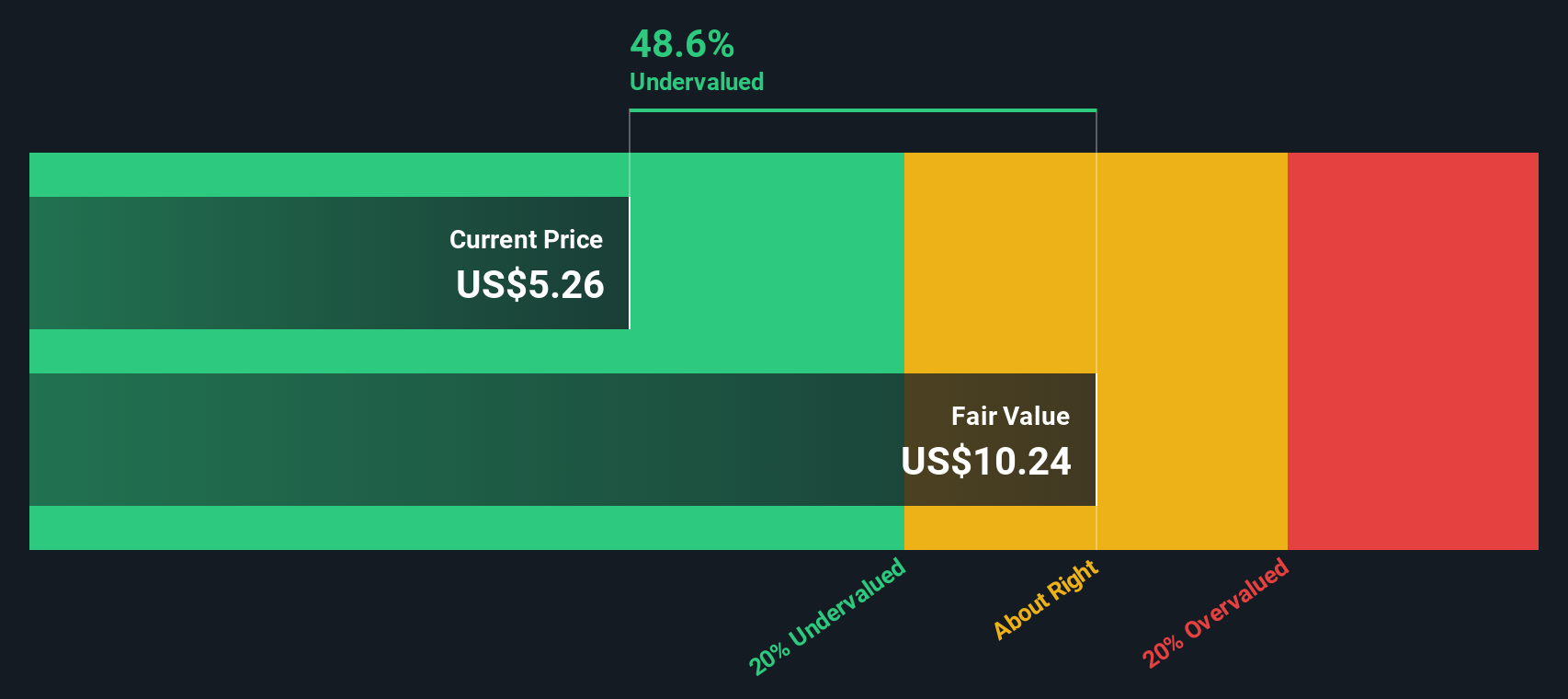

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Granite Ridge Resources is engaged in the development, exploration, and production of oil and natural gas with a market capitalization of approximately $1.88 billion.

Operations: Granite Ridge Resources generates revenue primarily from oil and natural gas development, exploration, and production. The company's cost of goods sold (COGS) has been increasing over time, impacting its gross profit margin, which was last reported at 82.98%. Operating expenses include significant depreciation and amortization costs. The net income margin has shown fluctuations with a recent figure of 7.83%.

PE: 22.5x

Granite Ridge Resources, a smaller player in the energy sector, has shown significant earnings growth with net income rising to US$25.08 million for Q2 2025 from US$5.1 million a year ago, and earnings per share jumping to US$0.19 from US$0.04. Despite high debt levels and reliance on external funding, their production surged by 37% year-over-year in Q2 2025. Co-Chairman Matthew Miller's purchase of 41,000 shares for approximately US$250K reflects insider confidence amid these developments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.