Please use a PC Browser to access Register-Tadawul

Get It

VeriSign (VRSN) Margin Decline Reinforces Investor Focus on Long-Term Profit Quality

VeriSign, Inc. VRSN | 242.00 242.00 | -0.85% 0.00% Pre |

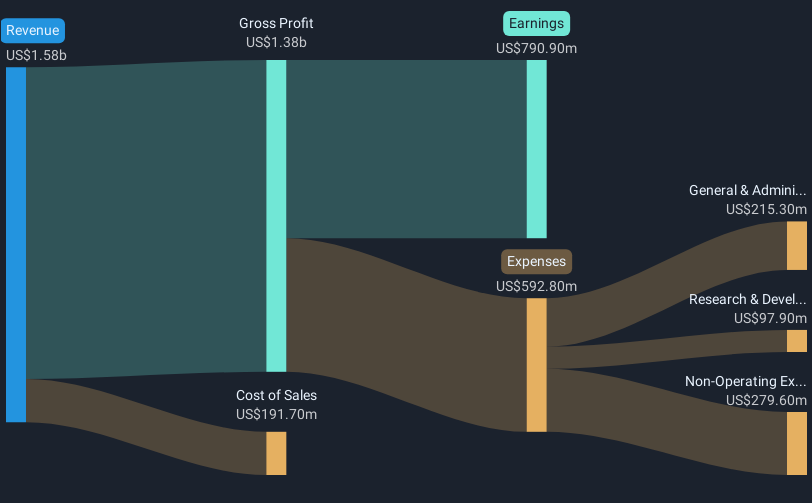

VeriSign (VRSN) reported that earnings are forecast to grow at 5.8% per year, with revenue expected to increase by 4.7% annually. Profit margins narrowed this year, landing at 49.9%, compared to 55.7% last year. Despite negative earnings growth over the past year, earnings have grown at 2.8% per year over the last five years, and the company’s profits are still considered high quality.

See our full analysis for VeriSign.The next section will put these earnings trends head to head with community narratives to highlight where consensus holds strong and where there may be surprises.

See how analysts weigh these profit trends in their latest forecasts. 📊 Read the full VeriSign Consensus Narrative.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for VeriSign on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Think you have a different take on the latest figures? Bring your perspective to life and share your own view in just a few minutes. Do it your way

A great starting point for your VeriSign research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Despite VeriSign’s solid profitability, narrowing margins and premium valuation could make future growth less certain as the business depends more on continued revenue expansion.

If you would prefer steadier performers, use our stable growth stocks screener (2099 results) to find companies with consistent revenue and earnings growth across economic cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.