Please use a PC Browser to access Register-Tadawul

Get It

Veracyte’s Strong Revenue Growth and Product Pipeline Could Be a Game Changer for VCYT

Veracyte Inc VCYT | 42.84 | +1.47% |

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

To be a Veracyte shareholder today, you need to believe in the company's ability to grow beyond its core Decipher and Afirma tests while executing on new cancer diagnostics like the Minimal Residual Disease (MRD) platform. While recent news of strong revenue growth and institutional interest draws attention to these positive trends, it does not materially change the underlying short-term catalyst: the expansion and reimbursement of existing tests remain the key near-term driver, while revenue concentration risk is still the most immediate threat.

The upcoming Q3 2025 earnings announcement on November 4 is the most relevant event, as it will offer fresh insight into revenue momentum and profitability. In this context, continued outperformance of core product lines and updates on MRD platform progress are likely to remain front and center for investors tracking near-term execution against growth targets.

However, with reimbursement risks still looming, it’s crucial investors remain mindful that ...

Veracyte's narrative projects $629.2 million in revenue and $121.9 million in earnings by 2028. This requires 9.5% yearly revenue growth and a $95.6 million earnings increase from $26.3 million currently.

Uncover how Veracyte's forecasts yield a $39.75 fair value, a 14% upside to its current price.

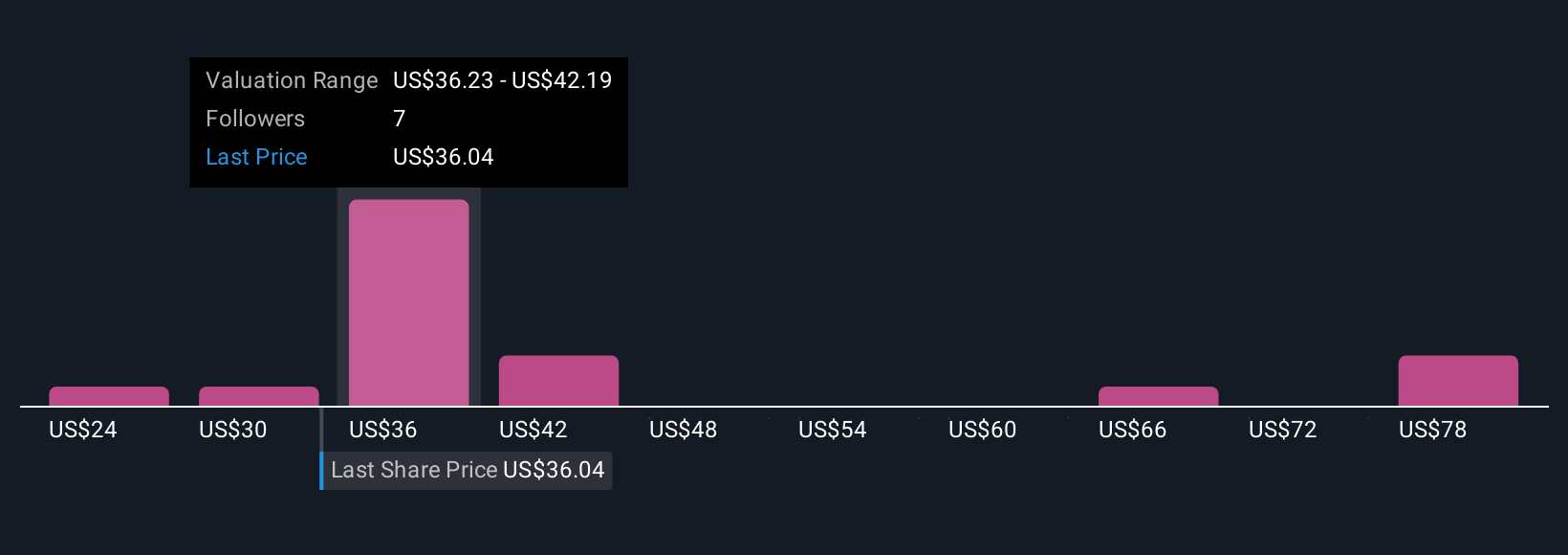

Six Simply Wall St Community members estimate Veracyte’s fair value from US$24.31 to US$83.39, showing wide variety in individual forecasts. These diverse views complement ongoing concerns about revenue concentration and remind you to compare alternative perspectives on performance drivers before making conclusions.

Explore 6 other fair value estimates on Veracyte - why the stock might be worth 30% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.