Vestis (VSTS) Reaffirms 2026 Outlook After Swing to Quarterly Loss Is Management Signaling Steady Confidence?

Vestis Corporation VSTS | 7.88 7.88 | +1.03% 0.00% Post |

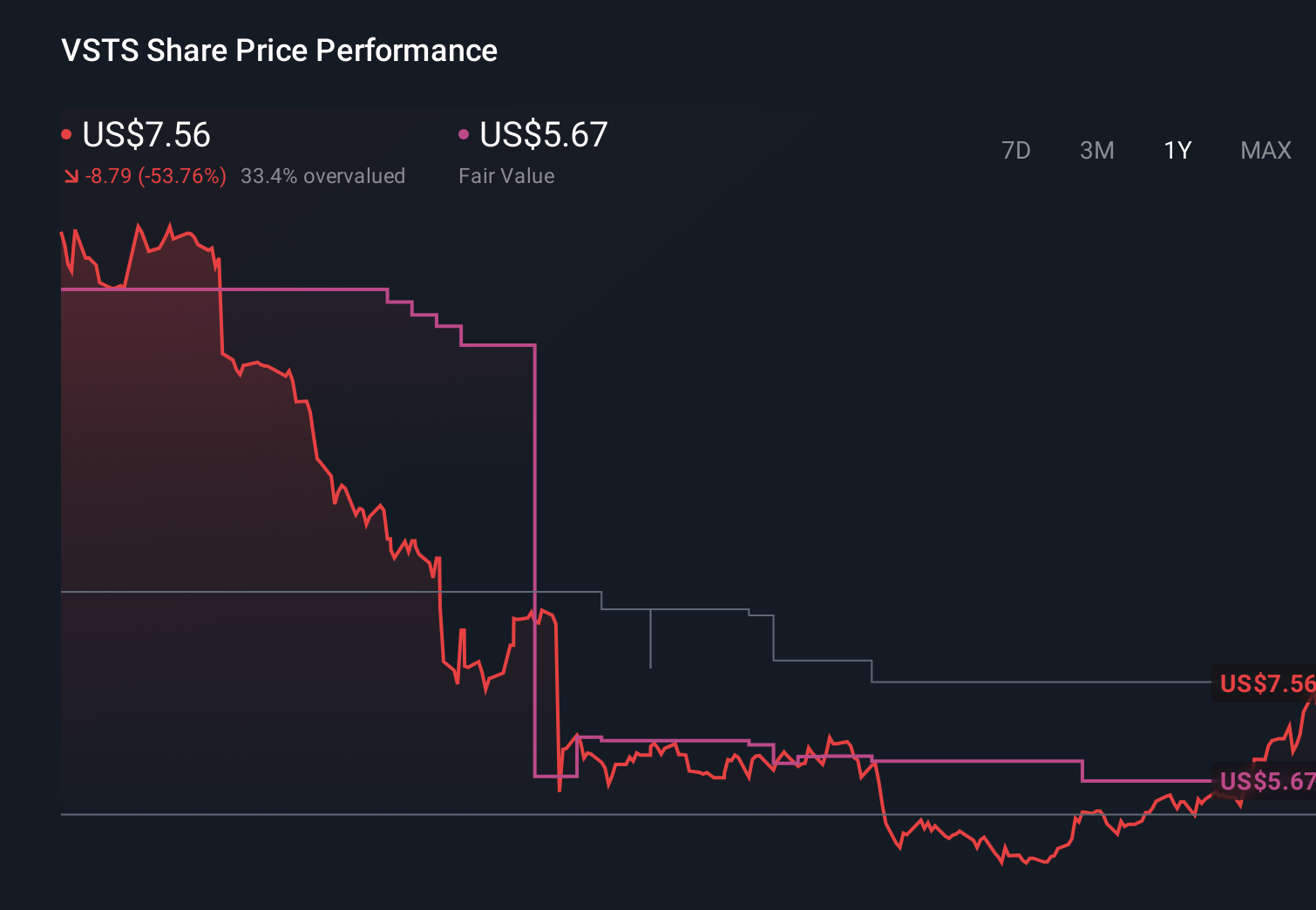

- Vestis Corporation’s first-quarter 2026 results, reported in February 2026, showed sales of US$663.39 million versus US$683.78 million a year earlier and a net loss of US$6.39 million compared with prior net income of US$0.832 million.

- Despite weaker revenue and a swing to loss, management reaffirmed full-year 2026 guidance, signaling confidence even as valuation views and forward earnings forecasts remain widely varied.

- Next, we’ll examine how reaffirmed full-year guidance despite a quarterly loss may influence Vestis’s previously outlined investment narrative.

Find 54 companies with promising cash flow potential yet trading below their fair value.

Vestis Investment Narrative Recap

To own Vestis, you have to believe its uniform rental and workplace supplies business can stabilize revenue, improve margins, and gradually repair its balance sheet. The first quarter 2026 loss and softer sales highlight pressure on that story, but the reaffirmed full year outlook for flat to down 2% revenue suggests management still sees its operational and pricing initiatives as intact. For now, this update does not materially change the key near term catalyst of execution on efficiency and pricing, or the main risk from customer churn and leverage.

The most relevant recent announcement is Vestis confirming its fiscal 2026 revenue guidance on the same day it reported the quarterly loss. Keeping that outlook in place, despite weaker results, ties directly to the catalyst of improving pricing discipline and operational upgrades, while also putting a spotlight on execution risk if contract losses, margin pressure, or high net leverage around 4.5x limit progress. With dividends and buybacks already restricted, delivery against this guidance has become an important confidence test.

Yet investors should also be aware that if customer churn remains elevated and leverage stays high...

Vestis' narrative projects $2.9 billion revenue and $62.5 million earnings by 2028.

Uncover how Vestis' forecasts yield a $5.67 fair value, a 26% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Vestis could reach about US$2.9 billion in revenue and roughly US$73 million in earnings, which is much more upbeat than consensus. Compared with the risk that long standing service issues could drive further customer attrition, this shows how far opinions can differ, and how this latest quarterly loss and reaffirmed guidance might lead you to rethink which version of Vestis' future feels more realistic.

Explore another fair value estimate on Vestis - why the stock might be worth as much as $8.00!

Build Your Own Vestis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vestis research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

No Opportunity In Vestis?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.