Please use a PC Browser to access Register-Tadawul

Get It

Warrior Met Coal Ramps Up Blue Creek As Earnings Story Shifts

Warrior Met Coal, Inc. HCC | 85.01 | -0.58% |

Warrior Met Coal focuses on metallurgical coal, a key input for steelmaking, which keeps it closely tied to industrial and infrastructure demand. In this context, the early ramp up at Blue Creek and the newly secured federal leases represent a material change in the scale and longevity of its reserve base. For investors tracking NYSE:HCC, these updates help frame how the company is positioning itself within the metallurgical coal segment.

Looking ahead, the combination of earlier than planned longwall output and added reserves gives Warrior Met Coal more optionality in how it plans future production and sales volumes. Investors may want to watch how the company sequences capital spending, manages unit costs, and approaches contract versus spot sales as Blue Creek contributions build through 2026 and beyond.

Stay updated on the most important news stories for Warrior Met Coal by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Warrior Met Coal.

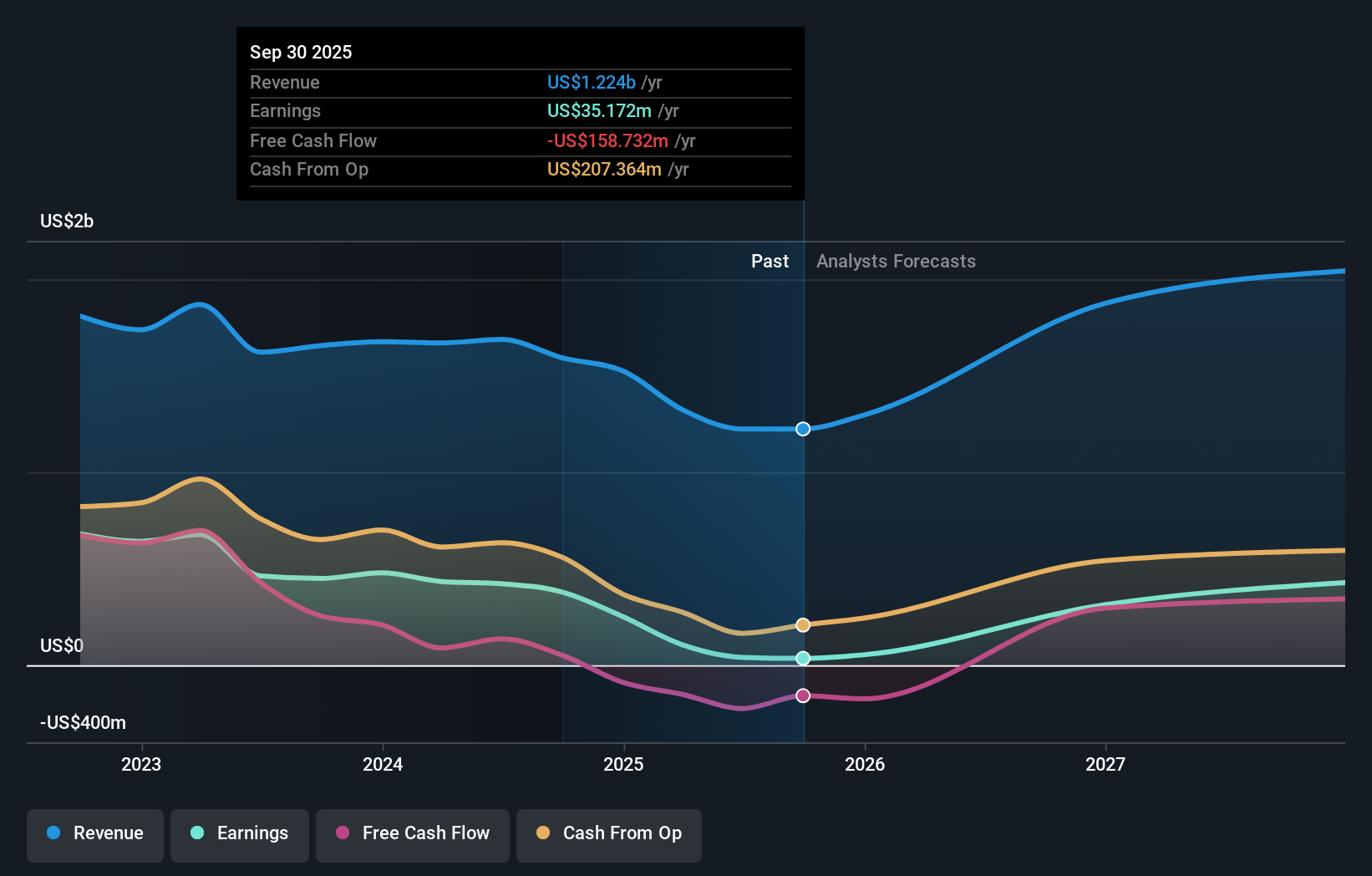

The early start at Blue Creek and the newly secured federal leases look central to how Warrior Met Coal is trying to reshape its production profile and cost base. Blue Creek contributed 1.3 million short tons in the fourth quarter of 2025, helping lift total steelmaking coal output to 3.39 million short tons versus 2.11 million short tons a year earlier. That higher volume fed into quarterly revenue of US$383.99 million and net income of US$22.96 million, compared with US$297.47 million and US$1.14 million respectively in the prior year period. At the same time, full year 2025 revenue and earnings stepped down from 2024, which suggests pricing and mix pressures despite the operational progress.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Warrior Met Coal to help decide what it is worth to you.

From here, it is worth focusing on how quickly Blue Creek scales within the 2026 guidance range and what that does to unit costs and margins. Pricing for metallurgical coal and the company’s mix between premium and lower margin products will matter just as much as tonnage. You might also track capital spending through the rest of the Blue Creek build out, free cash flow trends, and how committed management stays to dividends and any buybacks once major capex winds down. For context, peers like Arch Resources and Teck Resources provide useful reference points on contract coverage, realized prices, and cost structures in seaborne met coal.

To stay updated on how the latest news impacts the investment narrative for Warrior Met Coal, head to the community page for Warrior Met Coal to follow the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.