Please use a PC Browser to access Register-Tadawul

Get It

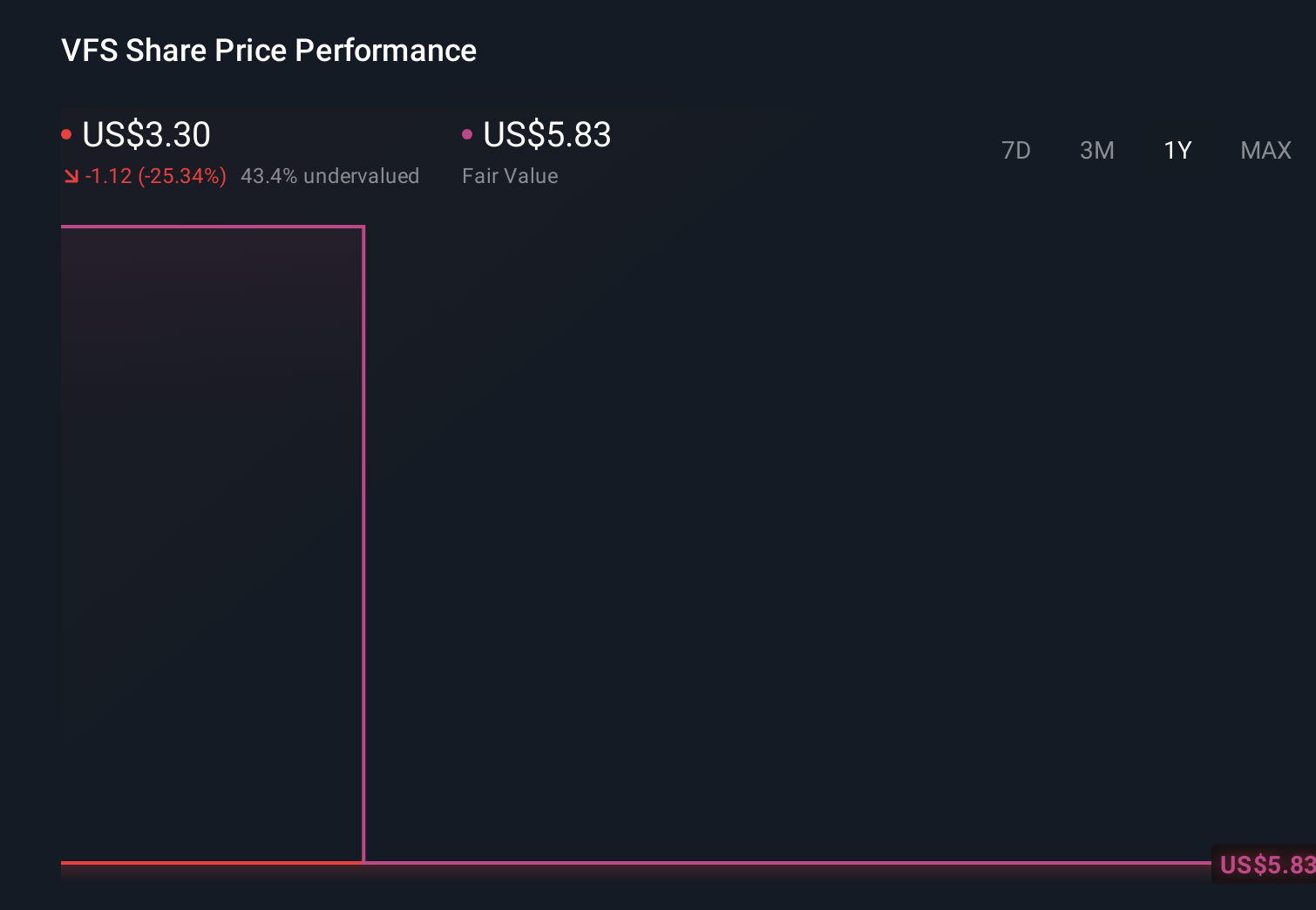

VinFast Auto (VFS) Is Down 8.3% After Wider-Than-Expected Q4 Loss Amid Global Expansion Costs

VinFast Auto Ltd. VFS | 2.86 | 0.00% |

Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

To own VinFast Auto today, you need to believe the company can turn rapid EV volume growth and global expansion into a sustainable, higher margin business before funding pressure bites. The latest results, with revenue up but full year net loss nearing VND 97,041,887 million, keep the spotlight on liquidity and cash burn as the key risk, while the near term catalyst remains whether rising deliveries can improve unit economics in coming quarters.

The most relevant recent update is VinFast’s Q4 and full year 2025 earnings release, which paired strong top line growth with a wider quarterly loss and deeper annual net loss. This tension goes to the heart of the current story: investors are weighing impressive reported revenue of about VND 90,427,611 million against persistent losses and a heavy investment cycle, and asking whether the scale up can realistically support the 2026 delivery ambitions already outlined.

Yet behind the delivery momentum, investors should also be aware of...

VinFast Auto's narrative projects ₫177,527.7 billion revenue and ₫8,991.9 billion earnings by 2028. This requires 48.9% yearly revenue growth and an earnings increase of about ₫89,207.8 billion from ₫-80,215.9 billion today.

Uncover how VinFast Auto's forecasts yield a $6.38 fair value, a 123% upside to its current price.

Some of the lowest analysts were already cautious, assuming roughly 47.3% annual revenue growth but no profits within three years, and you can see how Q4’s larger loss might push that already pessimistic view even further or, if execution improves, start to challenge it over time.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be a potential multi-bagger!

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.