Please use a PC Browser to access Register-Tadawul

Get It

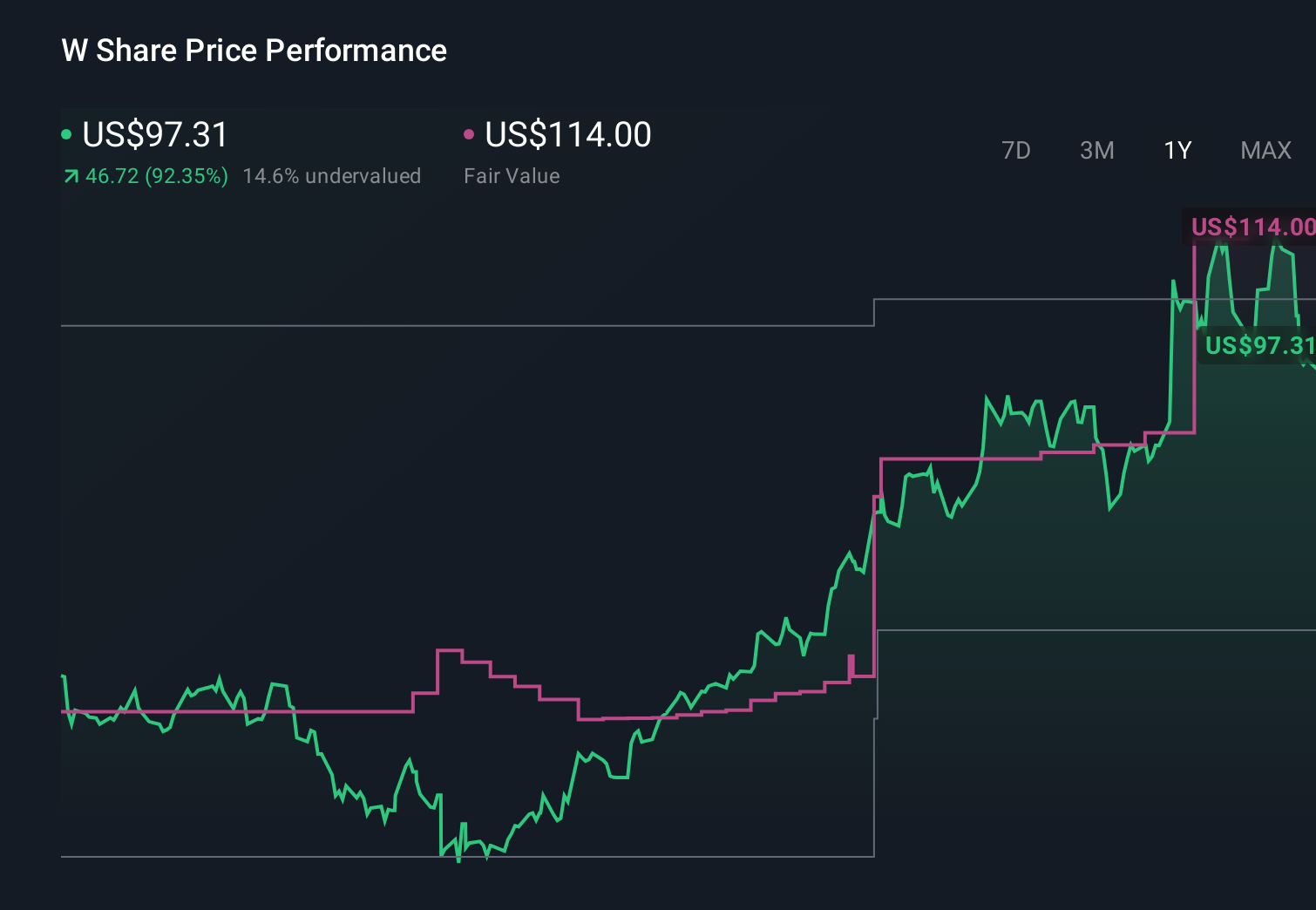

Wayfair (W) Is Down 17.2% After Revenue Rise But Renewed GAAP Losses Question Margin Progress

Wayfair, Inc. Class A W | 79.89 79.89 | +0.99% 0.00% Pre |

Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

To own Wayfair, you need to believe that its mix of e‑commerce, new stores, and logistics investments can eventually turn consistent revenue into durable profitability. The key short term catalyst is whether management can defend margins while funding growth; the biggest risk is that rising costs and tariffs keep GAAP results in the red. The latest earnings, with higher sales but a renewed net loss and margin concerns, directly heighten that risk rather than changing the story outright.

The most relevant recent development is Wayfair’s Q4 2025 report, where revenue and non‑GAAP EPS beat expectations but the surprise GAAP net loss and guidance for ongoing margin pressure unsettled the market. That reaction matters for the current catalyst because it shows how sensitive sentiment is to any sign that investments in logistics, international expansion, and physical stores are weighing on profitability more than they are supporting it.

Yet while revenue is growing, the renewed GAAP losses and higher cost pressures are exactly the kind of risk investors should be aware of...

Wayfair's narrative projects $13.9 billion revenue and $124.7 million earnings by 2028.

Uncover how Wayfair's forecasts yield a $113.64 fair value, a 50% upside to its current price.

The lowest ranked analysts were already cautious, assuming revenue of about US$13.3 billion and no profitability by 2028, which is far more pessimistic than the consensus and could look different once the latest margin setbacks and tariff impacts are fully reflected.

Explore 5 other fair value estimates on Wayfair - why the stock might be worth 48% less than the current price!

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

Opportunities like this don't last. These are today's most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.