Please use a PC Browser to access Register-Tadawul

Get It

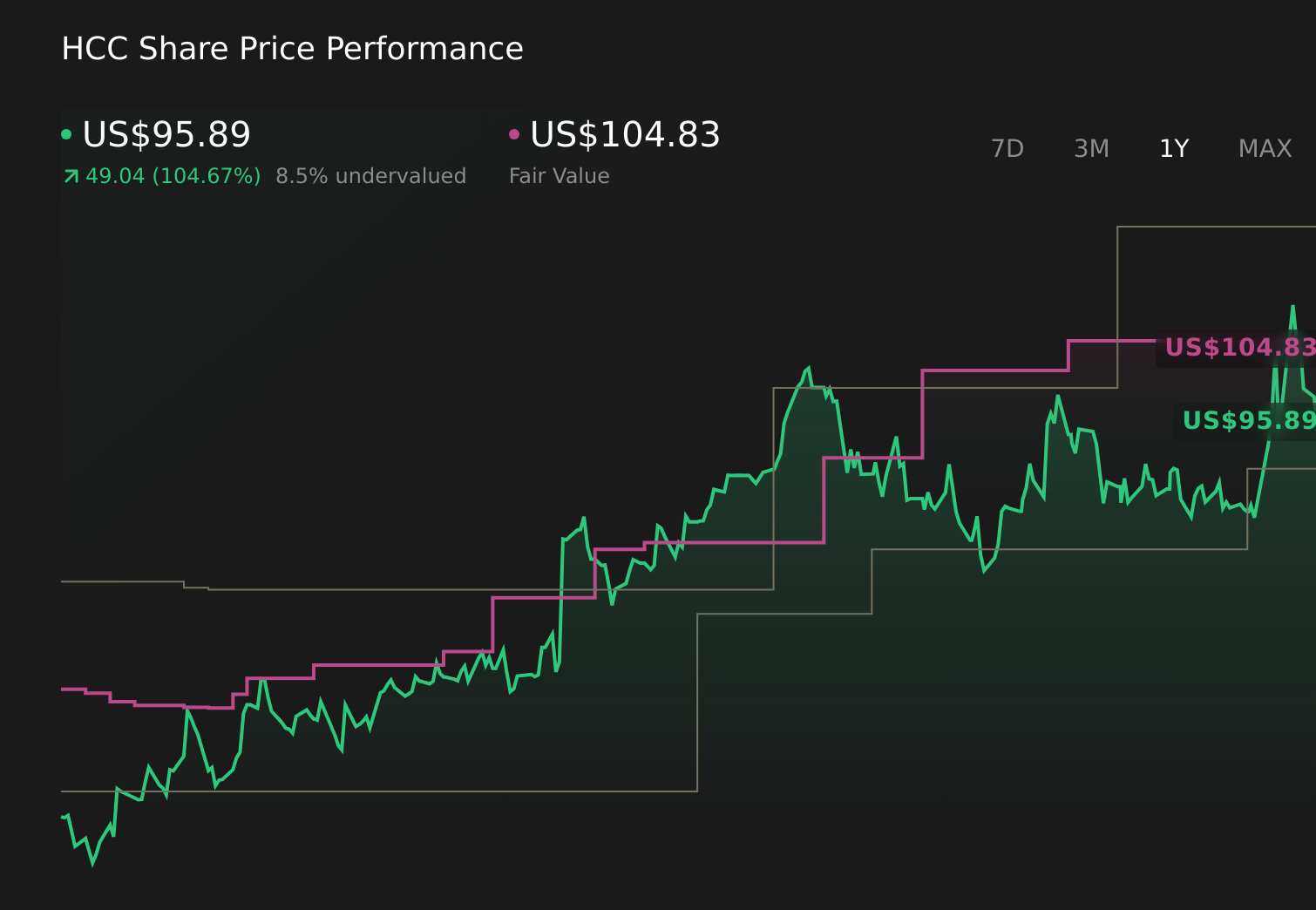

Warrior Met Coal Insider Sales Contrast With Valuation And Profitability Signals

Warrior Met Coal, Inc. HCC | 85.01 | -0.58% |

Warrior Met Coal focuses on producing metallurgical coal, a key input for steelmaking. For you as an investor, insider selling at a producer like NYSE:HCC sits alongside factors such as contract visibility, input costs, and steel demand, which often shape the longer term narrative around the business.

While 10b5-1 plans are designed to systematize insider trades, the scale and clustering of these sales can still influence how investors interpret management’s risk tolerance and capital priorities. As you monitor NYSE:HCC, this development may be one piece to weigh alongside upcoming company updates, board decisions, and any changes to capital allocation policies.

Stay updated on the most important news stories for Warrior Met Coal by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Warrior Met Coal.

Check out Simply Wall St's in depth valuation analysis for Warrior Met Coal.

For the full picture including more risks and rewards, check out the complete Warrior Met Coal analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.